The US Treasury refunding announcement at 2 pm central today has suddenly become a big deal. Like the early 1980’s when M2 and the money supply was a very big deal and garnered headlines every week – the Wall Street Journal in the early ’80’s ran a front-page article about a union hall meeting in the Midwest where a Fed Governor was speaking and how the first question in Q&A was about the money supply release – with the Treasury refunding announcement now reaching “money supply” proportions.

JP Morgan’s fixed-income team came through the western suburbs of Chicago a few weeks ago – part of Andy Norelli’s JP Morgan Income Fund – and Brandon Merrill, one of Andy’s co-managers detailed why the Treasury refunding’s and T-Bill auctions had gained such prominence this summer.

The budget deficit is much larger than expected in 2023 thanks a number of one-time factors per JP Morgan, including lower capital taxes in 2023, thanks to 2022 capital market losses, the social security COLA bump in 2023, which was the largest in – well – a long time, California tax payment deferrals thanks to the natural disasters in 2022, and several other items I couldn’t write down fast enough.

Another interesting point Brandon Merrill made was that the coupon auctions, i.e. 2,5,7, 10-year, etc. are set in advance and thus any “adjustment” needed to auction amounts are made up in the T-bill or short end of the curve, and since the deficit was so much larger than expected, the T-bill issuance has bee quite sizable relative to history, which is additional pressure on the short-end of the Treasury curve.

Merrill did say that this pressure was expected to abate by the end of October ’23. Let’s see what the results hold today.

October Jobs Report:

We get a look at the October jobs report on Friday, November 3rd at 7:30 am, but we also see JOLTS on Tuesday morning, 10/31, ADP or private sector payrolls on Wednesday morning, 11/1, and then jobless claims on Thursday morning of this week, 11/2, so there are plenty of labor-related reports this week.

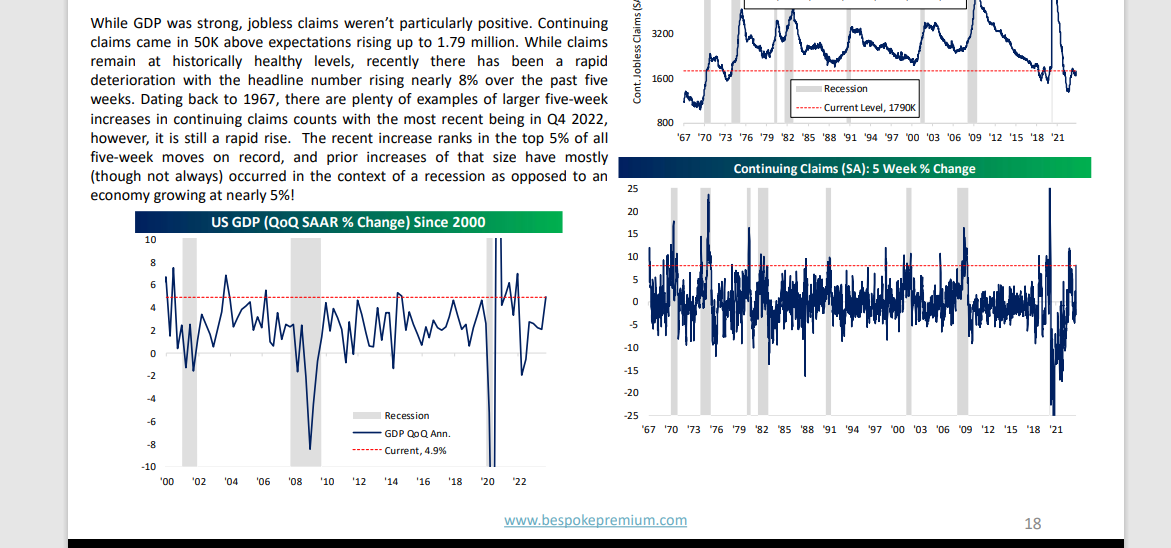

To the say the economic data continues strong is a vast understatement:

1.) The September jobs report was +336,000 net new jobs added as well revisions of +155,000 to prior months which is a whopping “almost 500,000” net new jobs added for September ’23. The interesting thing is that Average hourly earnings in September jobs was just +0.2%, lower than expected given the outsized gain. Jobs up and wage inflation down should have been a plus for stocks – instead October was a punk month for stock returns at least of 10/27/23.

2.) September retail sales, a large contributor to the 2/3rd’s of GDP that is considered “consumption” was also strong, +0.7%, vs the +0.3% expected.

3.) Third quarter GDP at +4.7%, and even if the change in inventories is excluded, the +3.3% is still very robust.

4.) Last week’s new single-family home sales of +12% in September is remarkable given the 8% mortgage rate. Homebuilder stocks like LEN and TOL are reflective of the under-supply, but it seems like “cash-buyers” are helping to fuel the new SF home strength.

But check this chart though:

Bespoke noted this weekend the sharp increase in “continuing claims” rising 8% in the past 5 weeks. Bespoke noted that – in the past – when you see a continuing claims increase like this – is occurred during a recession. Is it UAW and strike-related ?

Summary / conclusion: The Street is still populated with forecasts for 6% – 7% 10-year yield, which would leave much of this irrelevant. However, the catalyst for a move to a 6% – 7% 10-year yield might have implications for other asset classes within bonds, like high-yield, or investment-grade bonds, and even equity market allocations.

There is no question softer economic data would help Treasuries, but there is no indication other than this one Bespoke chart from this weekend’s reading that jobs, or consumer spending is slowing much.

What maybe more interesting though is that with that strong September jobs report, the strong September retail sales, the rock-solid Q3 ’23 GDP release and single-family home sales, the 10-year Treasury has NOT traded over 5.00% definitively. In fact – in the face of all this strong economic data – the 10-year Treasury yield has remained within 4.80% – 5%.

Just sayin…

Watch that refunding announcement later today.

Take everything here as one opinion. Writing it out helps me think through the ultimate portfolio changes, if and when they happen. Past performance is no guarantee of future results.

Thanks for reading.