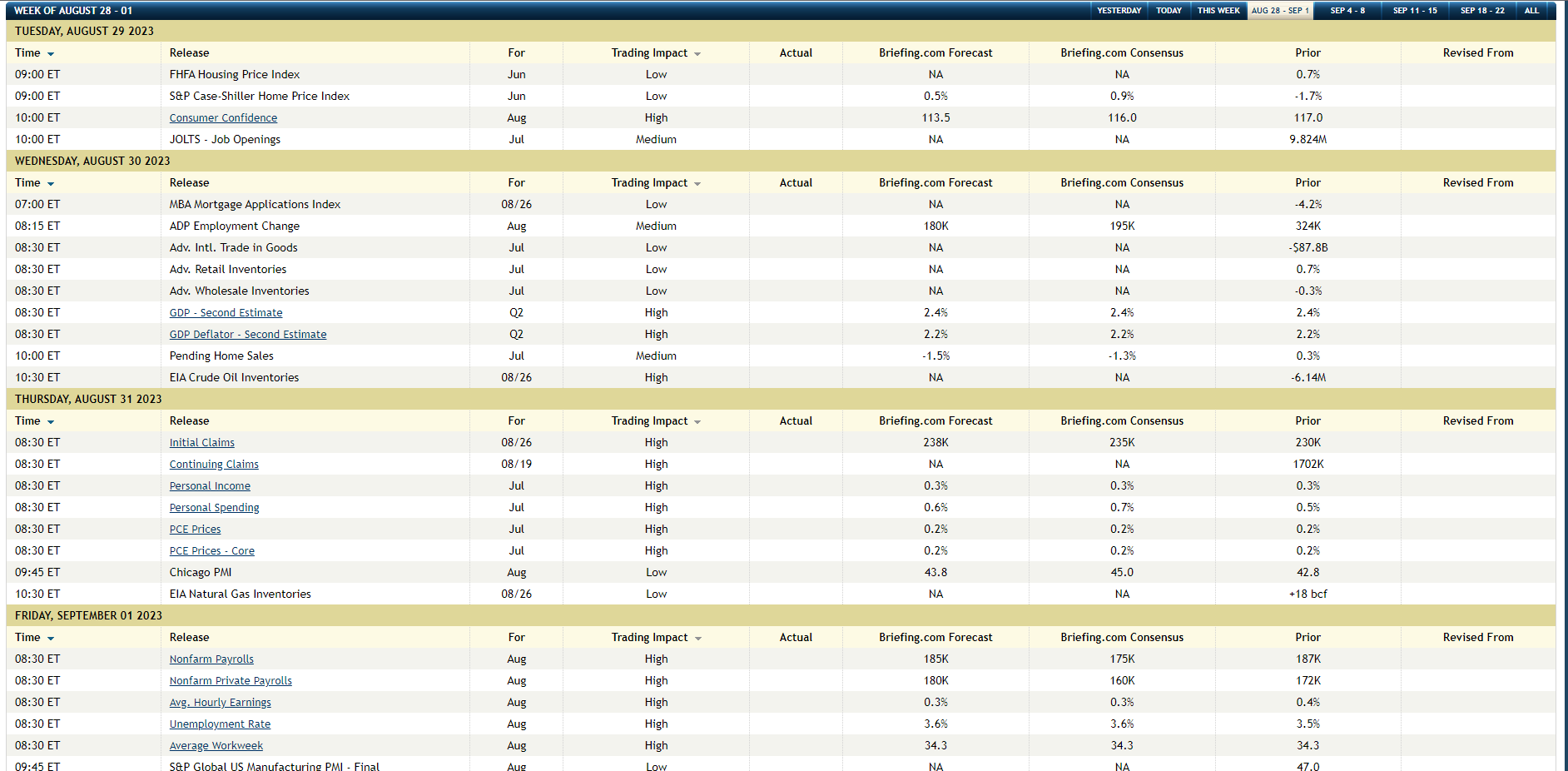

This economic data template published by Briefing.com is a useful tool for preparing for the coming economic data each week.

Here’s all the expected economic data for the week of 8/28/23 through 9/1/23.

On Friday, September 1, ’23, the August nonfarm payroll report will be released and consensus expectations are looking for 160,000 – 180,000 net new jobs created in the month of August ’23. Average hourly earnings ran a little hotter in the July ’23 report at +0.4%, despite the net new job growth being in-line with consensus.

The estimate for average hourly earnings for the August ’23 report is +0.3%.

