It’s a busy week for economic data, both monthly and quarterly, as well as the all-important FOMC statement on monetary policy due out Wednesday afternoon, July 31.

On top of that Microsoft releases their fiscal Q4 ’24 earnings Tuesday, July 30th ’24 after the closing bell.

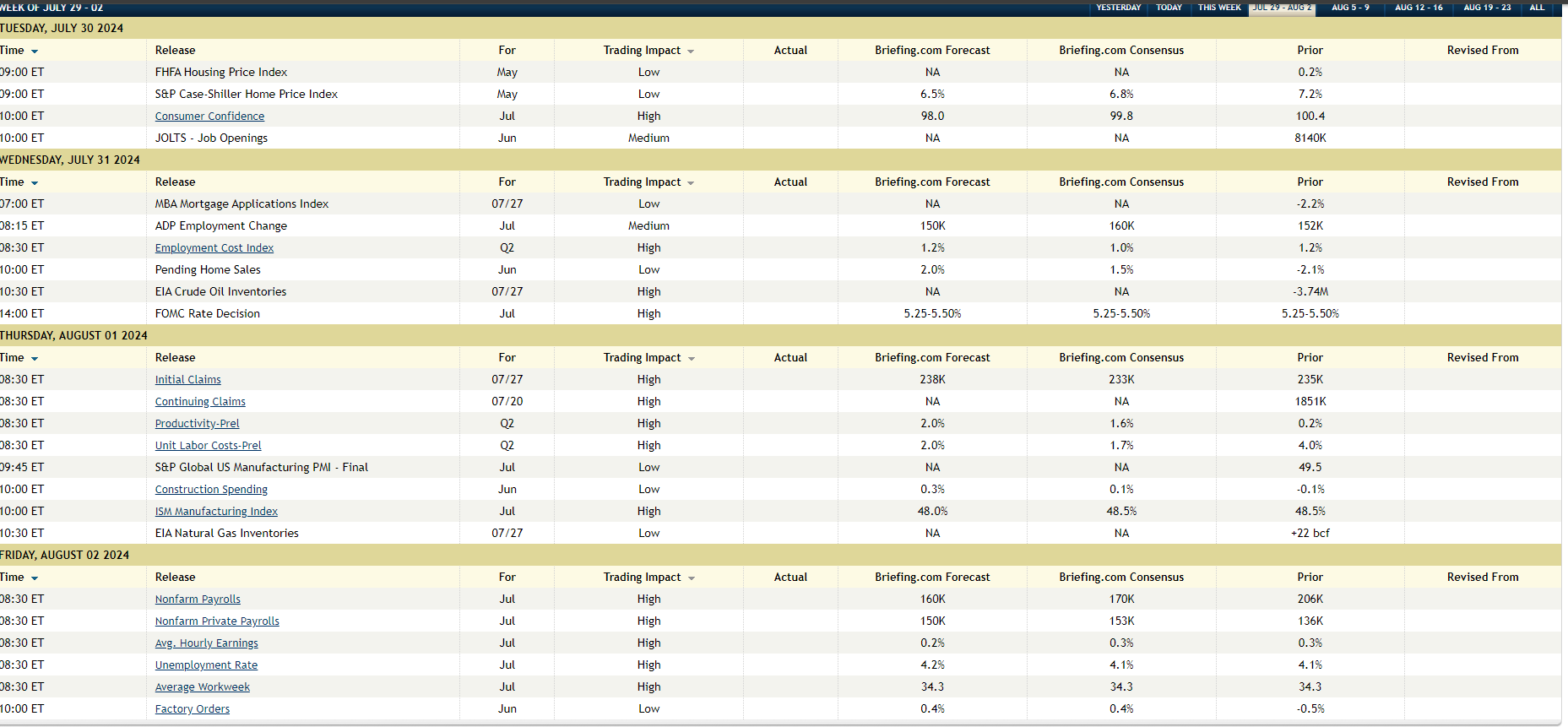

Briefing.com publishes a neat little summary of the pending economic data releases for the coming week. The above table shows what’s coming for “nonfarm payroll week” beginning July 29 ’24.

