Q2 ’26 financial results for the SP 500 start in earnest on Monday, July 13th, 2026 as the financial sector typically kicks off the first two weeks of earnings.

The big banks have lagged badly YTD as JPMorgan (JPM) is up just +0.47%, Bank of America (BAC) is +2.87%, Wells Fargo is down -9.20%, all while the SP 500 is +9.08%. Citigroup (C) stands out with a with a +20.86% YTD return as of Friday, June 12th. With Kevin Warsh’s first FOMC meeting this week, the financial sector might be spooked by the constant chatter over a move to raise the fed funds rate in the 2nd half of ’26, however let’s see how crude oil trades on Monday, June 15th, 2026, when we might see something in writing on Iran, and potentially a Strait of Hormuz re-opening.

This blog has been long more duration over the last 18 months than (in hindsight) I’d like to admit, but a note from Bespoke this weekend notes that “core CPI ex-rent”, is closer to 2%. It’s always an “iffy” proposition when certain numbers start getting excluded from critical econ data releases, but Bespoke summarized it this way for readers, “Taken together these top-level measures of CPI paint a mixed picture of still above-target inflation but less acceleration than we saw earlier in the year.”

It’s a personal belief that the mainstream financial media always overstates the “inflation threat”.

This blog’s single-largest financial sector position remains JPM as of 5/31/26, with a 5% weight in the composite portfolio. (Long all, except Wells Fargo (WFC), which is still below it’s 200-day moving average.)

The two larger financial ETF’s – the XLF and IYF – both have Berkshire (BRK.B) as their largest position to the tune of a 10% – 11% market cap weight in each ETF, with the stock trading down YTD.

SP 500 earnings:

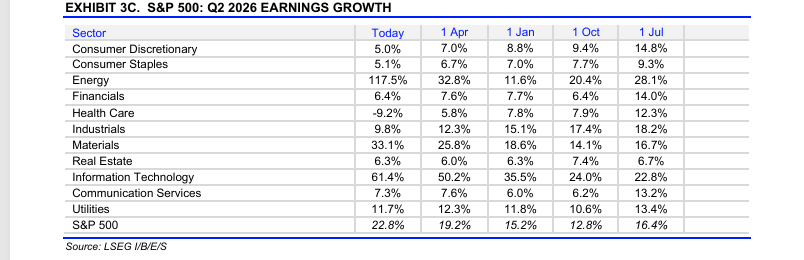

While this blog post from last Sunday, June 8th, gave an initial look at how Q2 ’26 financial results are shaping up, the numbers this week at the sector level see increases for expected Q2 ’26 technology and basic materials EPS growth, while the overall SP 500 EPS growth of +22.8% is pretty much unchanged from last week.

While Q2 ’26 expected EPS growth by sector could be helpful to readers the fact is that the trend is in place for Q3 ’26, and Q4 ’26 expected EPS growth by sector for the SP 500.

Little has changed on the SP 500 earnings front, when looking forward.

Quick Summary: Only Kroger (KR) and Accenture (ACN) report this coming week, (Thursday, June 18th) with no positions in either stock. An eye is kept on Kroger, since it’s right in the path of Walmart (WMT), given Walmart’s market share presence in grocery. Berkshire Hathaway has owned Kroger, which is interesting, since I thought Walmart would be the quintessential Buffett stock, but Walmart has never seemed to have a spot in the Berkshire portfolio.

Micron Technology (MU) reports the week after on June 24 ’26, and that will be a key earnings report for a while-hot sector. Semiconductors, per the Bespoke Report this weekend, have jumped to a global market-cap weight of 10% (the various SOX components) versus a market cap weight of just 2.1% 4 years ago.

If you traded the semiconductors in the late 1990’s, you have a healthy respect for the sector. Like the airline stocks, and the auto companies, the semiconductor stocks have formidable operating leverage, so the sector’s EPS estimates and cash-flow can decline rapidly if the semiconductor demand environment changes.

Just know what you own.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. None of this information may be updated, and if updated may not necessarily be done on a timely.

Thanks for reading.

Brian,

You might find some value in the interview linked below of bank analyst Charlie peabody from earlier today: https://www.youtube.com/watch?v=wVPU4kyzp0Y

Charlie’s core view is that banks are near peak earnings momentum and peak relative valuation, not because current numbers are bad, but because too many positives are simultaneously at extreme levels.

His bigger warning is that private credit, opaque balance-sheet structures, and heavy capital markets supply are the areas most likely to create the next real problem.

He does not argue that banks are the next 2008-style villain. He argues they may hold up better than private credit, but that does not mean bank stocks are attractive at current valuations.

A consistent late-cycle pattern: peak confidence, peak issuance, peak deal appetite, slowing internal momentum, and too much belief that the credit cycle can be postponed indefinitely.

Charlie’s core view is that banks are near peak earnings momentum and peak relative valuation, not because current numbers are bad, but because too many positives are simultaneously at extreme levels.

His bigger warning is that private credit, opaque balance-sheet structures, and heavy capital markets supply are the areas most likely to create the next real problem.

He does not argue that banks are the next 2008-style villain. He argues they may hold up better than private credit, but that does not mean bank stocks are attractive at current valuations.

A consistent late-cycle pattern: peak confidence, peak issuance, peak deal appetite, slowing internal momentum, and too much belief that the credit cycle can be postponed indefinitely.