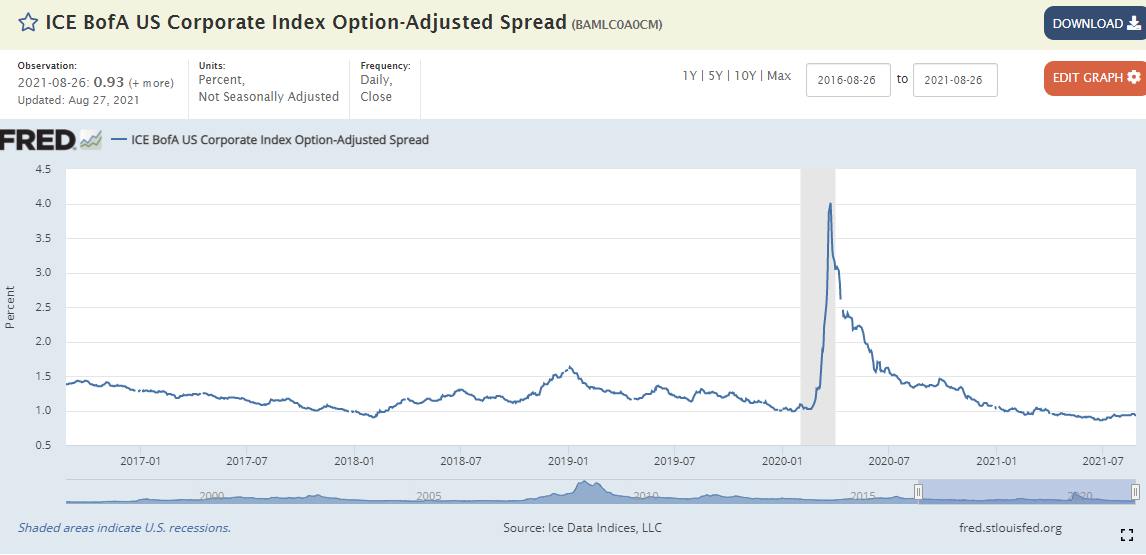

The above graph from the St. Louis Fed’s database shows the option-adjusted-spread (OAS) on the investment-grade or high-grade corporate bond index, and presently the spread is about 95 – 100 bp’s better than the equivalent Treasury.

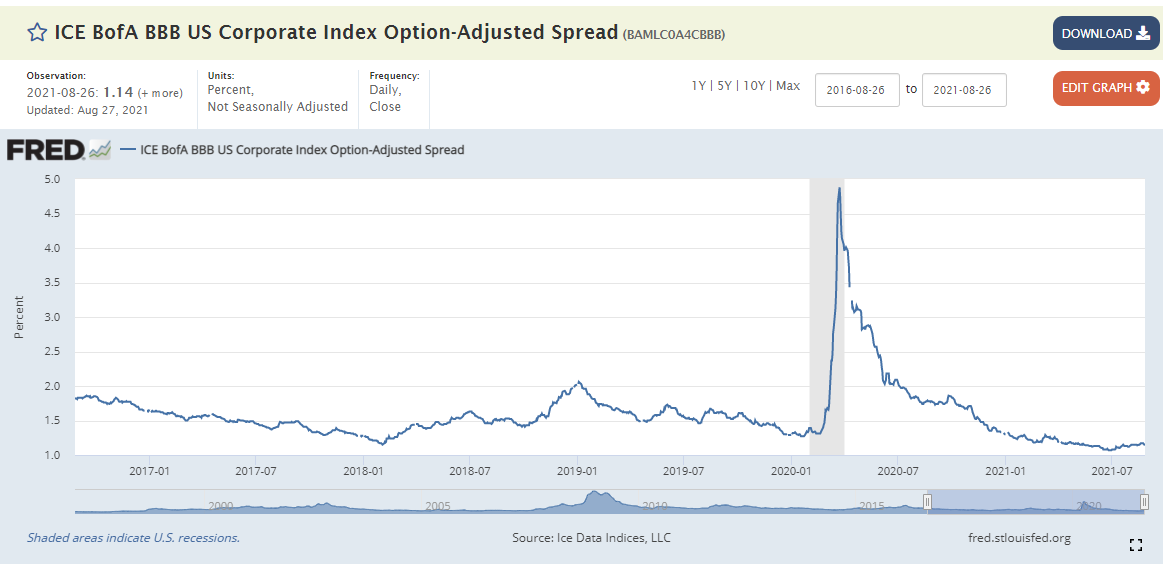

The chart, also from the St. Louis Fed website shows the BBB OAS on that particular segment of the corporate bond market and as of last Friday, August 27th, 2021, the BBB OAS was yielding about 104 bp’s over equivalent Treasuries, which should tell readers how vast the reach for yield has been in the last 18 months.

