The other two mega-cap tech names that report this week – META (META) and Amazon (AMZN) do so on Wednesday night, October 25th, after the closing bell, and on Thursday night, October 26th, after the closing bell, respectively.

Part I, posted Sunday night took a look at both Microsoft and Alphabet both scheduled to report after the bell on Tuesday, October 24th, 2023.

META (META):

Meta will lap a very easy quarter in Q3 ’23, where Q3′ 22 saw an 11% EPS miss on a 1% revenue beat. It was the poor results of Q3 ’22 that forced META to address operating expenses, which drove the operating margin down to 20% in Q3 ’22 from a peak of 48% in December ’20. From that quarter forward, META has improved the key margin. Since that earnings release, Meta stock has risen from $99 back to $300.

![]()

Expand the above table and take a look at META’s margin history since late 2020.

It’s not a big position for clients anymore, so not a lot of time will be spent talking numbers. A large chunk of the old Facebook was sold when the Cambridge Analytica story broke and Zuckerberg was found to be completely duplicitous and deceptive about what Facebook was doing with customer data.

If you’ve ever wondered why Warren Buffett doesn’t invest in technology stocks, you only have to look at META to understand why. The original Facebook (FB) was reputationally destroyed with the 2016 Presidential election, and so Mark Zuckerberg pivoted to the Metaverse (META), which I still don’t fully understand since I’ve never actually seen anyone wearing one of those black headsets, and now AI is a potential opportunity for META, if the current business model can get traction. Those are two / three major business model evolutions in the last 23 years, and only 11 of those years have been as a public company.

Valuation: after falling 29% in 2022 EPS is expected to rise 37% in 2023, and the expected, average 3-year EPS growth rate for META is 26%, with a 19x multiple currently. (The PE multiple is the average of the 2023 – 2025 PE.) Meta is expected to average 13% revenue growth over the next 3 years.

If you’re wondering where the expense savings came from for Meta, here is a look at their headcount the last 5 quarters:

- June ’23: 71,469

- March ’23: 77,114

- December ’22: 86,482

- Sept ’22: 87,314

- June ’22: 83,553

The forward revenue estimates are still expected to grow at a “mid-teens” rate, which is important.

Conclusion: Like Alphabet, Meta is dependent on ad spending and the last half of ’22 is making for easy comp’s for the Meta and Alphabet, where ad spending really softened. Since it’s no longer a major holding but some clients still hold shares – some with a cost basis around $20 per share – thus, it’s worth the follow. These are taxable accounts that are very capital gains sensitive that continue to hold the stock.

The stock is up 156% YTD, but is still down 19% – 20% from it’s $383 high in September ’21.

In a nutshell, headcount reduction and operating expense savings has helped operating margins gains since Q3 ’22. The important element to META is that revenue growth must continue and – given the forward estimates – 2023, 2024, and 2025 “expected” revenue (per Street consensus) looks good.

Amazon: (AMZN):

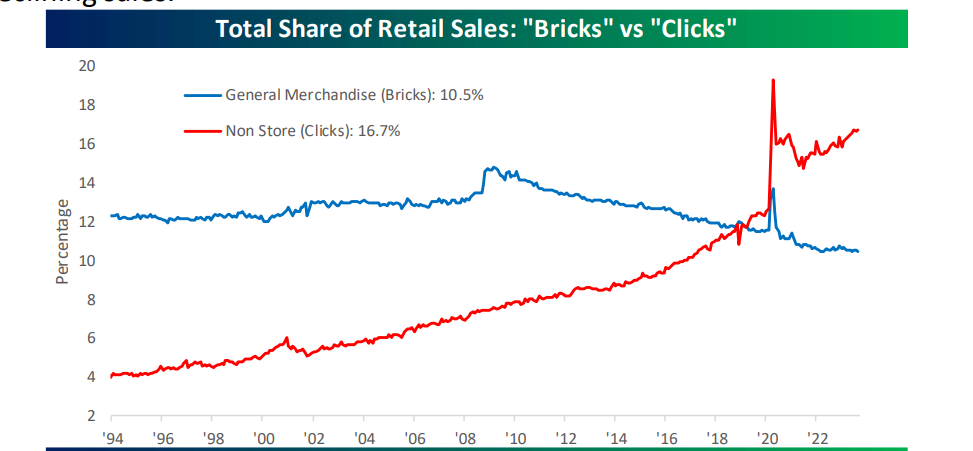

If there’s one graph that highlights the struggles Amazon has had since the onset of Covid and the pandemic, it’s the red line above (non-store portion of retail sales), compliments of the Bespoke Report, from October 20 ’23. Last week’s September retail sales report was still quite healthy and ecommerce continues to grow, but is still short of it’s 2021 peak.