The 6 releases this week that are “jobs-related”:

- June JOLTS report due out Tuesday morning, July 30 at 9 am central;

- The first look at Q2 ’24 Employment Cost Index is scheduled for Wednesday morning, July 31 at 7:30 am;

- The June ADP release is due out July 31 at 7:15 am central time Wednesday morning;

- Weekly jobless claims due out Thursday morning, August 1 at 7:30 am central;

- Also due Thursday morning, July 31 at 7:30 am is Q2 ’24 Unit Labor Costs and Productivity;

- The June nonfarm payroll report due out Friday morning, August 2nd at 7:30 am;

This is just a personal opinion, but I believe the Fed / FOMC / Powell are waiting for some “below-average” jobs data, meaning a weaker non-farm payroll report (-100,000 or more) and a weekly jobless claims figure that moves convincingly over 255k – 260k, before this persistent and never-ending discussion of fed funds rate reductions move from constant speculation to statistically probability.

Most Fed watchers think a September fed funds rate cut is now probable, but that will disappear quickly on Friday morning, August 2nd at 7:30 am, if the “net new jobs added” to the US economy is greater than 225,000.

The fact is the jobs market has been quite stable, as has housing (nationally), and retail sales (consumption), it’s probable the constant pre-occupation about monetary policy could continue, with nothing ever being resolved.

