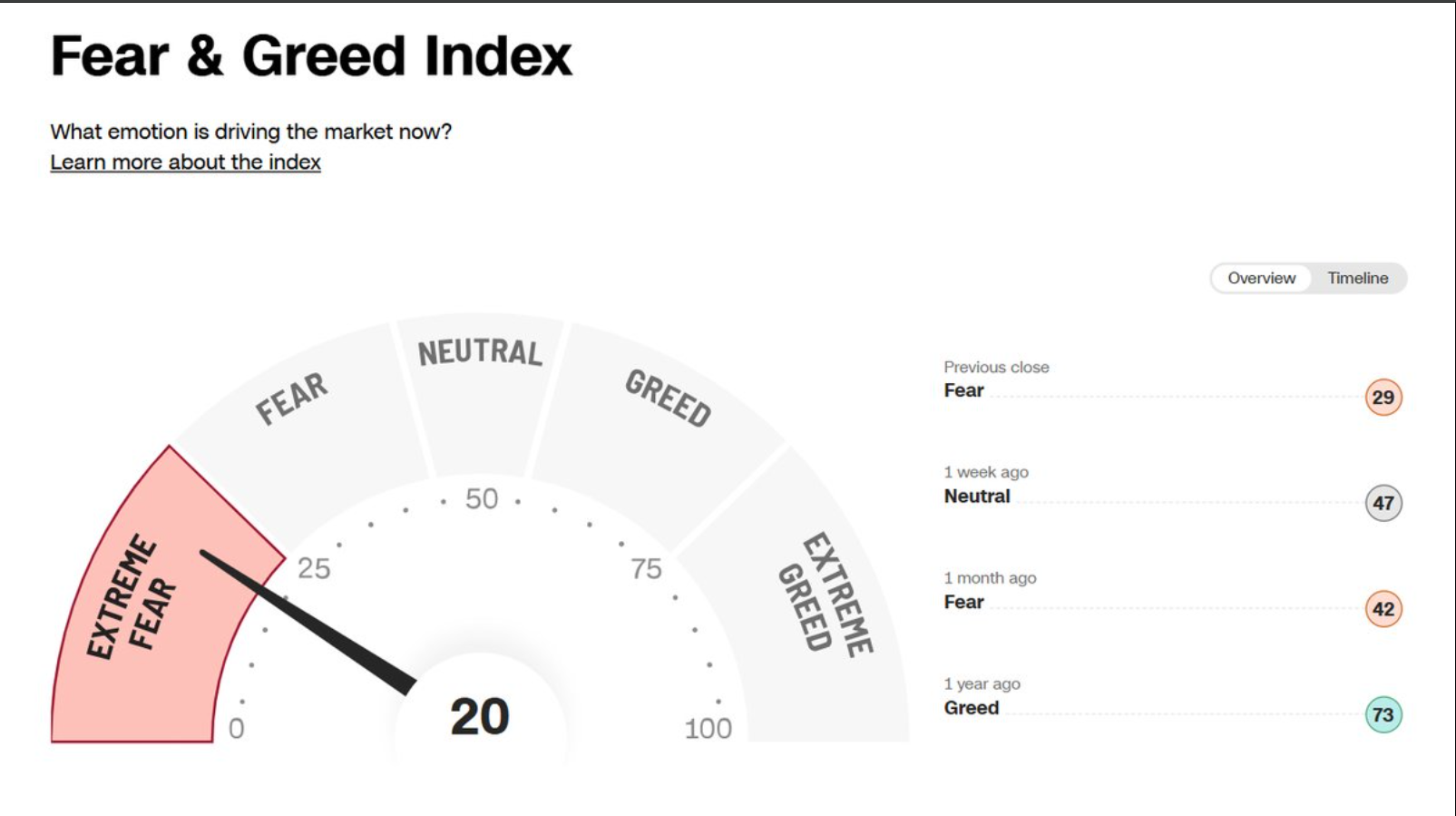

This index always catches the eye on X. This was posted last night, February 25th, 24 hours before the breathlessly-awaited Nvidia, fiscal Q4 ’25 earnings release, due today at 3:20 pm central.

The secular bull market we’ve seen since March 9, 2009, if it does end (and that’s not a prediction) with a definite whimper, if the Nvidia earnings release tonight is disappointing.

Microsoft’s stock is already wobbly from looking at the chart.

This is all a bit extreme, though, i.e. the talk of secular bull markets coming to an end.

The SP 500 could be due for a healthy rotation, given how Europe and some international markets are acting relative to the SP 500.

