With Schwab’s balance sheet restructuring, check out the changes in cash-flow generation for the discount-broker-cum-asset-management king, the last 3 years.

While some of this might be temporary, the cash-flow and free-cash-flow improvement means that Schwab (SCHW) COULD return more capital to shareholders over the next few years. Given the conservative nature of Schwab however, that doesn’t mean it will.

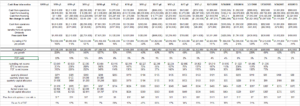

Here is the history of “Chuck’s” cash-flow generation:

Looking at the periods “pre balance sheet restructuring” which has resulted in the recent surge of cash-flow, but Schwab should be able to generate at least $1 billion to $1.5 billion in free-cash-flow every quarter, which would result in $4 to $6 billion annually.

(Readers can see from looking at the dividend and share repo section that Schwab went years without repurchasing any stock.)

The question is whether Schwab wants the dividend to be a bigger share of capital return or whether the Board wants to hold back more capital and use excess for share repurchases. Presently, the dividend is less than 10% of Schwab’s free-cash-flow while the pay-out ratio (less meaningful) is 25% of Schwab’s earnings per share.

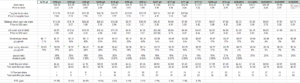

Chuck’s valuation

Note Schwab’s current cash-flow and free-cash-flow per share valuation and the free-cash-flow yield. (lines 692, 693, and 698).

Finally, here is a chart update on Schwab, from Gary S. Morrow (@garysmorrow), a great technician, posted last Friday, November 15th:

Summary / conclusion: Chuck has already endured the worst of the selling around the zero commission price war, but that bad news is masking many positives around Schwab’s balance-sheet restructuring and cash-flow generation. Even if we assume that the surge in Schwab’s cash-flow is somewhat temporary, “steady-state” assumptions still indicate Schwab will have more capital to return to shareholders over the next few years.

Morningstar retained Schwab’s “wide-moat” status after the zero commission headlines, and Schwab’s recent business update last week noted that Schwab’s “new accounts” rose 142,000 in October ’19, up 31% from September ’19 (yes, one month change) and rose 7% from October ’18.

For full and fair disclosure, Schwab has been this blog’s primary custodian since Day 1, in May, 1995, and there has never been need for another one, although at times I’m sure Chuck has wanted to strangle me (and I them). The support teams are great.

Schwab’s all-time-high was May ’18 near $58 per share. Calendar 2020 – per Street consensus – is looking for a slightly negative year in terms of revenue and EPS growth (-2% and -7% respectively) but let’s see if Schwab doesn’t use some of the excess capital to repurchase shares.

Finally a caveat for readers: typically Financial stocks do not traditionally get valued on “cash-flow” and free-cash-flow basis, but rather capital adequacy and return-on-equity. However Schwab, and the discount brokers like the exchanges, (CME, ICE), are more asset-intensive with volume driven over a fixed-cost-base. Schwab might have to retain some of that excess cash-flow to hold on the balance sheet to generate interest income, but some of that will also likely get returned to shareholders.

The bottom line is that the stock is substantially cheaper today with the worst of the price wars behind it. As Schwab works through 2020 the lowest expected growth it’s expecting in years, long-term investors should take an interest in the stock.

(Schwab has been the #2 holding for client accounts since just after the Great Recession ended 2009, early 2010. It’s a long-term holding and will remain so, although it’s position has slipped to #3 as JP Morgan has rallied and Schwab has traded lower on the zero commission price war.)

Thanks for reading.