A lot of big financial names report this week. Some will be covered here, in terms of pre-earnings analysis, with Tech to follow later in the week as many big technology names report the following week.

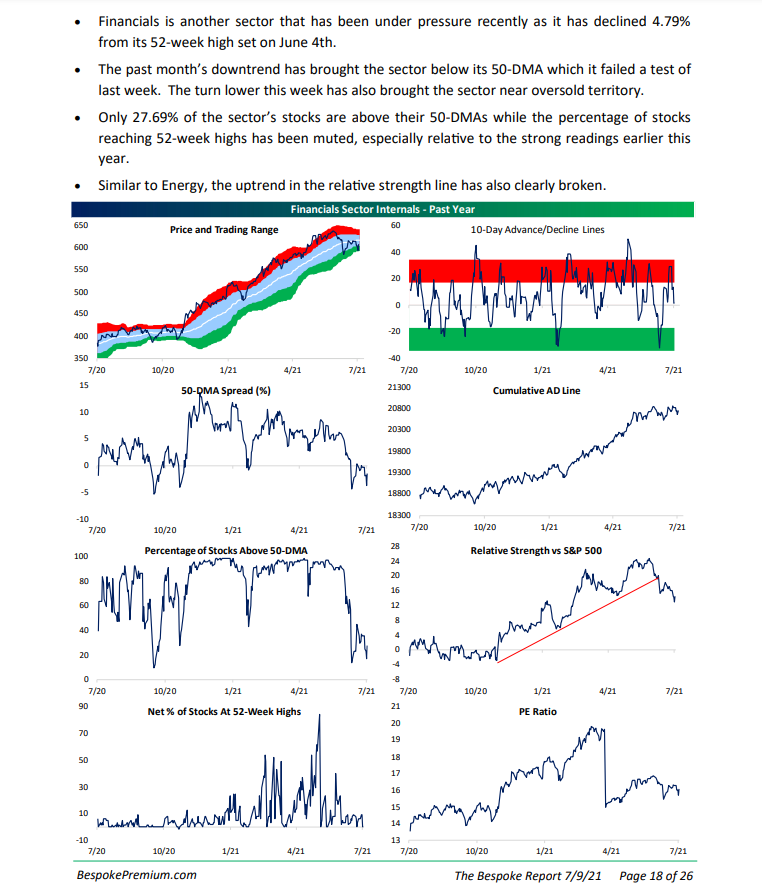

Bespoke – in their weekly (and always informative) Bespoke Report, published these metrics on the financial sector in Friday’s, July 9th, 2021 weekly review:

Of the 8 boxes, two caught my eye from a macro perspective on financials: the box at the top left showing the sector very oversold, and the box in row 3, in the right-hand column, showing the broken trendline. Personally, I think a lot of damage has already been done to the sector in terms of the correction, after the monstrous rally from the November 1 ’20 lows.

Individual stocks:

Goldman Sachs (GS): doing the prep for Goldman’s expected earnings release on Tuesday morning, July 13th, 2021, I was shocked at some of the numbers. Goldman shot the lights out in Q1 ’21, printing $18.60 in actual EPS vs the $10.22 estimate with actual revenue of $17.7 billion versus the $12.4 bl estimate. The backup in Treasury rates didn’t bother GS one bit as ROE hit 31% (not a typo, and per Briefing.com) w 117 IPO’s coming to market in Q1 ’21. Equity trading revenue rose 67% in Q1 ’21 vs 40% in Q4 ’20.

Goldman is expecting $9.95 in EPS for Q2 ’21 on $12.2 billion in revenue for expected y/y growth of 59% and -8% respectively, which will be quite slowdown from Q1 ’21. The SP 500 was up 15.25% as June 30, credit markets were stable, SPAC IPO’s were bouncing back, so the capital markets while not as white hot as 2020 during the summer, shouldn’t present an issue for Goldman’s numbers.

Here’s is the number that was shocking: if Goldman just meets the $9.95 consensus (IBES by Refinitiv source) Goldman will have printed $50 per share in 4-quarter trailing EPS, leaving the stock trading at 7.5x trailing earnings. Full-year ’21 consensus today is expecting 46% EPS growth on 14% revenue growth and at $371 per share is trading at just 8x earnings.

Because Covid and the pandemic played havoc with the financial sector, looking at four-year average EPS and revenue (2019 through 2022), Goldman is currently expecting 7% revenue growth and 14% EPS growth.

Goldman’s stock looks very cheap here on a P/E basis, but the sell-side EPS and revenue estimates are actually lower for full-year ’21, ’22 and ’23 than the trailing $50 in EPS and $50 billion in revenue.

The Street (sell-side consensus) has never done a good job modeling their own business. The brokerage stocks have the highest standard deviation of “actual vs consensus” estimates, for any sector besides semiconductors.

For GS to earn $50 per share on TTM basis when the bank earned just $21 per share in 2019 is pretty amazing.

JP Morgan (JPM): Jamie Dimon’s house is the perfect combination of individual and corporate banking and capital markets. JPM can win (or lose) both ways, but this quarter there will likely be more upside revisions even though Jamie warned on revenue during the quarter.