SP 500 data:

- The forward 4-quarter estimate for the SP 500 jumped to $232.80 this week from last week’s $231.72. It’s clear the last few weeks and really since mid-July ’23 that SP 500 forward earnings estimates are seeing positive (i.e. upward) revisions;

- The PE ratio on the forward estimate is 18.9x this week versus the same 18.9x last week;

- The SP 500 earnings yield ended the week at 5.28%, versus the 5.30% last week and has now risen off the late July ’23 and early June ’23 levels of 5.03%, thanks to both the rising forward estimate and the market correction;

- Since June 30 ’23, the Q2 ’23 bottom-up EPS estimate has risen from $52.91 to $54.24;

- Per the IBES data by Refinitiv reports, the “upside surprise” for Q2 ’23 SP 500 EPS is 8% as of this past week, still ahead of Q1 ’23’s 6.7%, while the revenue upside surprise is 1.8% versus the 2.2% from Q1 ’23;

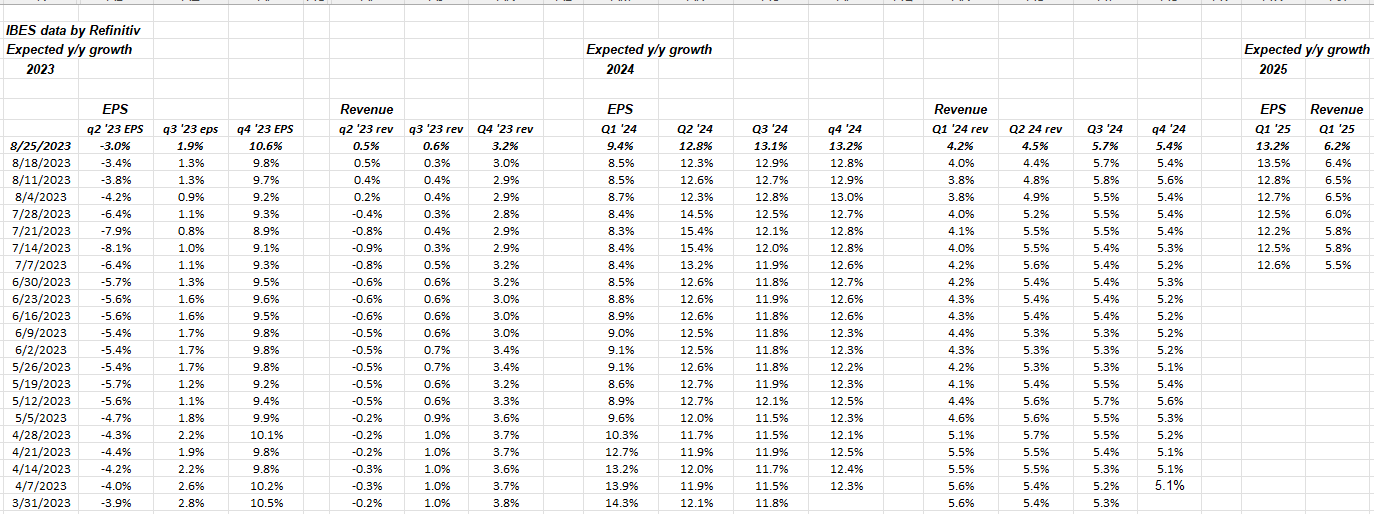

Expected Quarterly SP 500 EPS / Revenue Growth Rates:

Haven’t shown this table in a while, but readers should note the increase in the expected quarterly EPS growth rates for the rest of 2023 and 2024 in the table:

Note the bump in 2024 estimates, too.

