John Butters of Factset noticed something that we picked up in our earnings data over the weekend, but since John wrote about it first, he deserves the credit.

Coming into q3 ’13 SP 500 earnings season, which starts next week, the expecetd earnings growth for the key benchmark for q3 ’13 is +4.6% year-over-year earnings growth.

Since mid-2012, as we have come into earnings season, y/y EXPECTED earnings growth the last 4 quarters has been closer to expectations of just 1% to 2%, as earnings season started, with actual earnings coming in much better.

The point is, as we await q3 ’13 earnings, already the revisions are less severe, and with 4.6% growth expected for q3 ’13, that is the highest pre-reporting growth rate we have seen since early 2012.

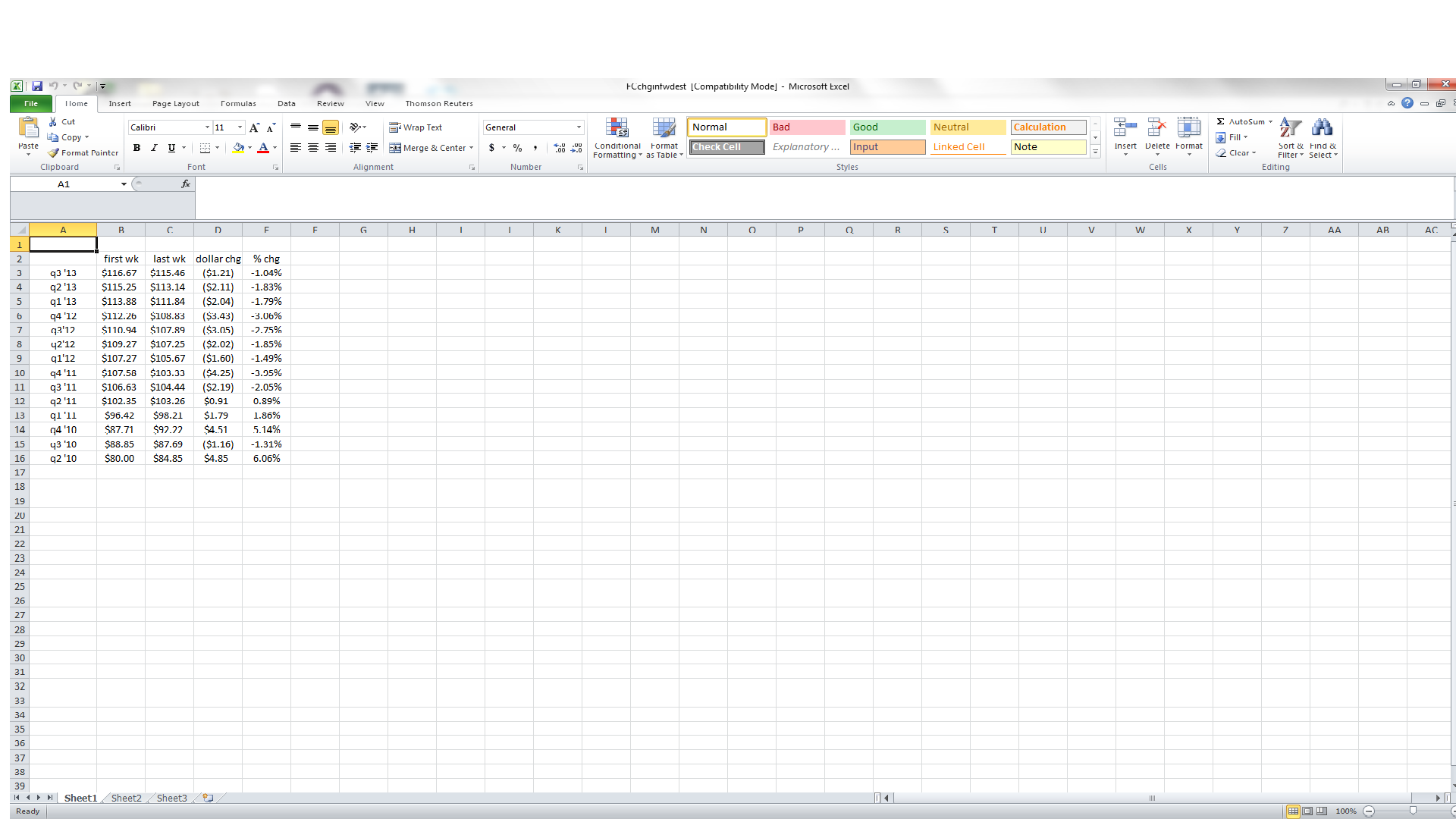

To show this graphically, on an Excel spreadsheet, we logged the “forward 4-quarter estimate” for the SP 500 as of the first week of each quarter, and then the last week, to show readers how the forward estimate progresses over each quarter.

Even with the forward estimate, as of the July – Septrember period of 2013, you can see that after the slump that started in early to mid 2012, the absolute decline in the forward estimate is getting less dramatic, and the dollar amount of change during the quarter is starting to lessen.

There is another metric we track on another Excel spreadsheet that shows the number of upward / downward revisions by week, that ThomsonReuters publishes. We intend to publish that by early next week.

The point of all this is that – using the ThomsonReuters data – we proved Facset’s conclusion that “Lower estimate cuts than average for the SP 500 for q3 ’13”, at least from a dollar and percentage perspective.

This entire rally in the SP 500 both with last year’s 16% return for the SP 500, and this year’s YTD return of 20%, has been with more absolute number of negative revisions than positive revisions, within the SP 500.

My own conclusion is that analysts remain spooked and very negative, and have no reason to stick their neck out and postively revise numbers until they see the data. Also, another reason could be that the large-cap and mega-cap names saw numbers cut dramatically in the earlier part of the decade, and given their cash-flow generation, stock buybacks are adding more growth than originally expected to earnings data.

This is navel-gazing at its finest, but we found it interesting and possibly a good tell for 2014.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager