Being overweight Technology and Financial’s for clients like the Yin and Yang of investing. Airlines, the Energy sector, cruise lines, casino’s and gaming, all the problem children were avoided this last bull market.

All but the Financials – with clients two largest holdings being JP Morgan (JPM) and Schwab.

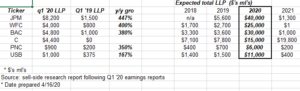

click to open / enlarge

If you are wondering what’s happening with the big banks, this spreadsheet was prepared using a sell-side research report showing the expected growth in “loan-loss provisions” for the big banks in 2020.

JP Morgan is a big chunk of the major banks with Bank of America following.

The left side of the table is the LLP for just Q1 ’20, and shows the year-over-year growth vs 1 year ago, to give readers some scale as to the enormity of the losses expected.

So what’s the good news ?

DAILY DATAPOINT

Every month we look at price correlations across a variety of asset classes and sectors, and today we’ll look at large cap banks (using the S&P Banks Index/KBE ETF) and their smaller brethren (S&P Regional Banks Index/KRE ETF). The point of this analysis:

Bank stocks are usually early cycle stock market outperformers and, given that US financial institutions are better capitalized now than at any point in the last +20 years, they should provide market leadership this time around as well.

But… today’s bank stock performance was pretty dreadful, with the Banks Index down 5.1% and Regionals down 5.6%. Not the sort of price action one likes to see a day before earnings reports start.

While government programs like PPP and larger unemployment checks will help sustain the US economy, access to credit is the fundamental engine of American economic growth. As long as bank stocks remain under pressure, the market is signaling that all is not well with this conduit.

Also worth mentioning: banks are the largest single piece of the S&P 500 Value Index (8%) and a truly outsized part of the Russell 2000 Value Index (20%). Banks will have an outsized impact on when the Value trade starts to work.

There are 2 charts below with the historical price correlations for the KBE ETF (large banks) and the KRE ETF (small banks) versus the S&P 500. We use daily price returns and trailing 90-day correlations to the index. Here is what we see in the data:

#1: Large/small bank stock return correlations to the S&P 500 are at 0.92 and were as high as 0.95 in mid-March, basically the same as their all-time highs back to 2006. Remember: correlations can only go to 1.0, and the average correlations since 2010 are much lower than now (0.76 for large bank stocks, 0.72 for small bank stocks).

#2: The only other time we’ve seen bank stock correlations to the S&P 500 this high was in Q4 2011 during the Greek debt crisis. They were over 0.9 from mid-August 2011 all the way through to January 2012 (for small caps) and mid-March 2012 (for large caps).

#3: It was only after these correlations started to break apart that Financials led the S&P higher in 2012, 2013 and 2014:

2012:

Large cap Financials: +28.8%

S&P 500: +16.0%

2013:

Large cap Financials: +35.6%

S&P 500: +32.4%

2014:

Large Cap Financials: +15.2%

S&P 500: 13.7%

The bottom line here: sector correlations decline when industry fundamentals start mattering more to stock returns than general market conditions, so it makes sense that Financials led the market higher once we got past 2009 – 2011. The initial move off the bottom for US stocks post-2008 was more about “the world did not end” than anything else, after all.

That means Financials are the group to watch, the stocks that signal when real economic recovery is taking place. History says we may have to wait a few months to find an investable level for the group, but the fact that correlations are so high just now shows the clock has at least started.

The above is cut-and-pasted from Bick Colas and Jessica Rabe’s DataTrek blog, dated April 13th, 2020.

Unfortunately, two charts didn’t come through, but the point from the blog was that – once correlations start to show some distinction or dispersion, then Financials have historically started to outperform.

The blog makes a very interesting point in the last sentence and should be noted by readers.

Summary / conclusion: This blog post might be particularly timely given the Administration’s Press Conference tonight about re-opening procedures for the states, and also the Gilead Remdesivir news afer the close tonight.

Clients long exposure includes the XLF and the KRE (and these ETF’s have taken a beating for sure in the last 60 days)

The logic is the quicker the opening of the US economy, the lower should be some of the “expected” loan-loss provisions (and don’t forget potential recoveries from those loans written off) and the less hit to bank EPS could be expected going forward.

Much of this is tied to employment and income data obviously, but this isn’t 2008 – 2009 either. The US economy slammed shut and will be reopened gradually, maybe faster than expected.

JP Morgan – after earnings estimates have been updated post-earnings – is expecting a decline of 4% in revenue in 2020, with an expected decline of 49% in EPS, much of that loan loss provisions.

(Take all opinions on stocks, sectors, markets, with substantial skepticism. Evaluate all information in light of your own comfort levels, risk profile and financial profile. Markets change quickly and the information herein may not be updated.)