This weekend’s Weekly Earnings update noted the SP 500 earnings yield (EY) is at a 6-month high, and that 4 big tech names are scheduled to report this week: Microsoft, Alphabet, Meta and Amazon.

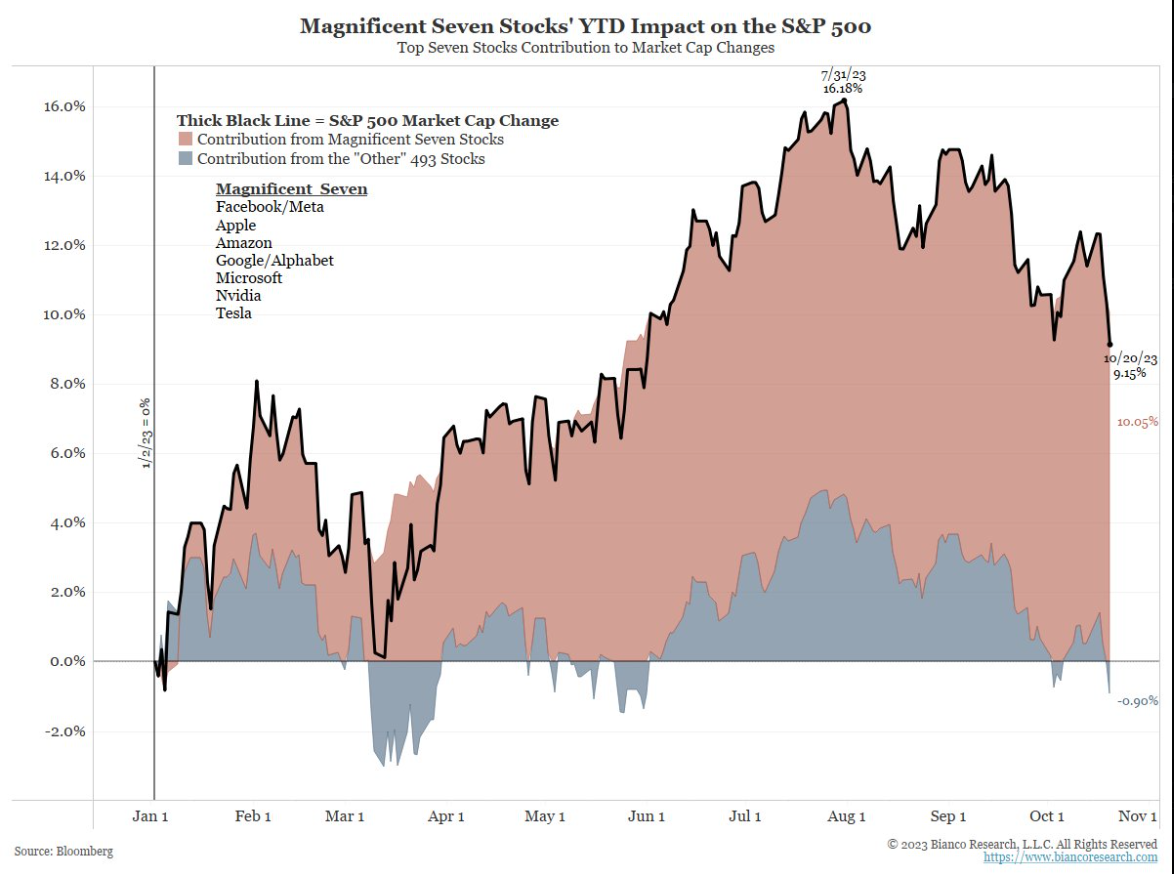

Jim Bianco posted some interesting graphs to X over the weekend, and here’s one:

This graph shows how tenuous the SP 500 leadership is currently, and without the mega-caps, the SP 500 is down on the year.

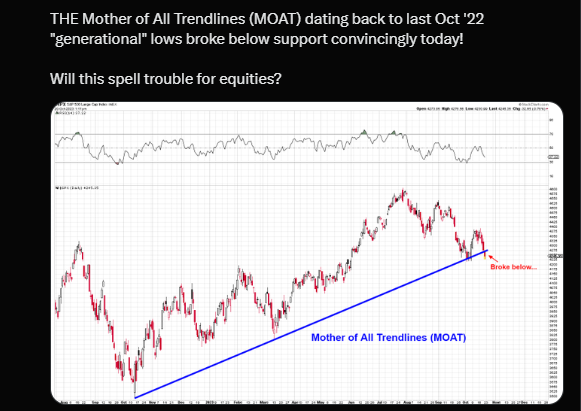

This is a chart posted to yesterday’s blog post noting how the SP 500 is sitting on the trendline from the October, ’22 lows.