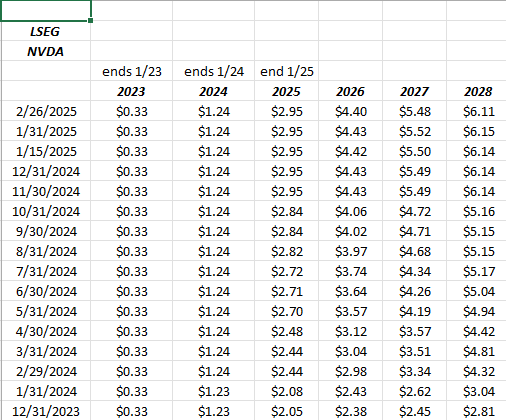

Nvidia estimates and estimate revisions:

LSEG, this blog’s primary EPS and revenue estimate source is expecting $0.75 and $38.05 billion in revenue tonight, while Briefing.com, is expecting $0.85 in EPS on $38.1 billion in revenue for Nvidia’s fiscal Q4 ’25 results. Versus EPS of $0.52 a year ago, Nvidia EPS growth is expected at +63% y-o-y tonight, while revenue growth is expected at 73%. (It’s suspected that LSEG is using a GAAP EPS number, while Briefing.com is using expected “operating” EPS for NVDA.)

NVDA EPS estimate revisions:

Looking back to July – August ’24, when the Nasdaq looked it was “peak sentiment”, the fiscal 2025 through 2028 EPS estimates have shown a roughly 10% – 20% cumulative positive revision since that time.

Looking at the above table, if readers would measure the rate of EPS estimate revision from 12/31/23 through 8/31/24, the positive revision rate is much higher:

Let’s look at the cumulative EPS estimate revision for NVDA in two different periods:

Fiscal ’25:

- NVDA cumulative EPS change from 8/31/24 to 2/26/25: +5%

- NVDA cumulative EPS change from 12/31/23 to 8/31/24: +38%

Fiscal ’26:

- NVDA cumulative EPS revision from 8/31/24 to 2/26/25: +11%

- NVDA cumulative EPS revision from 12/31/23 to 8/31/24: +67%

Fiscal ’27:

- NVDA cumulative EPS revision from 8/31/24 to 2/26/25: +17%

- NVDA cumulative EPS revision from 12/31/23 to 8/31/24: +91%

Fiscal ’28:

- NVDA cumulative EPS revision from 8/31/24 to 2/26/25: +19%

- NVDA cumulative EPS revision from 12/31/23 to 8/31/24: +83%

This blog has never followed NVDA fundamentally or built the valuation models that are typically done for individual stocks, held for clients.

Thus, the demand for the Blackwell chip and the stressed production might have caused some of this pullback in analyst optimism in the last 6 months.

I couldn’t help noticing the slowing in the estimate revisions over the last 14 months.

One other event that caught my attention was the 10-for-1 NVDA stock split in June ’24: when Alphabet and Amazon (and I thought there was one other stock, maybe Tesla, but it was a 3-for-1 split) did 10-for-1 splits in the summer of 2022, the stocks didn’t make new all-time-highs for some time.

Summary / conclusion: This blog has no positions in Nvidia currently. When NVDA blog post in early January ’25 was published, and Seeking Alpha picked up the post, (here’s the www.seekingalpha.com version of the post with comments) there was pushback on the suggestion that Nvidia’s EPS growth may be slowing.

I have to say it since it really left an impression on me at the time, but I thought it was Sam Altman, one of Evercore’s top executives, who mentioned that he thought Nvidia could ultimately have a $15 trillion market cap, which, although the two aren’t directly comparable, left an impression since that would be roughly half the USA’s annual GDP growth every year. This was a similar discussion to what was said about Coca-Cola’s stock price return (and growing market cap) from the late 1980’s to the late 1990’s: I think it was the Motley Fool within a few years of Cola stock peaking (July ’98 to be exact) who published an article that said Coca-Cola’s market cap could eventually be greater than the US economy at the time, (the Buffett holding got a lot of attention as blogs, and the internet exploded in the mid to the late 1990’s), although that was 25 – 30 years ago, and I can’t recall the exact publisher of the article.

The final aspect that strikes me about NVDA’s business model, is that it’s hardware, and a production enterprise, and if you look at what happened to hardware stocks like Intel and Cisco in the early 2000’s (neither Intel or Cisco has traded back close to their all-time-highs from the year 2000, and this is 25 years later), while Intel and Cisco generated ample free-cash-flow during the late 1990’s halcyon days, once the market shifted, it wasn’t good.

Enviable and seeming impenetrable moats in one era, become achilles heels in the next disruption. Just ask Cisco and Intel.

This post will surely generate it’s share of vitriolic commentary, but I did not mention at all Nvidia has peaked. Nvidia’s success could go on for a while. The stock’s overwhelming popularity amongst retail investors just gives me pause. Many bulls were very right on the stock.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal, even over short periods of time. LSEG is the source of all EPS and revenue estimates, except where noted. The information above may or may not be updated, and if updated may not be done so in a timely fashion.

Thanks for reading.