Capex: FASB – the Financial Accounting Standards Board – defines “capex” as “the investment required to sustain the economics of a business”. Capex is not an expense, i.e. a deduction from revenue, but rather is a “capitalized” item that shows up on the statement of cash-flow in the “investing” section, and before the 1980’s services economy exploded, was traditionally “payments for property, plant and equipment” that weren’t expensed, but capitalized, and then depreciated over the useful life of an asset. (CPA’s and PhD’s in Accountancy, please forgive me, and this opening paragraph. The goal is to give readers a quick lesson in in investing and accounting jargon and then further explain why all this is necessary. I am NOT an accountant or CPA, and don’t pretend to be one, but it’s important to lay a foundation for what’s to follow.)

First, before getting into the nitty gritty of valuation, readers should probably understand that the traditional “financial analyst” whose curriculum and body of study was first developed by the Chartered Financial Analysts (CFA) Society in the early 1960’s, has always worked from, or always started with the understanding that the analyst begins his or her analysis with the audited financials or quarterly earnings report, and then builds a valuation model from the basic financial statements.

I probably talk about it too much on this blog, but to explain to readers what a speculative frenzy (for lack of a better word) the late 1990’s were, and how far business accounting drifted from any sense of reality, in the midst of the large-cap growth and technology bubble of the late 1990’s, readers should know that after Enron, Worldcom, and Tyco blew up, Arthur Andersen & Co. Inc. – arguably the global accounting firm with the best reputation for it’s accounting expertise – was CRIMINALLY indicted for it’s Enron document destruction activities, only to later have the indictment overturned by the Supreme Court. However, the reputational damage was done, and probably the greatest accounting firm in the post WW II period, with a pristine accounting reputation, was completely destroyed. (Arthur Andersen was a partnership, just like a lot of law firms, and I often wondered what happened to the old partners that had 100% of their wealth still tied up in the firm when it went south. I don’t recall reading any post mortem’s on Arthur Andersen and what it meant for partners after the firm went under, although I can’t believe many were willing to discuss it publicly.)

The point being that in the post 2001 – 2002 world (read Sarbanes-Oxley) accounting returned to it’s more rational and sleepy domain as did management’s who in the late 1990’s were really trying to stretch the bar in terms of accounting principles and accounting reality. The other point being that if the financial statements are bad, then the stock or bond – as a long-term investment – will be bad too.

SP 500 earnings quality today is generally quite good as borne out by the “cash-flow to net income” comparison. Someone will put up an argument, but the fact is that earnings quality is still high relative to what was seen in the 1990’s.

First, let’s look at Apple: Apple announced Thursday night, May 2nd, 2024, that their plan was to – over time – buy back an additional $110 billion in common stock, which was pretty amazing given the size of that buyback.

Stock repurchases and dividends are paid from free-cash-flow. Here’s a look at Apple’s trailing-twelve-month (TTM) free-cash-flow (FCF):

![]()

Readers can see that since the December ’21 quarter, the TTM free-cash-flow has basically been flat.