How the big 4 tech names of the Magnificent 7 trade after their September quarterly results will go a long way to determining whether the uptrend continues or the trendline fails.

Let’s look at the fundamentals:

Microsoft: (MSFT):

When Microsoft reports their fiscal Q1 ’24 results after the close Tuesday night, October 24th, Street consensus is expecting $2.65 in EPS on $54.5 billion in revenue for expected year-over-year (y.y) growth of 13% and 9%, respectively. Operating income growth is expected to grow 13% y.y. MSFT guided to 25% – 26% (cc or constant currency) Azure growth in fiscal Q1 ’24.

Street guidance by segment for Q1’24:

- Total revenue: $54.3 bl (midpoint)

- Prod / Business: $18.1 bl (midpoint)

- Intell Cloud: $23.5 bl (midpoint)

- PC biz: $12.7 bl (midpoint)

In fiscal Q4 ’23, MSFT generated 10% rev growth (cc), operating income growth of 18%, and EPS growth of 21%. Azure actually came in a tad better-than-expected, up 27% for the quarter, vs the +26% expectations.

For fiscal Q2 ’24 (December ’23 qtr), the Street is expecting $2.66 in EPS, $24.2 billion in operating income and $58.4 billion in revenue for expected y.y growth of +21%, +19% and 11% respectively.

From a bigger picture perspective, the move in AI (artificial intelligence) will begin in earnest with the launch of Copilot on November 1 ’23, Commercial users already have Copilot with the update to Windows 11 in late September ’23, so it will be interesting to hear preliminary thoughts from MSFT management on the conference call, if they choose to discuss it. Microsoft did warn earlier in calendar ’23 that AI will likely swell capex in fiscal ’24, so the capex guide for the rest of the ’24 fiscal year will be important.

I thought the closing of the Activision deal the last few weeks, would continue to drive Microsoft’s presence into the consumer space, which they are in already with XBox, but the closing of the deal doesn’t seem to have generated any analyst commentary yet. Personally I think it’s a positive for the software giant given their enterprise share, although Morningstar maintains that gaming is a no-moat business.

Valuation: MSFT is a fortress stock, with an “expected” 3-year EPS growth rate of 16% on an expected 3-year average revenue growth rate of 13%, that currently sports a 26x EPS multiple, so on a PE-to-growth basis, the stock is cheaper pre-earnings than it was earlier in the summer. Even with a cash-flow valuation of 27x and 40x cash-flow and free-cash-flow (ex cash) Microsoft has a 3.5% free-cash-yield. The software giant is coming off an easy year of comp’s with revenue growth slowing to mid-single-digit y.y growth, but that is expected to change going forward, as the forward revenue estimates expect mid-teens revenue growth going forward.

Microsoft has $111 billion in cash on the balance, recently hiked their dividend nicely, and tends to repurchase $5 – $6 bl of their stock every quarter. Sometimes that quarterly repo jumps to $7 – $8 billion.

The Intelligent Cloud (IC) segment and Azure are now the straw(s) that stir the drink at Microsoft. Back in 2016, the Intelligent Cloud segment was just hitting 30% of total Microsoft revenue and 43% of operating income, while today that revenue has risen to 43% of total and the same percentage of operating income. Copilot will only add to IC’s results going forward.

Conclusion: Microsoft’s EPS and revenue estimates have remained stable to higher since the July ’23 earnings report, and MSFT was fairly cautious on revenue guidance for Q1 ’24. With the launch of Copilot coming up, investors will hear with the December ’23 quarter’s results how Copilot is impacting numbers. Since the Spring ’23, there’s a lot of hype around AI, but no one is yet quantifying the impact. There are no indications that the quarter will come in at anything other than “expected” given trends in EPS and revenue and the trading of the stock. MSFT will likely be a leader in AI as they were with cloud.

The stock has been a top 10 holding for clients since shortly after ValueAct took a 2% stake in the stock in the spring of 2013 and it hasn’t disappointed.

MSFT peaked in early November ’21 at $249 per share, so the stock is down from it’s peak two years ago by 8%, but is up 37% YTD in terms of it’s trailing return.

