Source: internal spreadsheet

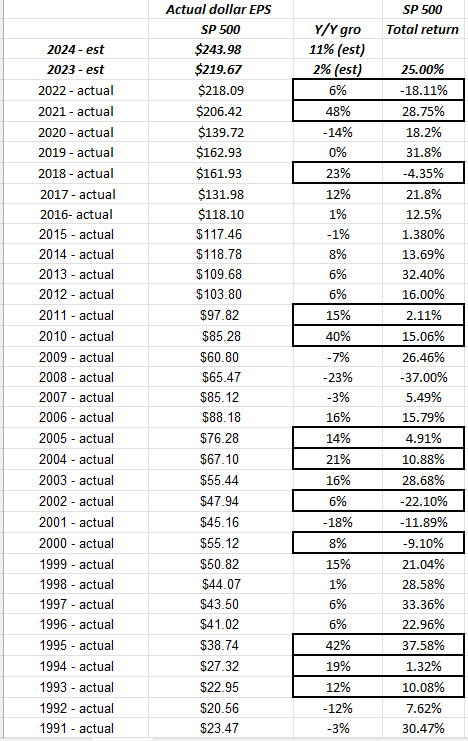

The above is a spreadsheet listing dating back to the early 1990’s, showing annual SP 500 earnings growth vs the actual return on the benchmark for that calendar year.

As you can see, there are substantial variances in “return vs earnings growth” narrative.

The boxes in black border represent the years where the stock market saw “PE compression” or years where the return on the SP 500 was lower than the SP 500 earnings growth for that year.

This article from April ’23, takes a longer look at the data and prior to Q1 ’23 earnings talked about the market return in early ’23 vs earnings expectations.

Calendar 2023 is a perfect example of the SP 500 returning 24% – 25%, with one week left in the year, while SP 500 earnings are up just 2% before we’ve seen Q4 ’23 earnings. More importantly, technology sector earnings are up just 7% so far in calendar ’23, and yet the tech sector (rather the Nasdaq) is up roughly 45% YTD.

This post is in response to a tweet between Neil Sethi (@neilksethi) and Gina Martin Adams (@GinamartinAdams) this week.

Here’s the actual tweet and responses:

Summary / conclusion: There is no question 2023 is a year of “PE expansion”. Looking at the data in the above spreadsheet, readers can see how years of PE expansion are clustered together:

- 1996 – 1999

- 2012 – 2017 (a surprisingly long period of PE expansion)

The fact that 2023 is such a robust year of PE expansion and the fact that years of multiple expansion tend to show some clustering, might leave one a little more bullish about 2024’s SP 500 return prospects.

If the Fed does cut the fed funds rate in 2024, it’s likely the +11% expected SP 500 EPS growth won’t hold up, and we could see a 2nd year of the benchmark multiple expanding, while SP 500 EPS growth slows.

It’s an interesting narrative, and this blog has written on it numerous times over the years.

My guess is we’ll have a good idea of what’s expected in 2024, by the end of January ’24, as the companies reporting their Q4 ’23 earnings starting January 10 ’24 will offer full-year earnings guidance for the coming twelve months.

The fact that Fed-Ex (FDX) and Nike (NKE), two world-class global brands, reported difficult November ’23 quarters and offered tepid guidance this week, isn’t encouraging for Q4 ’23 earnings.

More to come over the weekend.

Take all of this with substantial skepticism. None of this is advice, or a recommendation, and past performance is no guarantee of future results. All SP 500 EPS and revenue data is sourced from IBES data by Refinitiv. Investing can involve loss of principal. Capital markets can change quickly, both positively and negatively. Readers should evaluate your own comfort level with market volatility and adjust your portfolio accordingly.

Thanks for reading.