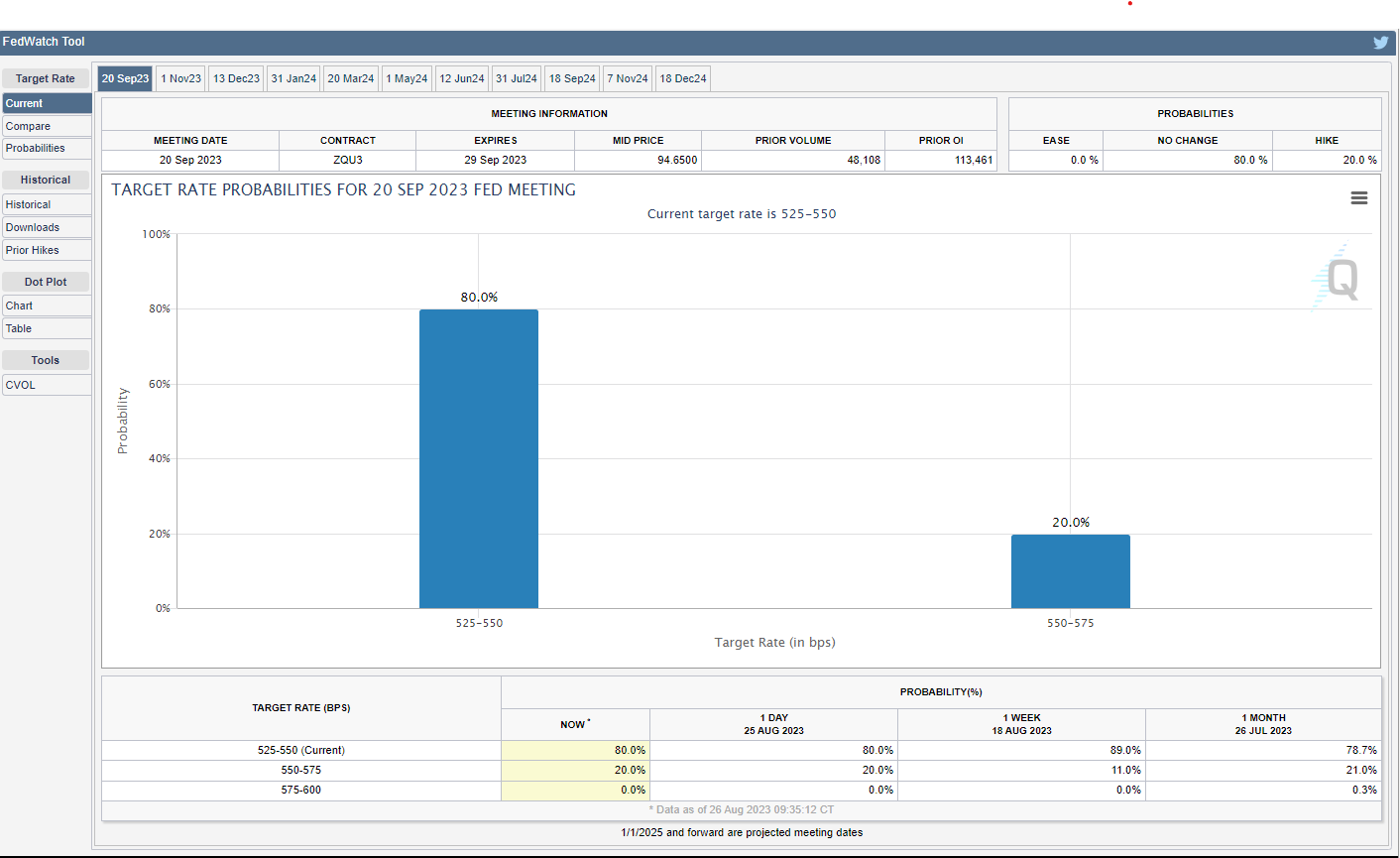

Fed funds futures:

Jerome Powell’s Jackson Hole statement released to the financial markets on Friday morning, August 25th, 2023, seemed to have little impact on the fed funds futures for the next FOMC meeting on September 20, 2023. There is an 80% chance of “no change” to the fed funds rate on 9/20 and a 20% chance of a 25 bp increase, which was where I thought the probability metrics were prior to the release.

Obviously, next Friday’s Sept 1, ’23 August jobs report will impact the fed funds futures market.

Summary / conclusion: Nvidia (NVDA) was still up 6% on the week, even though the bigger surprise in terms of watching the daily trade this week was seeing NVDA sell off and finish lower on Thursday and Friday.

But it’s clear the Treasury market uncertainty and the direction of interest rates, is acting like a wet blanket for “PE expansion” and the stock market moving forward, in a seasonally-weak period anyway, and that’s not a bad thing.

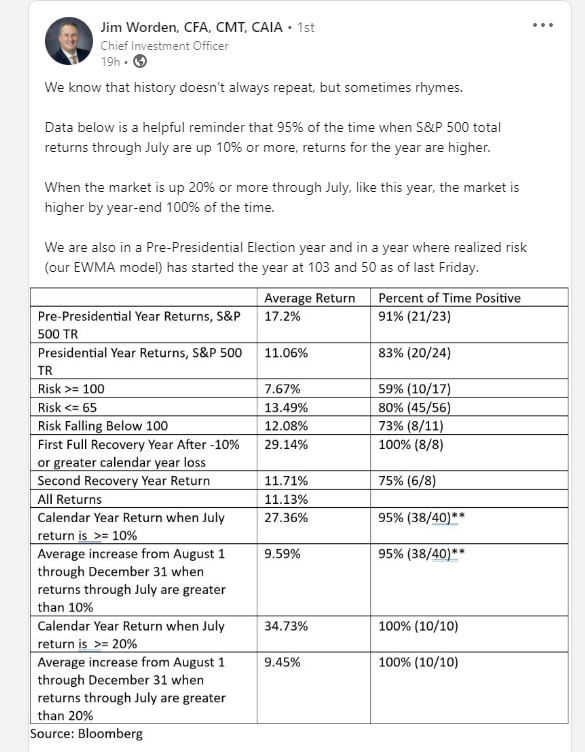

Here’s the last thought for the markets this week: just happened to read a LinkedIn post by Jim Worden at breakfast this Saturday morning, and the statistical patterns highlighted by Jim.

The statement “when the market is up 20% or more through July, like this year, the market is higher by year-end 100% of the time.”

The statement “when the market is up 20% or more through July, like this year, the market is higher by year-end 100% of the time.”

Statistically, that makes it hard to support the bearish case.

Take all of this with a grain of salt and a healthy amount of skepticism. Past performance is no guarantee of future results. All SP 500 EPS and revenue data is sourced from IBES data by Refinitiv, although the spreadsheets and measurements are my own, hence all errors are the author’s fault. None of this should be construed as advice, and all information and opinions provided may or may not be updated and if they are updated may not be done in a timely fashion. Capital markets can change quickly. Evaluate your own comfort level with market volatility and adjust your portfolios accordingly.

Thanks for reading.