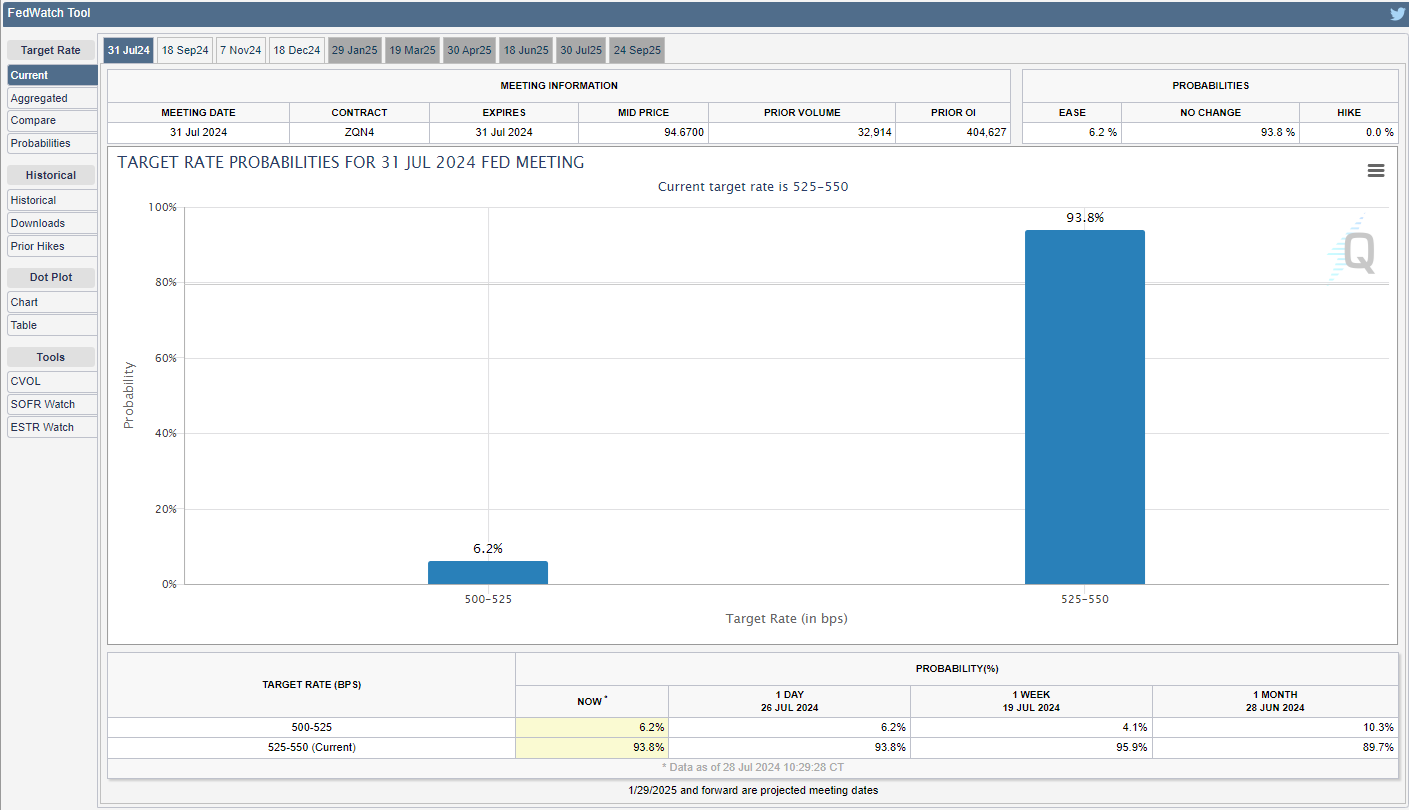

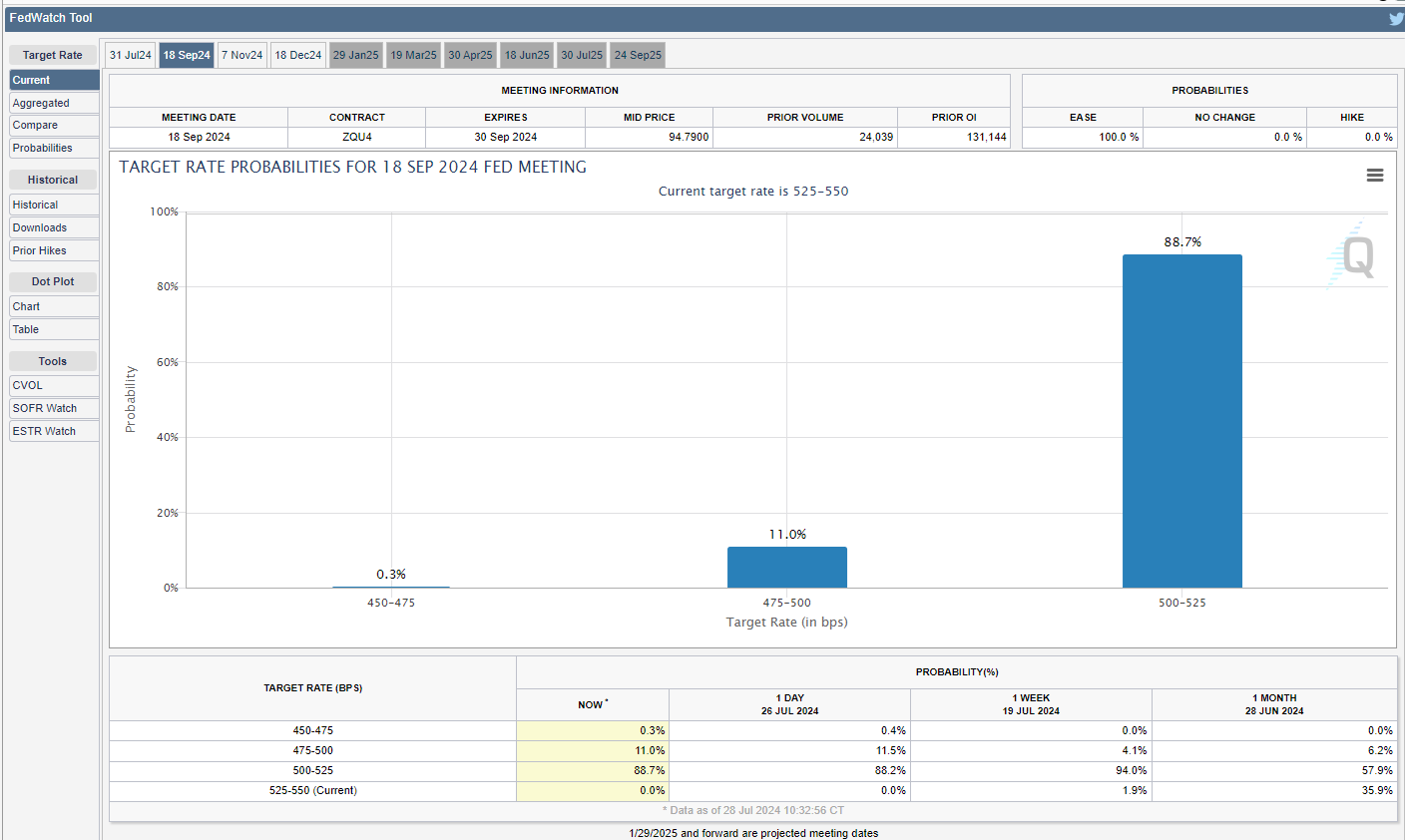

What’s really interesting from the CME FedWatch (Fed funds futures market):

The July 31 meeting statement is expected to affirm the 5.25% – 5.50% (5.375%) current fed funds range. But let’s now look at the fed funds futures for September ’24:

There is presently an 88% chance – per the CME fed funds futures – that the fed funds rate is reduced by 25 bp’s at the Sept ’24 meeting.

