A “12-week rate of change” section was added to the SP 500 forward earnings curve analysis:

The data is telling us that for periods where the current quarter’s have reported, note the upward revisions and the size of the “12-week rate of change”.

For the forward periods q4 ’20 – Q3 ’21 and 2021 calendar, the 12-week rate of change is much smaller.

That’s one clue that Street (i.e. buy and sell-side analysts and strategists) remain a little sheepish in terms of raising estimates, despite the upside strength to Q3 ’20, or put another way, once the Street has seen actual earnings like Q2 ’20 and Q3 ’20, note the strength in the upward revisions.

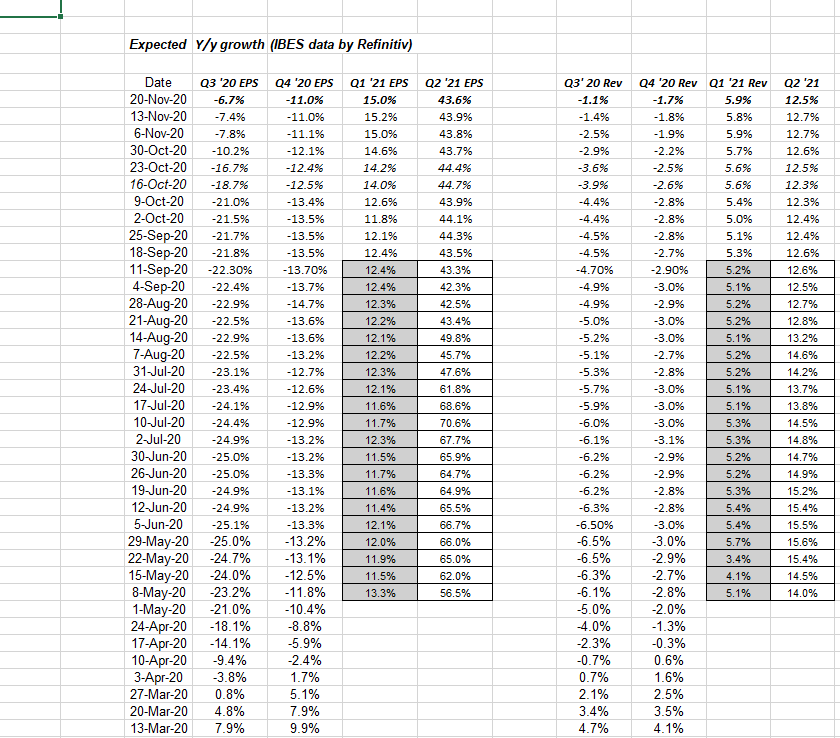

Q3 ’20 through Q2 ’21:

The story is still a positive for the SP 500 or maybe to be a little more cautious, there is little to be worried about currently in the next 4 quarters expected SP 500 EPS and revenue growth.

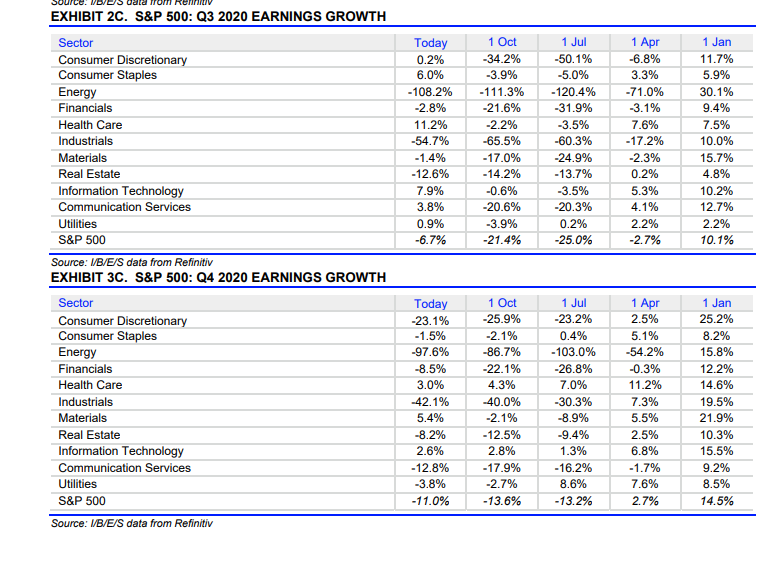

Q4 ’20 – how the growth rate expectations have changed:

Note the upward revisions to Q3 ’20 expected EPS growth rates for sectors like Consumer Discretionary (Amazon), Communications Services (Google and Facebook) and Consumer Staples after the 3rd quarter earnings have been reported. Those are substantial improvements in Q3 EPS estimated growth rates after seeing the numbers. Readers and investors can also infer from this and Q2 ’20 results that Street analysts have had a tough time modeling the numbers.

Now look at Q4 ’20 estimates. Energy, Health Care (somewhat surprisingly) Technology (also surprising but a very small negative revision), and Utilities are the sectors that have seen downward pressure on their expected EPS growth rates. Technology went from an “expected EPS” growth rate of 2.8% on October 1 to 2.6% on November 20, ’20. Hardly alarming, but look at the improvement in the Financial sector since October 1.

The sell-side analysts and buy-side strategists that model and post their estimates to the various services have been overly conservative in their estimates during the pandemic i.e. Q2 ’20, Q3 ’20 and potentially q4 ’20.

The rest of the SP 500 data:

- The forward 4-qtr estimate” this week was $159.90 versus last week’s $159.92

- The forward PE this week is 22.36x

- The SP 500 earnings yield is 4.47%, hovering around the 4.50% area the last 3 weeks. Still pretty low in my opinion, but likely to improve based on higher forward EPS probably more so than a 20% correction to “price” or the denominator (i.e. SP 500).

- The average expected growth rate for 2020 and 2021 SP 500 EPS is 3% this week, down from 4% for most of the last 6 months.

Summary / Conclusion: The weekly SP 500 earnings update is yielding few surprises or trend changes, despite the lack of fiscal stimulus, Covid-19 worries, and the President’s persistent accusations of fraud around the Presidential election.

Not much has dented this stock market this year with the SP 500 +12% YTD. Even corporate high-yield credit improved this week despite Treasury Secretary Mnuchin not renewing some of the Fed liquidity programs, which would have been a backstop for corporate credit. The fact is though, corporate credit improved in 2020 on it’s own once just the presence of the Fed liquidity programs were announced in late March ’20. I do think the Fed or Treasury bought some HYG via the programs in July ’20, but it was a small amount relative to the size of the program and the credit markets had already resumed functioning by the end of April, 2020.

2021 will likely have a very different “attribution” in terms of the SP 500 return versus this year.

More will be disclosed near year-end, but expect that the sector stars of 2020 may not have the same repeat performance in 2021.

Take everything you read here with substantial skepticism. SP 500 earnings and revenue estimates can change very quickly.