When Cisco nearly hit $60 per share in July, 2019, the 19% EPS growth generated in fiscal 2019 by the networking giant was mostly buyback-supported. Between October ’18 and August 1, 2019 or the end of Cisco’s 2019 fiscal year, between $21 – $21 billion of Cisco’s cash balance was spent repurchasing shares or for for those who like to do the quick math, a per quarter average of $5.0 to $5.2 bl in common stock was repurchased.

Since August ’19, or after one quarter of fiscal 2020, just $780 million of shares were repurchased.

It’s not necessarily a negative, but Cisco is one of the classic 1990’s “growth babies” that is “caught-in-the-middle” (to use a Michael Porter, Competitive Strategy term) as management is transforming the Cisco model from a data networking and communications model to a Security, Applications and subscription model that moves away from Routing and Switching (to the extent it can).

It’s not an easy job and Chuck Robbins is doing a decent job to reshape the company for the next 20 years.

When Cisco reports after the closing bell on Wednesday, February 12th, 2020, Street consensus is looking for $0.76 in EPS on $11.76 billion in revenue for expected year-over-year growth in EPS of +4% on a 4% decline in revenue. Fiscal 2020 consensus is expecting just 1% revenue growth and 5% EPS growth, a far cry from last year’s 18% EPS growth on 5% revenue growth.

Last quarter, fiscal Q1 ’20, Cisco’s revenue guide for this Q2 ’20 was worse-than-expected, which sent the stock down 7% post earnings, but that is now in the stock price, and expectations are subdued for the networking giant.

Really, fiscal 2020 is a transition year as some of the “macro” from slowing trade and Emerging Market service provider weakness has reigned-in expectations.

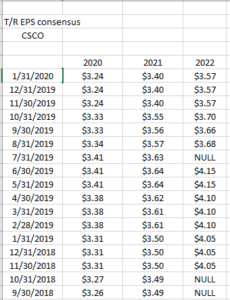

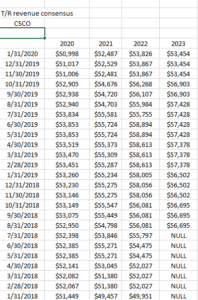

How do EPS and revenue estimate revisions look ?

Source: IBES by Refinitiv

Data source: IBES by Refinitiv

Readers can see that EPS and revenue estimates for this fiscal year and beyond pretty much track or correlate with the progress on US – China trade and tariff issues (not to mention friction over Huawei) so as Cisco puts distance between that macro situation and it’s business model, the stock should reflect that.

Although it’s not shown, if readers did the math, the “average” annual revenue growth expected by the Street for Cisco from 2020 through 2022 is 2% and expected EPS growth is 5%.

What’s the worry ?

Unlike Microsoft, Oracle, IBM, Apple (long all to some degree) and others from the late 1990’s, transforming a business model on the fly is a tough task. I felt like John Chambers in a lot of ways stayed mired in the past to a large degree, thus the task facing Chuck Robbins is even more urgent and pressing. Apple did it in a remarkable fashion, transforming a Tech Hardware model into a higher-margin Services model on the fly without missing a beat in terms of growth.

Cisco’s got a far tougher transition ahead of it.

Before the share repurchase “bulge” in fiscal ’19, Cisco was generating about $2.5 bl in free-cash-flow per quarter. Since tax reform was passed in December ’17, Cisco’s cash balance has fallen from $74 billion in January ’18 to $23 billion as of November ’19.

The Kid is spending a lot of cash to keep investors interested in the stock.

Here’s some quick valuation metrics as of the Nov ’19 quarter:

Fwd div yield: 2.8%

Cisco has found a bid in the low $40’s twice in late 2018 and then again November, 2019, which is probably close to a 3% dividend yield.

As far as can be told, we don’t yet know what the new Cisco dividend will be for 2020, but it will be interesting to see how the Board responds. The last four dividend increases (per quarter) have been $0.05 a quarter (calendar 2016), $0.03 a quarter (calendar 2017), $0.04 a quarter (calendar 2018), and $0.02 a quarter (calendar ’19).

If the pattern holds, $0.03 a quarter or $0.12 a year would be calendar 2020’s dividend followed by a $0.01 in calendar 2021.

(But that’s a guess.)

Summary / conclusion: Cisco hit an all-time-high of $82 per share in March of 2000, and has never looked back. The next highest print was $35.00 and change in December ’07, which wasn’t really broken above until 10 years later or December ’17. So the last two years have really seen Cisco work to retake the all-time-high although 1% revenue growth wont get you there in a hurry.

The issue remains that “infrastructure platforms” is still 57% of Cisco’s revenue and is growing just low-single-digits at that. Applications and Security is 17% of Cisco revenue up from just 15% two years and while its growing at a faster rate than the old switching and routing business, it’s not fast enough to really move the needle for Cisco (yet).

Investors need a quarter or two quarters were Applications (11%) and Security (6%) really see robust growth that the Street thinks is sustainable.

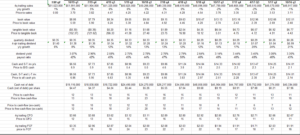

Clients currently hold a 1.6% position in Cisco and as a portfolio manager for individuals, The Kid is the perfect stock for a client accounts. The above chart shows Cisco vs the SP 500 since 1/1/2010 or the last decade, it’s under-performance isn’t too onerous (certainly nowhere near as bad as IBM’s), you get a decent dividend, and investors can be patient with Cisco.

If Cisco’s +/- 10% after Wednesday night’s call won’t matter much. The stock is a long-term hold and what I’m really interested in is whether Security and Applications can start to growth at a faster clip and reduce The Kid’s dependence on switching and routing.