With Walmart (WMT) reporting this past week, it’s thought the Q1 ’24 earnings season has officially ended, but with Nvidia (NVDA) scheduled to report their quarterly results on 5/22/24 after the closing bell, earnings season has likely been extended for another week.

Nvidia is the new stock market darling.

SP 500 data:

- The forward 4-quarter estimate slipped a little this week to $252.93 from last week’s $252.99, and vs the $243.98 that started the year.

- The PE on the forward estimate is now 21x versus the 20.6 x last week, and the 21x PE that started the year.

- The SP 500 “earnings yield” is 4.77%, vs the 4.85% last week, and the 5.19% that started 2024.

- The SP 500 EPS “upside surprise” is was +8.2% this week. Let’s have a look at how the upside surprise for SP 500 earnings has progressed over the last 5 weeks:

Progression of SP 500’s EPS upside surprise:

- 5/17: +8.2%

- 5/10: +8.3%

- 5/3: +8.4%

- 4/26: +9.5%

- 4/19: +10.1%

SP 500 EPS upside surprise over last 4 quarters:

- Q1 ’24: +8.2%

- Q4 ’23: +6.3%

- Q3 ’23: +7.2%

- Q2 ’23: +7.9%

Those are healthy numbers, both the last 5 weeks and the last 4 quarters.

StyleBox Update:

Click on the above spreadsheet, to see relative and absolute performance of the “styles” from large-cap growth to small-cap value.

The numbers that jump out to me are the “3-yr” annualized returns at the bottom of the spreadsheet. Those 3-year annual returns still appear rather modest in what mostly “above-average” historical returns across all styles.

The return data is sourced from Morningstar, and I wish we could get 20, 25, and 30 year returns (just for perspective) as well.

These two blogs posts (here and here) which are updated monthly, showing the 23-year annual return for the SP 500 (Jan 1, ’00 through 4/30/24) being just over 7%, and bond asset classes reflecting the horrid drawdown and returns since the Fed started raising the fed funds rate in March, ’22.)

Those style-box annual equity returns are not bullish for prospective, forward, stock market returns in the least.

The other point that readers need to be aware of, is that any poster, author, or blogger, or investor can show data that makes markets look fabulous or horrid. just by changing the starting point of the data. Caveat emptor.

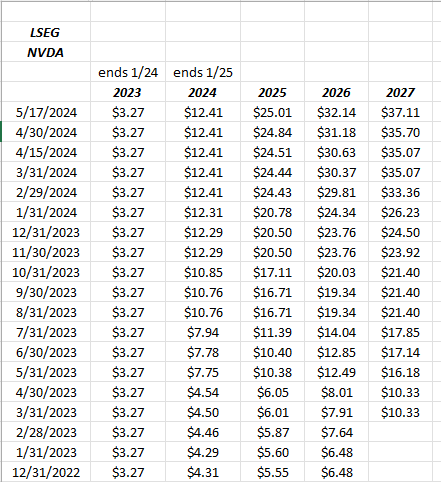

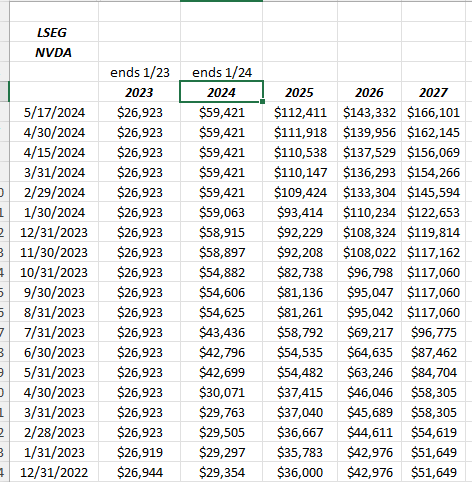

Nvidia’s EPS and revenue estimate revisions:

No Nvidia is owned directly for clients, but rather clients are long NVDA through the SMH (semiconductor ETF) which as of Friday, May 17 ’24, shows that NVDA is a 20.8% weighting in the SMH. As of Friday, May 17th, NVDA is up 86.75% YTD, while the SMH is up 31.75% YTD.

NVDIA reports their fiscal Q1 ’25 this week:

What’s interesting about NVDA’s EPS revisions, is that for 2024, which just ended in January ’24, the two-year EPS increase was roughly 200% ($12.41 vs $4.31 start), while fiscal ’25, which investors will get the first look at Wednesday night, has shown a 351% increase ($25.01 vs the $5.55 starting estimate) for the same period.

NVDA’s revenue estimate progression is similar. If you’re a momentum investor, you love these numbers.

The goal was to show the estimate revisions to readers: not making any judgment on these numbers or the valuation in any way.

Nvidia matters greatly this week, it’s the stock market darling since Apple fell out of favor and lost it’s momentum. SP 500 earnings continue to be rock solid, but pay attention to the sectors too.

With the stock market as complacent as it is, it wouldn’t require much to unsettle the SP 500 and the Nasdaq. Bad body language from Jensen Huang, unexpectedly conservative guidance from NVDA, it wouldn’t take much to generate a 5% correction here. However, banking on that and trading for it, (i.e. raising cash) means an opportunity cost of missing out on more capital gains, if nothing materializes.

JPMorgan broke out this week, above it’s previous $200 high. JPM did it in a very quiet fashion too as Amazon slid lower after taking out it’s July ’21 all-time-highs around $189, and then sliding back.

Microsoft is trading below it’s all-time-high too: I watch these levels as the indices make new all-time-highs since it gives a relative strength perspective.

The question is will NVDA give tech and mega-cap stocks another jolt higher this week with Q1 ’25 earnings ?

Summary / conclusion: The aspect of this equity market rally that is surprising is that it lacks any of the frenzied trading we saw in the late 1990’s as well as late as in late 2017, early 2018 (there was a big VIX spike in early 2018), and then again in 2020 – 2021 with SPAC’s and bitcoin and crypto. The meme stocks popped in the last 10 days, and fizzled just as fast.

Personally, it’s a little worrisome that Microsoft and Amazon are starting to lag. Microsoft updates the Street this week on AI initiatives via Microsoft Build (developers conference ?), which presumably will / might include some commentary on CoPilot’s adoption rate ? CNBC did a 5-minute segment on Friday, May 17th, on CoPilot that talked about users possibly balking at the $30 per month price tag. Don’t remember the name of the reporter but I thought it was timely and well done. CoPilot launched in mid-November ’23; don’t remember management saying much about it on the April ’24 earnings conference call.

This blog’s technician (X – @GraySMorrow) flagged the decent technical action in EEM and VWO last week, the emerging market ETF’s that also hold China companies. Clients are long only EMXC (Emerging markets ex-China ETF). China is uninvestable in my opinion.

It doesn’t seem to get much press, but there is a definite “broadening” in the market action to some out-of-favor sectors. That’s probably a healthy sign.

Bespoke noted in their fixed income weekly Wednesday of this past week, that they thought the Treasury market rally had more steam left in the tank (so to speak). Last week’s blog picked up some Bespoke work from May 1, which showed inflation’s correlation to crude oil.

A drop in crude oil through $70 price level would be very bullish for Treasuries (and thus equities) in my opinion.

None of this is advice or a recommendation. Past performance is no guarantee of future results. Investing can involve the loss of principal, even for short periods of time. All SP 500 (and individual company) EPS and revenue date sourced from LSEG.com. Readers should gauge their own comfort level with portfolio volatility and adjust accordingly.

Thanks for reading.