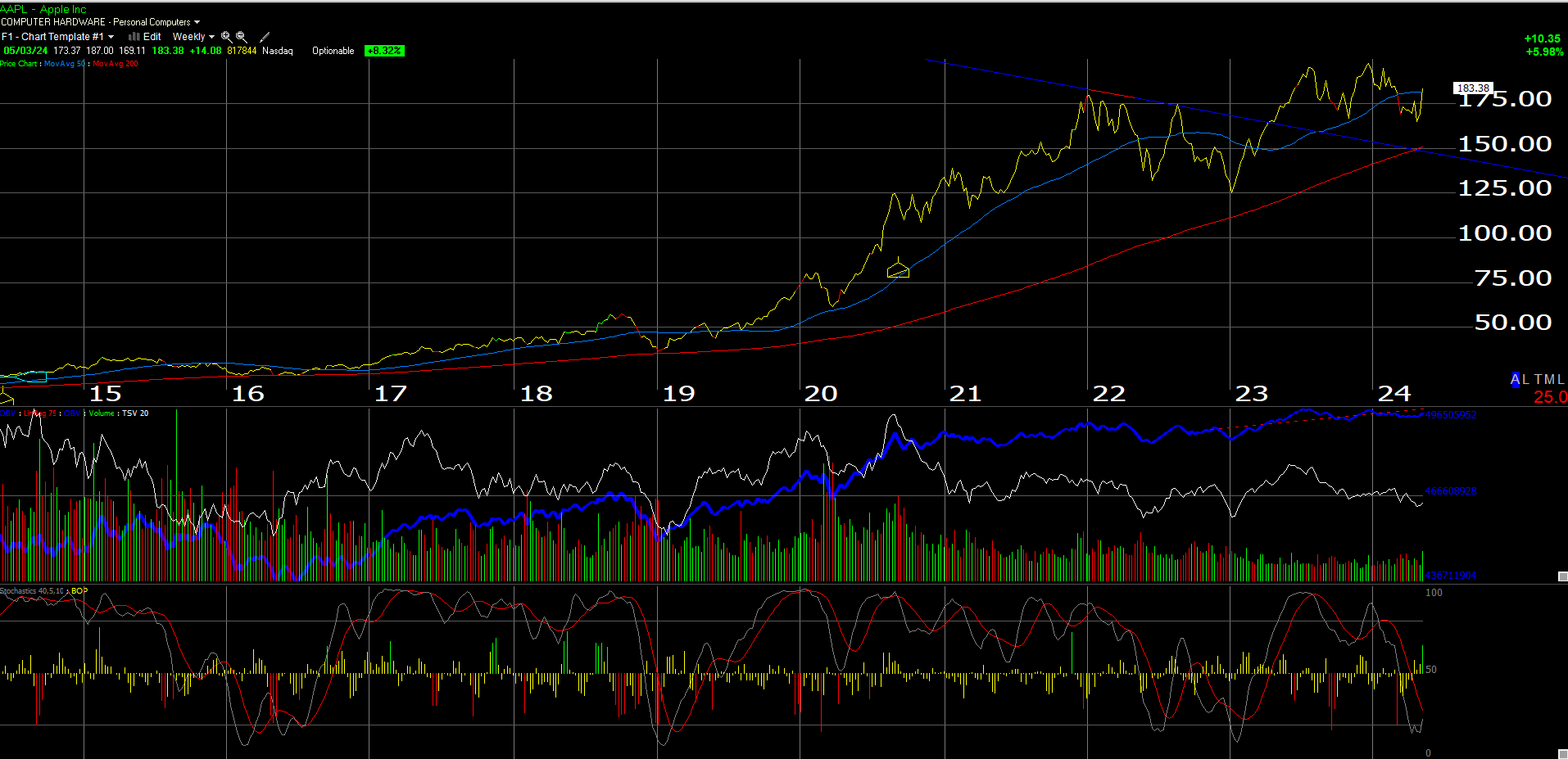

The interesting aspect to this is that looking at the Apple weekly chart, the stock first started to flatline as of the December ’21 quarter.

Note the stock’s price behavior prior to and then starting with the December ’21 quarter.

That’s not the point of this Apple note though. When a company like Apple starts paying out much of it’s capital, the common conclusion that long-term investors usually make is that growth opportunities have dried up, and the company is returning capital to shareholders because they cannot earn a return on that capital, greater than their cost-of-capital, thus returning capital via dividends and share repurchases is usually chosen by management the board of directors.

![]()

The above spreadsheet shows the TTM dividend and buyback for AAPL and it’s percentage of free-cash-flow.

The point being Apple has been paying out all of it’s excess capital for some time.

Does Thursday night’s Apple buyback announcement, portend a lack of reinvestment opportunities for the core business ? Probably not. But I do think that Apple’s AI announcement this coming week has to get the attention of the Street (sell-side analysts and investment community) and it has to leave the impression with the investment community that AI means a new, credible, growth opportunity.

You could easily make the case that Apple is a mature business. Android is still viable competition, but I’ve always thought Tim Cook – given he succeeded Steve Jobs – was always underrated as a CEO. It’s unclear why AAPL followed the strategy they did with VisionPro, (the AR/VR headset) since it already looks like a bust.

Apple annual returns versus SP 500 annual returns:

- 1-year: Apple’s +0.95% vs the SPY 22.4%

- 3-year: Apple’s +9.6% vs the SPY 7.91%

- 5-year: Apple’s +28.3% vs the SPY 13.09%

- 10-year: Apple’s +23.7% vs the SPY 12.30%

- 15-year: Apple’s +27.8% vs the SPY’s 14.5%

The returns are sourced from Morningstar as of 4/30/24.

It’s only for the 1-year return period that Apple has underperformed the SP 500.

Will AI’s capex surge reduce technology stock valuations ?

Finally, regarding the AI capex strain that many of the mega-cap 7 have reported from much higher capex guidance over the next few years, it’s still all about free-cash-flow. Now free-cash-flow is a simple equation starting with cash-from-operations, subtracting capex, which then determines free-cash-flow, so if all else is kept equal, then higher capex for these tech companies could result in lower free-cash-flow for longer periods of time, and that could lower valuations for the technology sector.

Lower free-cash-flow estimates (and lower actual free-cash-flow) going forward will present a market environment where technology stocks PE’s “contract” rather than expand.

Don’t be surprised if the mega-cap 7 or mega-cap 10 stocks trade listlessly for a few quarters as the true “capex” is worked out.

Summary / conclusion: The AI explosion and the expected capex surge could impact the mega-cap stock space. All other things kept the same, higher capex means lower free-cash-flow going forward and that could impact valuation.

Clients haven’t owned Apple as a major top 10 holding since 2017 – 2018, when President Trump put tariffs on China. My fear was that this would boomerang back on Apple, but that call was way too early, since it was Tik-Tok and Ukraine which seems to have cooled the relationship between American businesses selling in China and Xi JinPing. It’s not just Apple either, but Tesla, Nike, Pepsi, and a few others.

The Apple announcement around AI will be critical: back in 2013, after what was then the Facebook IPO, the stock meandered from the mid $40’s down to the low $20’s until Facebook’s July, ’23 conference call when Zuckerberg announced that the firm was pivoting to the mobile app (as opposed to the desktop) and the stock took like a rocket and ended 2023 near $60 per share. Same with Tesla, the pivot to the low or “Model 2” hasn’t driven a huge rally, but it’s stopped TSLA from falling further.

The problem like March, 2000, is when the tech companies have nothing to pivot to, but today that pivot is really AI, and what will likely multiple derivations of AI in the coming years. Apple needs to be involved in this somehow and be able to articulate the strategy to Wall Street.

None of this is advice or a recommendation. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time.

Always appreciate readers taking the time to read the article.