The big banks don’t report until Friday, January 12th, 2024, but it might help to throw JPM’s earnings preview out early for readers, given the stock is within a $1 or $2 of it’s October, 2021, all-time-high of $172.96 per share. A close above $173 with a little volume, would be a very good sign for JPM bulls (of which I am one), contingent on the SP 500 also making all-time-highs with it.

- For Q4 ’23, consensus sell-side estimates are expecting $3.43 in earnings per share on $39.78 billion in revenue for expected year-over-year (yoy) growth of -4% and +15% respectively. JP Morgan has a tough compare against Q4 ’22 strong earnings report which printed $3.75 in EPS one year ago. (That $3.43 estimate has slid lower from $3.66 in mid-October ’23.)

- For Q1 ’24, the current consensus is $4.18 on $41 billion in revenue for expected yoy growth of 2% in EPS and 7% in revenue.

- For calendar ’24, the current consensus is expecting full-year EPS of $15.75 on $159 billion in full-year revenue for -5% decline in EPS on a -1% decline in revenue.

In Q3 ’23, better-than-expected credit performance and net interest income (NII) drive the 10% EPS upside surprise, as well as decent expense control.

If JP Morgan hits the consensus estimates, the big bank will have printed $16.23 in full-year ’23 earnings per share, a new record for the bank giant, surpassing 2021’s $15.34 in EPS, on $160.6 billion in revenue (also a new bank record), part of which is also due to the big acquisition of First Republic, one of the bank’s affected with the same affliction as Silicon Valley Bank (SIVB), which went bankrupt in March ’23.

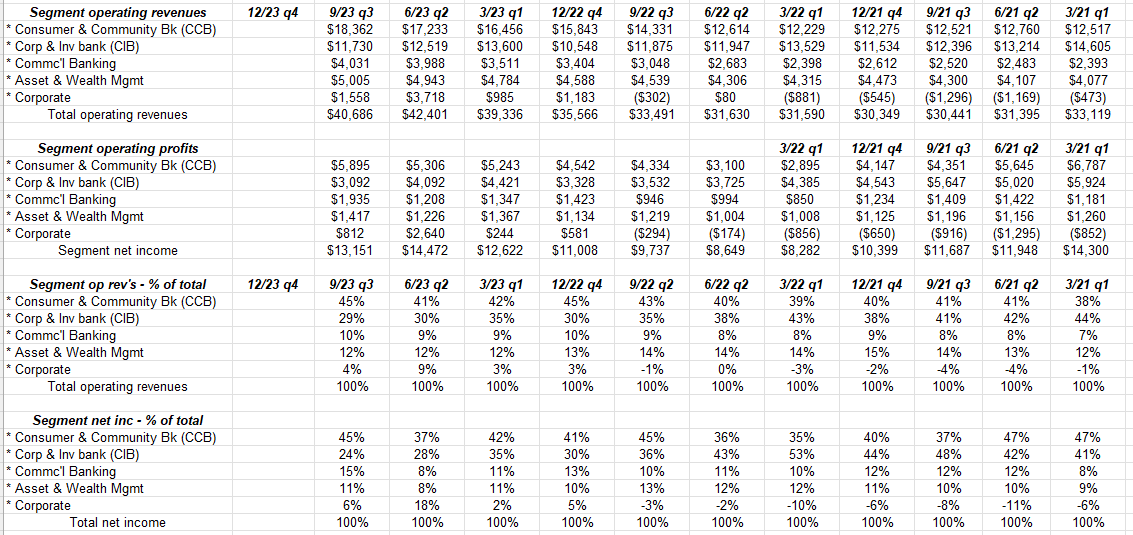

This blog has published this breakdown by segment for JP Morgan in prior previews, and as readers can see the Consumer bank is almost half of JP Morgan’s business, and per the credit card, and consumer default data, as well as the jobs market, while there is a little weakening in the metrics, the fact remains the US consumer is still in pretty good credit shape after the pandemic. ( I thought Jamie Dimon said early in ’22, when many thought a US recession was much closer, that if the US unemployment rate jumped to 6%, the bank would likely have to add $5 – $6 billion of credit loss reserves. The last 8 quarters and the fact that the unemployment rate has remained so contained, has allowed JP Morgan to add credit reserves at a much more reasonable pace, but the prospect still looms large that the US will likely see some kind of recession.)