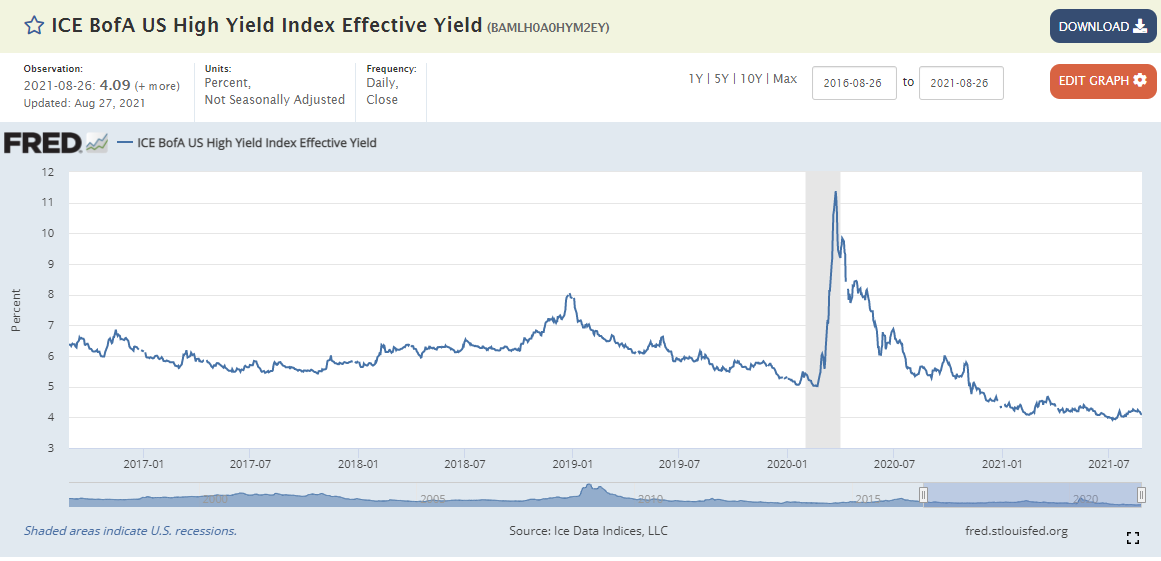

Finally, this ‘corporate high yield chart shows that the junk bond or below-investment grade asset class of the corporate bond market is yielding around 4%, but the spread-to-Treasuries the last few months has been pretty consistent around 350 bp’s.

Junk’s “spread-to-Treasuries” is still higher than in 2007, when according to Jessica Rabe over at DataTrek, the “tights” (i.e. tightest credit spread) for the corporate high-yield bond index hit it’s narrowest or tightest level ever.

Summary / conclusion: With Jay Powell’s statement last Friday morning, clients saw their municipal high yield exposures increased, with a tactical bet by me that the Fed won’t likely give a clear signal on tapering until their December ’21 meeting at the earliest. It’s clear the Delta variant has slowed air traffic and the re-masking might take a little starch out of the rapid US recovery. That being said, this coming Friday’s September 3rd, 2021, August jobs report is important with consensus expecting 750,000 – 800,000 “net new jobs” created in August ’21 and the unemployment rate falling to 5.2%.

The municipal bond market (this is a blog post from early February ’21) has been a big winner for clients in 2021, particularly muni high yield as the fiscal stimulus has bailed out cities and states like the City of Chicago and the State of Illinois. Both were rated Baa3 and on the verge of a downgrade to junk, which would be the only major city and state to sport a below-investment-grade credit rating, but – lo-and-behold – thanks to Washington’s Covid-19 stimulus and aid, both municipalities got an upgrade to Baa2 this spring.

Both Blackrock’s Rick Rieder and JP Morgan’s David Kelly gave conference calls lately and the conclusions were largely the same.

With the corporate high-grade bond index now having a duration very close to 9 years and the high-grade spread of about 100 bp’s, there is a lot more reward than risk in duration and high-grade credit these days. (More my words than theirs and readers can understand why.)

Client high-yield muni funds (two Nuveen funds) have really outperformed high-yield corporate this year with Nuveen’s John Miller’s muni high yield fund returning 8.07% this year while the shorter-duration Nuveen high yield fund is returning 7.06%, versus the Bloomberg’s High-yield Index 4.31% return. The HYG has returned 3.18% this YTD, as of last Friday, August 27th, 2021. (This blog post was written in mid-April ’18 and in hindsight it was a decent call. A lot of the corporate high yield funds went into muni high yield.)

My own take on this is that there is more and more risk in the credit and bond markets every day. $120 billion in bond buying is going to be “tapered” at some point – and as JP Morgan’s Dr. Kelly noted in last week’s call, Ben Bernanke tapered roughly $10 bl per month in 2013, from a smaller base (I believe), so we can probably assume that on an absolute level, this tapering will have to be larger.

Clients have a “tactical bet” on credit and yield for the next few months, but as year-end approaches and assuming no change in Fed commentary, the plan will be to re-allocate for 2022.

Take everything with great skepticism, and do your own homework. This could all change tomorrow.

Thank for reading.