Q1 ’20 SP 500 earnings are going to reflect (probably) a strong January and February, 2020 and then a very weak March, 2020 while the 2nd quarter will / could reflect a very weak April, 2020 and then a slowly improving May and June, 2020.

The difficulty with earnings-watchers such as myself is how to handicap the US economic shutdown that was the equivalent of driving a car down an expressway at 60 MPH, with everything going smoothly and then throwing the car into park.

Here is one suggestion: use the annual and quarterly averages as was suggested last Wednesday night, for getting a more-accurate longer-term read into SP 500 earnings.

A preview of JP Morgan’s earnings was just written for Seeking Alpha and if you look at the “expected” consensus for JP Morgan’s revenue and earnings for 2020 through 2022, the consensus is expecting just 2% EPS and revenue growth for the banking giant over the next 3 years on average.

That’s too low: the bank grew average revenue 2% from 2011 through 2019 and EPS (even with the London Whale incident) 15% for the entire decade.

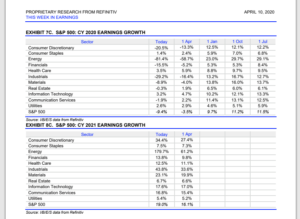

Currently looking at the SP 500 as a whole, the “whisper” number for SP 500 EPS for 2020 as a whole is an expectation of a 20% – 25% decline, while the 2021 SP 500 is currently expecting 19% EPS growth.

Personally, I think JPM is probably cheap here trading at a 15% – 256% discount to its long-run “intrinsic value” estimate of $115 – $125 per share, but investors have to look through the current earnings cycle and into 2021.

Here is the current 2020 – 2021 full-year consensus from IBES by Refiniitv:

Here is another data point you won’t see in mainstream media:

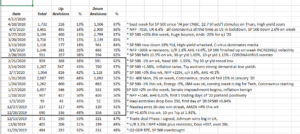

Usually the last two weeks of one quarter and the first week of the new quarter have very few estimate revisions, since analysts typically have their models set and simply await the earnings results, but Covid-19 has had analysts furiously adjusting their models with the new expectations and the result of the shutdowns, so earnings revisions have surged already, usually consistent with mid-quarter reporting.

To my knowledge, no sell-side analysts have been through a pandemic before so undoubtedly there is a wide variance around Q1 and Q2 ’20 SP 500 EPS and revenue results.

Assume this when looking at the data changes, although “consensus” will still be the best forward-looking data we have.

Finally don’t forget “SP 500 revenue” consensus:

SP 500 revenue is expected to fall 4.3% y/y in Q2 ’20, (the expectations are that it will be less than 1% currently for Q1 ’20) which is a big drop for the benchmark.

The last time revenue fell this much year-over-year was the middle of 2015 and was also due to Energy revenue falling 35% y/y in the middle of 2015.

It requires a longer post to detail this for readers, but what’s interesting is that in the middle of 2015, we didn’t see the harm to consumer demand (i.e consumer discretionary sector) that we see expected in Q2 ’20.

Summary / conclusion: Try and look at some of the averages both for Q1 and Q2 ’20 and for 2020 and 2021. The pundits will have readers focusing on 2020 and the collapse of SP 500 EPS which garners headlines but as the US looks to reopen look at longer-term SP 500 estimates like Q3 ’20 and then 2021 because the SP 500 benchmark will be discounting all of these timeframes.

take all this with substantial skepticism, and a healthy grain of salt. Covid-19, a vaccine, even an anti-viral could appear quickly.

Events are changing rapidly.

Thanks for reading,