Doing the math, “online store” revenue for AMZN is down to 39% of total revenue for the ecommerce giant versus over 50% during 2020 and 2021 or the throes of the “stay-at-home” and “work-from-home”. Online store revenue over the last 7 quarters has averaged “0%” and been negative 4 of those last 7 quarters ended June ’23. (Amazon does not disclose segment operating income to my knowledge.)

AWS (Amazon Web Services), which is 16% – 17% of Amazon’s total revenue has seen yoy revenue growth slow markedly the last 7 quarters:

- 6/30/23: +12%

- 3/31/23: +16%

- 12/31/22: +20%

- 9/30/22: +27%

- 6/30/22: +33%

- 3/31/22: +37%

- 12/31/21: +40%

While sell-side analyst’s have been reluctant to assign a reason for the AWS slowdown, it’s clear that post-Covid, perhaps adoption during Covid slowed as corporations exited the pandemic.

At one point AWS was accounting for all of AMZN’s operating margin but as AWS online resumes growth, and AWS has slowed, the AWS operating margin was just 36% of AMZN’s total operating margin in the June quarter.

Valuation: trading at a PE of 40x for an expected EPS growth over the next three years of 51% on an average expected revenue growth rate of 12%, AMZN – like the other big tech stocks in 2023, is cheaper on a growth-at-a-reasonable-price basis than an absolute basis, but that’s not untypical of growth stocks.

Morningstar star has a $150 fair value estimate on AMZN versus its current price of $130 – $135, so the ecommerce giant is still thought to be slightly undervalued versus that estimate. The big issue for AMZN is that they expanded too quickly during 2020 and 2021 or in the midst of the pandemic to keep up with demand, and now have had to “right-size” the business to be able to leverage revenue growth. Personally I think AMZN is finally getting there and comp’s look easier in 2024, particularly for AWS and the online business.

AMZN Conclusion: The goal here is not to re-write “War & Peace” for AMZN pre-earnings, but readers can see that 56% of AMZN’s revenue that was growing at a decent clip, has now slowed. Physical stores or rather the Whole Foods acquisition that is now Amazon Fresh, isn’t meaningful yet, at 4% of total revenue.

Long-term investors are watching the graph above and waiting for ecommerce sales to resume their upward trend (and it will) and eclipse the pandemic highs from 2000 and 2001.

AMZN has lost a lot of the “frenzied” investor base, as Jeff Bezos’ departure top-ticked the stock for long-term investors, but I also don’t think there is any long-term damage to the core business models, only that AMZN had to adjust to “too-fast growth” in 2020 and 2021. If there is one metric ot watch in future quarters, watch the yoy revenue growth for the online business; anything better than 10% will drive operating margin leverage. AWS does face easier revenue and margin comp’s in 2024.

Tech earnings conclusion: Given the performance of the tech sector the last few months, sentiment and bullishness has really been tempered around the mega-cap names as they enter into Q3 ’23 earnings tonight. On a GARP basis the 4 stocks previewed look cheaper than they did three months ago. I still remain positive about tonight’s earnings reports and tech in general headed into Q3 ’23 earnings releases. Alphabet faces the easiest comp’s versus Q3 ’22, I still like Microsoft and Amazon for longer-term positions for clients (both stocks remain top 10 positions in client accounts) and have been for the last 12 – 13 years, while the smallest weight is META, only because of Cambridge Analytica, and whatever Metaverse seems to be or could be in the tech sector.

Take all of this with substantial skepticism and a considerable grain of salt. Past performance is no guarantee of future results. This is only one opinion in a sea of opinions so treat it accordingly. Some of the information above may or not be updated and if updated may not be updated in a timely fashion. gauge your comfort level with your portfolio volatility and adjust it accordingly.

Thanks for reading.