Alphabet: (GOOG/GOOGL):

Alphabet also reports their September ’23 quarter after the closing bell on Tuesday, October 24th, 2023. Street consensus is expecting $1.45 in EPS, $21.4 billion in operating income and $75.4 billion in revenue, for y.y growth of 2%, 25% and 10% respectively. Looking at the valuation spreadsheet, the aspect of GOOGL’s financials that jumps out is that GOOGL faces very easy comp’s or compares in the first half of calendar ’24.

In Q3 ’22, (i.e. last year), GOOGL printed 1% EPS growth, a decline in operating income of 19%, on 29% revenue growth. Last year’s Q3 ’22 was in the midst of the ad spending slowdown when all major ad businesses missed consensus by 4% – 5%. GOOGL’s Q3 ’22 operating margin fell by over 900 bp’s y/y in Q3 ’22.

It looks like Q3 ’23 will also be an easy compare for GOOGL Tuesday night as well.

Last quarter, Q2 ’23, revenue grew 9% cc, operating income grew 12% and EPS 19% as ad revenue as cloud revenue grew 28% y.y.

Cloud revenue has been growing 28% – 29% for the last 2 – 3 quarters and in the mid 30% range back in mid-’22.

Valuation: again, using the 2023 – 2025 EPS and revenue estimates, the average, expected EPS growth for the next 3 years for GOOGL is 16%, while revenue growth is expected to average 10% over the next 3 years, and with the stock trading at 20x multiple (average for next 3 years) GOOGL looks more attractive on GARP or growth-at-a-reasonable-price basis than on an absolute basis. GOOGL is cheaper than MSFT on a cash-flow and free-cash-flow (ex cash) basis, trading at 16x and 24x those valuation metrics.

GOOGL has repo’ed a whopping $60 bl in shares on a trailing-twelve-month basis, which represents about 4% – 5% of GOOGL’s market cap. I think Ruth Porat instituted the repo in 2017 and it’s done nothing but grow every quarter.

Conclusion / summary: with ad revenue being 80% of total Alphabet revenue and Alphabet Cloud being 11% of revenue, it has a long way to continue to expand, particularly at it’s 25% – 35% y.y growth rate, but cloud’s operating income is what really needs to grow as it represents just 2% of operating income currently.

EPS and revenue estimates have been revised higher since the July ’23 earnings release, but remain somewhat flat to slightly lower versus the October ’22 estimates.

My own opinion is GOOGL will have a good quarter, particularly against easy ad spending weakness one year ago, but the bigger risk is the potential judgment around GOOGL search and the pending search lawsuit that’s gotten a lot of attention the last few weeks. This potential judgment will hang over the stock and judges can be notoriously fickle and not stick to precedent, which can result in sharp swings in stock price.

GOOGL (the stock) also peaked in mid-November ’21 near $150, and is trading down about 10% from it’s all-time-high, but the YTD trailing return for the search giant is +54% YTD.

Part I conclusion:

The helpful aspect to the tougher market action since July 31 ’23 on the back of higher interest rates, is that for growth stocks that do continue to grow, the PE compression can only last so long and the stocks pop like a beach ball being held under water.

There is no discernable reason apparent today, that either Microsoft or GOOGL will miss their respective quarter’s when financial results are released Tuesday night, and in fact given GOOGL’s easier comp’s against last years Q3 ’22, the results will likely look pretty strong, so being long both stocks for clients, the positions will likely remain unchanged until after results are posted Tuesday night, October 24th.

Both Microsoft and Alphabet will be beneficiaries of AI, but MSFT has the more discernable path forward with Copilot today, while GOOGL’s quarter will likely be influenced again by cloud revenue growth and the strength in ad spending.

Stay tuned for Tuesday night. How tech reports this week, will no doubt be instrumental in whether the SP 500 can hold the uptrend.

(Take all this with a healthy dose of skepticism. This is one person’s opinion, and past performance is no guarantee of future results. All individual stock EPS and revenue estimates are sourced from IBES data by Refinitiv, although valuation data and metrics are sourced from internal spreadsheets. Capital markets can change quickly for both the good and the bad. This information may or may not be updated and if updated may or may not be updated in a timely fashion. Readers and investors should gauge their appetite for volatility accordingly, and make adjustments where necessary.)

Thanks for reading.