Very few have noticed that Walmart (WMT) has traded to an all-time-high before the e-commerce juggernaut Amazon (AMZN) has done so. The 3-for-1 stock split recently likely helped Walmart push above it’s previous all-time-high of $56 and change last November ’23, as it trades tonight around $59.

Amazon hit an almost perfect “double-top” at $188 in July and November ’21, and has yet to recover that level in the 27 months. It’s getting close, but it’s not there yet.

Very few noticed too that Jeff Bezos’ CEO resignation occurred right around the July ’21 earnings report, so Jeff “top-ticked” his own stock with his resignation.

Quick recap of Walmart and Amazon earnings reports:

In Walmart’s earnings preview, this blog talked about WMT being a margin story, but fiscal Q4 ’24 was a gross margin story, with GM increasing 122 bp’s y.y, to 23.97% from Q4 ’23 22.75%, rather than an operating margin story, which is what AI and supply-chain enhancements will deliver. To be frank, I was right for the wrong reasons, but the margin story is just getting started.

Gross margin was helped by advertising which in the conference call notes, it was noted that advertising grew 28% y.y to $3.8 billion, still a small part of overall revenue, but it does fatten Walmart’s margins.

Here’s an important comment on the conference call on grocery inflation (sourced from TheTranscript):

![]()

Here’s what jumped out about Walmart’s metrics:

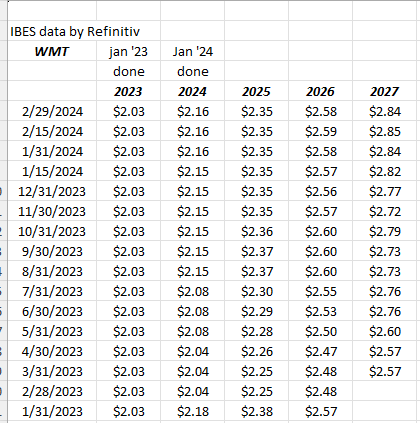

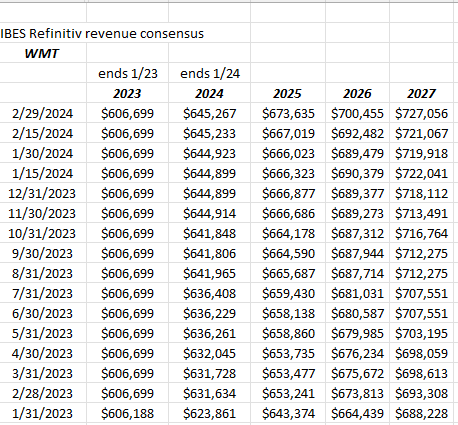

Walmart management offered very tepid earnings guidance for their fiscal ’25 (ends Jan ’25), and it’s showed up the last two weeks in very little interest in raising ’25, ’26 or ’27 EPS estimates.

However, note the steady progression upward in Walmart revenue estimates, even after the “deflationary position” referenced above in TheTranscript note.

Analysts are not shy about raising Walmart’s revenue estimates for the next few years.

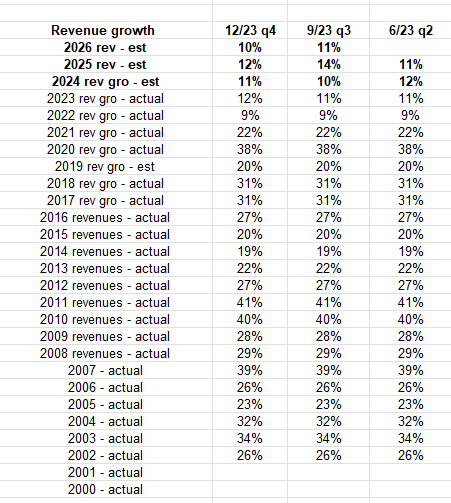

Summary / conclusion: Walmart is JUST coming out of the 2021 and 2022 excess inventory issue, meaning it’s just the last few quarters that there has been a return to normal balance sheet and cash-flow metrics. For a secular “mid-single-digit” revenue grower and “high-single-digit” operating income and EPS grower, Walmart can continue to take share in grocery – grocery grew mid-single-digits y.y in the Jan ’24 quarter – Walmart will need the margins to drive additional growth.

Amazon: great quarter, stock still trading below all-time-highs

Amazon put up good growth in Q4 ’23 against a tougher quarter in Q4 ’22, but here’s the bigger, longer-term, change in Amazon for readers:

Amazon grew revenue growth y.o.y at a greater than 20% rate from 2000 to 2021 (one exception), but that revenue growth looks to have permanently slowed to half the previous two decades pace.

It’s manageable, as Amazon too (like Walmart) is focusing on margin.

Advertising and AWS drove Q4 ’23 for Amazon with a big upside beat in operating income for the ecommerce giant. Operating income of $13.2 billion beat the consensus of $10.4 billion (LSEG) generating a 26% upside surprise.

Morningstar noted that Amazon’s 7.7% operating margin was the best for the 4th quarter in a decade.

Summary: No valuation talk in this post, rather it was just a note to highlight Walmart’s leadership relative to the SP 500 and how Amazon lags. Are we entering a period, where – despite the Mag 7 status – Amazon, Alphabet and Apple, are becoming mature businesses and the “growth” mantle is being passed to other sectors like the AI stocks ?

Another metric I thought was interesting: Amazon generated $575 billion in revenue in calendar ’23, and with it, cash-flow from operations for the same period was $85 billion. Walmart generated $648 billion in fiscal ’24, and with it, cash-flow from operations for the same 12 months was $36 billion.

Amazon still has the more efficient asset base, but Walmart is closing the ecommerce gap.

None of this is advice or a recommendation. Past performance is no guarantee or suggestion of future results. Investing can involve the loss of principal, even for short-time periods. Readers should gauge their own comfort with portfolio and individual stock volatility, and adjust accordingly.

Thanks for reading.