Watch what happens to Sept ’24 fed funds futures with the nonfarm payroll data that is due out Friday morning, August 2nd. While all the other data does matter to some extent, it’s the nonfarm payroll report (business survey) and the unemployment rate (household survey) that have a bigger influence on monetary policy decisions.

The fact is that 88% chance of a 25 basis point fed funds rate reduction could dissipate quickly with stronger numbers Friday morning, just like the 6 – 8 fed funds rate cuts that we started 2024 with in December ’23 and January ’24.

SP 500 earnings data: (accidentally omitted from Friday’s, July 26th SP 500 earnings update):

- The forward 4-quarter estimate for the SP 500 (FFQE) fell sequentially to $259.84 vs the $260.40 last week, and the $261.39 to start the quarter on July 5 ’24, so the unusual string of SP 500 weekly sequential increases that we saw from April – June ’24, may be starting to dissipate;

- The PE on the forward estimate was 21x this week, versus 21.2 last week and 21.6x on June 30 ’24 (not enough of a difference to be material);

- With 206 companies having reported Q2 ’24 earnings for Q2 ’24, the “upside surprise” is lower than in previous quarters, at +4.4%, versus +8% in Q1 ’24, and +7.9% in 2 ’23.

- The “upside surprise” is heavily influenced by the mega-caps though, so this week matters with Microsoft, Amazon, and Meta reporting.

- SP 500 revenue “upside” surprise” is consistent with past quarters as is the ” % above” and “% below” consensus;

- 171 SP 500 companies are expected to report this coming week, which means 377 companies will have reported Q2 ’24 results by Friday morning, August 2nd, ’24;

The Friday, July 26th S&P 500 Earnings data post (linked above) was simply me trying to explain that we could have decent SP 500 earnings from the SP 500 mega-caps and the tech sector but still lower stock prices since “capex” has a bigger impact on valuation than earnings (at least presently given the AI push), so readers should be made aware of that dynamic. Discounted cash-flow valuations are not perfect by any means, and when I had to do one in business school, and saw that small changes in the growth rates could lead to large changes in individual stock valuations, I (foolishly) discounted (no pun intended) the DCF model, when in fact, it’s the process and discipline of building the DCF the model that is the real “education” so to speak.

Summary / Conclusion:

Before the Super Bowl LVIII on Sunday, February 11th, 2024, 60 Minutes aired an interview with Jerome Powell, and the current Fed Chair – when asked by Scott Pelley what the Fed paid most attention to, Jay Powell responded (reportedly), “Jobs, jobs, jobs”.

The problem with financial media is that every economic release is treated like Moses coming down from the mountain, when in fact it’s job data that really drives Fed monetary policy. And it makes perfect sense too, since jobs drives income(s), and income drives consumption (i.e. spending) and consumption and spending are 2/3rd’s of GDP. When America is employed and can find employment, she is considerably less restless.

This week is chock full of labor market and wage data for economic geeks like myself.

Personally my own opinion is that Powell is itching to get back to a “normal” yield curve (fed funds rate below the rest of the Treasury yield curve), since it’s the equivalent of the rear-naked-choke (brazilian jiu jitsu reference), for the banking system. While the larger banks that were absolutely crushed in 2008 are much better off today than given the capital reforms, etc. it’s the regional banks that are feeling the pinch of a 5.375% fed funds rate, while the 2-year and 10-year Treasury yield bounce around between 4% and 5%.

For what it’s worth, what the September ’24 CME fed funds futures bar chart (www.cmegroup.com) FedWatch, and you’ll know if the FOMC and Jay Powell have greater or lesser conviction around a 25 basis point reduction in September ’24. The fact is that fed funds reduction could become 50 bp’s quickly.

None of this is advice or a recommendation, simply an opinion. Past performance is no guarantee of future results. Investing can involve loss of principal, even for short periods of time. All EPS and revenue data around SP 500 earnings is sourced from LSEG.

Thanks for reading.