The swing factor in terms of earnings “delta” is the Corporate and Investment Bank (29% of net revenue and 24% of operating profits), and while the bond market rally in the 4th quarter of 2023 tightened credit spreads and the IPO calendar started to fill, that segment of the bank probably has more upside to it, although continued favorable capitals markets would help.

The current low consensus for 2024 EPS and revenue growth might seem to be a red flag but a year-ago, coming into 2023, the consensus EPS growth was expecting 8% and it’s going to be closer to 39%, while revenue growth for 2023 was expecting 9% at year-end ’22 and actual revenue growth is 24%.

A lot of that ( I think) is actually First Republic (which was very accretive to the bank) if you track the progression of the numbers, but the fact is 2023 turned out much better in terms of consumer and corporate balance sheets than was expected a year ago.

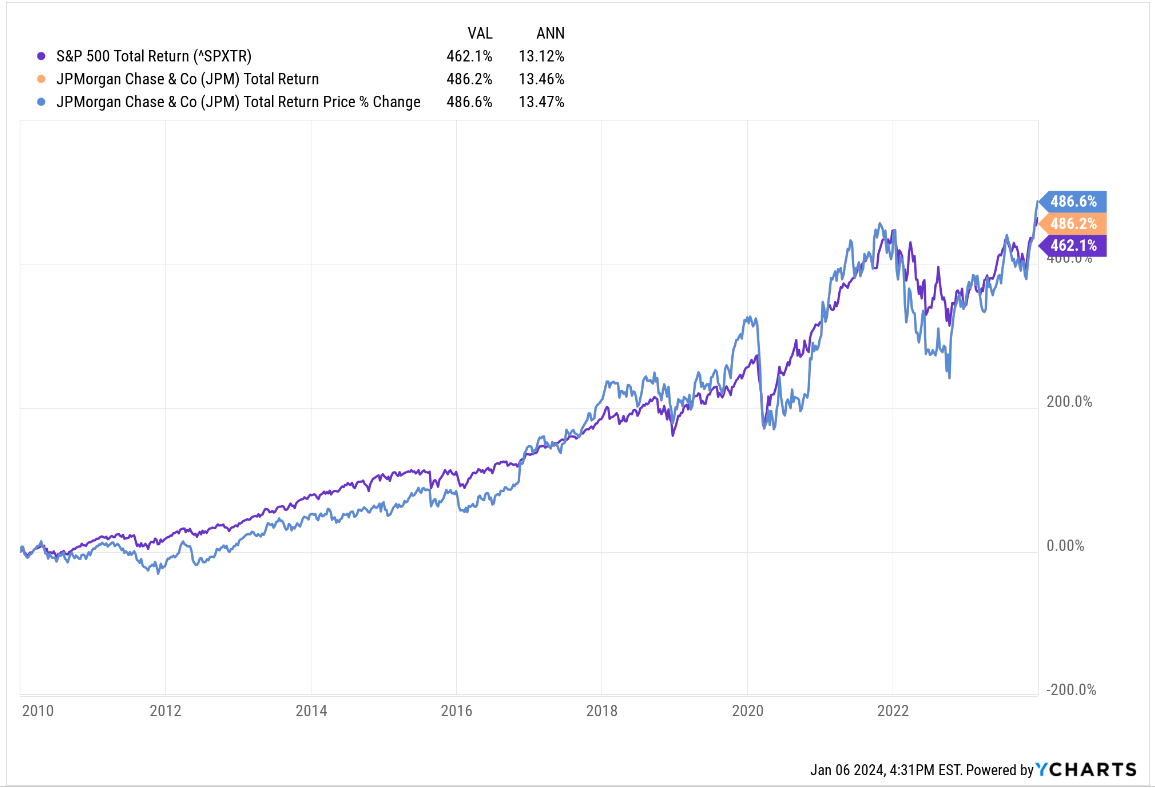

How has JP Morgan stock performed ?

JP Morgan still holds a slight edge to the SP 500 total return since January 1, 2010 or post GFC, through 12/31/23, so we’ll take it.