JPM is looking at consensus estimates of $3.17 and $30 billion in revenue when they report their Q2 ’21 financial results on Tuesday morning, July 13th,

JPM will have earned between $15 – $16 per share on a 4-quarter trailing basis if consensus is met, and like Goldman, the forward estimates are actually lower than that for calendar ’21, ’22 and ’23.

The bank still had about $4.7 billion of share repurchases left at the end of Q1 ’21.

Trading at 10x trailing EPS and 12x expected ’21 EPS, and 2x tangible book, the stock has close to a 3% dividend yield at $150, and there should be dividend increases coming.

The flatter yield curve since March hurts all the spread banks, but JP Morgan has hat capital market booster.

The bank is one of client’s “Top 10″ positions and has been for years. The London Whale was a killer, but Jamie has a remarkable track record over the years.

Charles Schwab (SCHW): Schwab is typically a mystery when it releases earnings, but Briefing.com has Schwab slated for Thursday morning, July 15th, 2021, before the market opens.

Schwab EPS and revenue estimates are still being influenced by the Ameritrade merger which went on the books in the 4th quarter of 2020, thus the year-over-year compares are still showing the “acquired” EPS and revenue as opposed to organic growth.

Schwab consensus is expecting $0.75 in EPS on $4.45 bl in revenue on Thursday morning, July 16th, 2021, for year-over-year growth of 39% and 82% respectively. It’s the merger with Ameritrade and not the pandemic influence from 2020 that is driving the numbers (although, yes, the SP 500 correction and the spread widening influenced asset values in Q1 and Q2 ’21), but since the merger, Schwab is seeing nothing but positive EPS and revenue revisions since, and particularly after Q1 ’21’s results.

Goldman downgraded the stock this week, but if you look at the forward estimates and the expected growth, and (again) using the 4-year average since 2020 and 2021 are so distorted, Schwab is expected to grow EPS 12% and revenue 19%, while trading at a low 20x’s multiple.

What caught my eye after Q1 ’21’s results and the upward revisions was that Morningstar raised their long-term operating margin assumption in Schwab from 46% to 52%, which – given that Schwab’s expected revenue growth in ’21 and ’22 will be higher than EPS growth makes sense.

Schwab has always been disciplined about their margins, and that’s something I feel as a $32 million adviser who custodies all assets at Schwab.

Mr. (Chuck) Schwab was one of the original disrupters starting Schwab after “the big bang” or commission deregulation in the early 1970’s. It’s a longer story that needs to be told after Schwab releases earnings on Wednesday.

Schwab is another “Top 10” holding. I like to own disruptors for clients and Schwab is still doing that.

Bank of America (BAC): Brian Moynihan’s shop like JP Morgan has a combination of old bank and capital markets which we like to see in this kind of market environment.

Bank of America is expected to report Wednesday morning, July 14th, before the open and – per consensus – the Street is expecting $0.77 for 108% y/y growth on $22 billion in revenue, for 1% decline.

One of the notes from the Q1 ’21 conference call was that BAC could still another $1 billion in loan loss reserves and the dividend has yet to change, so BAC would a prime candidate for returning more capital (as I see it).

At $40 per share as of Friday, July 9th’s close, BAC is trading at 13x estimated 2021 EPS of $3.06 and all three calendar estimates i.e. 2021, 2022, and 2023 continue to be revised higher.

I think the stock is cheap here. but a trade down to $35 or near the 200-day moving average, would make the stock very cheap. At $40, BAC is also trading at 2x tangible book value.

Summary / conclusion: Given how the numbers lay out i.e. trailing 4-quarter EPS vs forward estimates, or calendar year estimates, there is an expectation we are seeing “peak earnings” or will see “peak earnings” with the June quarter’s results for the likes of Goldman Sachs or JP Morgan. Without making a prediction, I’m not convinced of that.

It’s clear the banks didn’t like the yield-curve flattening since March ’21, (check the KRE or regional bank ETF chart) but the bigger banks are still aided or supported by capital market activity.

The key metric coming out of the next week, will be what happens to 2021 revenue estimates for all the firms above, and how does that number get revised i.e. up or down ?

2020’s 2nd quarter was actually pretty strong when looking at actual revenue in Q2 ’20 vs the consensus estimate, so revenue revisions will matter more than EPS revisions coming out of this week’s results.

I still like the sector and remain overweight the sector with JP Morgan, Schwab, being the two top holdings, while CME is a lighter weight and some Berkshire and Bank of America is owned. Of the names above, BAC looks like the better value in terms of a reasonable PE to low-teens growth, and more of it may be bought for clients. Although earnings weren’t previewed, I like Morgan Stanley’s acquisition of Etrade, and what that combination could mean. I think Morgan has repositioned faster than Goldman for the retail investor, but from the numbers Goldman put up maybe that investment banking and M&A is really the right place to be.

Financials have a 10% – 11% market cap weight in the SP 500, down from their peak of 17% 5 – 6 years ago. The era of and repeat of 0% interest rates and 1.4% 10-year Treasury yields is not helping the spread lenders.

Take everything here with great skepticism. The consensus estimate numbers will change and some maybe materially after earnings this week.

Thanks for reading.