When JPM reported their Q3 ’23 EPS, the stock was trading around $145. It’s run up nicely into this week’s earnings report, i.e. almost $30 per share, so a reader could reasonably expect some profit-taking after Friday’s earnings, but this blog has no plans to do any short-term trading around the earnings release.

Valuation:

Trading at 10x – 11x expected future EPS growth of – well – not much in expected EPS growth, and 1.75x book value (book value as of the Oct ’23 quarter was $100 per share, and tangible book was $82 per share), it’s kind of puzzling why analysts haven’t lifted numbers yet for 2024 and 2025. And maybe that’s a red flag. With ’23 expected EPS and revenue growth of 39% and 24% respectively, maybe analysts are waiting for guidance and to actually see how conditions unfold in Q1 ’24.

Here’s analyst projected EPS and revenue growth for 2024 – 2026 (as of January 6 ’24) :

- 2026: est EPS growth: -1%, revenue growth est -3%;

- 2025: est EPS growth: 0%, revenue growth est 1%;

- 2024: est EPS growth: -5%, revenue growth est -1%;

With the stock within a dollar of an all-time-high, it’s easy to be bullish, expect for looking at these numbers.

Summary / conclusion: This blog will be out with some more bank / financial sector previews before the end of the week, but JP Morgan continues to be one of the “best of the best” (to steal a line from Men in Black), hence writing the earnings preview forces me to review all the numbers and gather my thoughts and helps formulate the thesis around the stock.

While all the internal metrics like credit and net interest income look solid, the First Republic acquisition seems under-appreciated by investors. That deal had to be hugely accretive for JP Morgan as EPS estimates jumped from $13 to $16 per share from the end of March ’23 to the end of December ’23. It wasn’t all First Republic, but certainly that looks like a good chunk of the expected ’23 upside even as the Commercial and Investment Bank stayed below ’21 levels, which is not a surprise.

For ’24, to duplicate ’23’s growth, I think the Fed / FOMC has to cut rates for the JP Morgan to see EPS and revenue growth at anything approaching 2023’s levels.

The other fly-in-the-ointment is Basel III. To listen to Jamie Dimon rant about the expected capital increases being put forth by the regulators, is a thing of beauty, as someone who leans to the right politically. JP Morgan could probably repurchase more stock and boost the dividend further, but they are being constrained by current capital requirements, and what’s being proferred publicly by the regulators in terms of Basel III, probably makes today’s capital reg’s look paltry. The major bank CEO’s like Jamie Dimon are out in full force in Congress to make sure the proposed plans get watered down (hopefully materially).

It’s almost like the regulators want to repeal the credit / business cycle at the national bank level, and thus put the financial results on auto-pilot, or make financials a completely-regulated industry.

JPM’s weight in the SP 500 is currently 1.25%, and it’s currently ranked 11th in market cap rankings. Clients weight is a multiple of the SP 500 weight, given the bank’s long-term performance, and it’s ROE consistently in the mid-teens or better. JPM has been a top 10 holding for years, within client accounts.

The way to play the stock for readers is – rather than chase it here – wait and make sure the stock trades to an all-time-high above $173, with the all-time-high being from late October ’21, at $172.96. The SP 500 is also testing it’s early January ’22 high of 4,818, so it would hard to reason that if the SP 500 does break out to an all-time-high above 4,818, that the banks wouldn’t participate – particularly a bank like JP Morgan – and move to all-time-highs with the market.

Readers don’t want to get caught chasing JPM higher, only to have the SP 500 and the financial sector correct if the SP 500 corrects and takes time to trade back over the early January ’22 high near 4,818.

None of this is advice or a recommendation, but rather an informed gameplan about how I plan to approach JP Morgan’s coming earnings report. What happens in the overall stock and bond markets does matter in terms of individual stock volatility. Past performance is no guarantee or suggestion of future results. Investing can involve the loss of principal. EPS and revenue data is sourced from IBS data by Refinitiv. This earnings preview may or may not be updated, and if updated, may not be done in a timely fashion. Capital markets can change quickly, both positively and negatively. Readers should gauge your own comfort level with portfolio volatility and adjust accordingly.

Thanks for reading.