Walmart (WMT) reports their fiscal Q2 ’24 financial results on Thursday morning, August 17th, 2023, before the opening bell. Current sell-side consensus expects $1.69 in earnings per share (EPS) on $159.9 billion in revenue, and $6.9 billion in operating income, for expected year-over-year (y.y) growth in revenue of 4.6% in revenue, 1% in operating income and -4.5% decline in EPS.

It was the July ’22 quarter where Walmart saw about 130 bp’s of gross margin pressure and “high-teens grocery inflation” per the notes.

With July ’23 retail sales out this morning, grocery rose +0.8% which was one of the stronger categories, so that bodes well for the retail giant that does about 50% – 60-% of it’s expected fiscal ’24 revenue of $635 billion from the grocery aisles.

The point is, Walmart has an easier comp against last year’s July ’22 quarter. Let’s see if it helps.

Historical operating margin:

Walmart’s early April ’23 announcement of significant automation of the supply chain was an announcement that could have important ramifications for the retail giant. Here was the short summary of the Walmart April 4, 2023, announcement as well as a look at 3 – 5 year guidance as summarized on Briefing.com:

- Co also affirms its commitment to financial framework of 4% sales growth and 4%+ operating income growth over the next 3-5 years.

- As part of WMT’s 2023 Investment Community meeting, the company also highlighting its purpose, unique culture and the importance of its associates and unveiling its plan for a new more connected and automated supply chain which will improve the experience for its customers and associates and simultaneously increase productivity.

- By the end of Fiscal Year 2026, Walmart believes roughly 65% of stores will be serviced by automation, approximately 55% of the fulfillment center volume will move through automated facilities, and unit cost averages could improve by approximately 20%

Walmart’s operating margin has been under assault from Amazon since the early 2000’s but Walmart’s operating margin really started to get hammered in the middle part of last decade, from 2015 – 2019. Here’s the progression of the numbers.

- 2021 to Apr’23: 4.06%

- 2010 to 2019: 5.23%

- 2001 to 2009: 5.74%

- Late 1990’s: 5.84%

To demonstrate to readers the impact of last decade and the ascendancy of Amazon’s e-commerce or online stores, here’s what the decade of 2010 to 2019 looked like for Walmart in terms of operating margin pressure, cut down the middle:

- 2016 – 2019: 4.48%

- 2010 – 2016: 5.73%

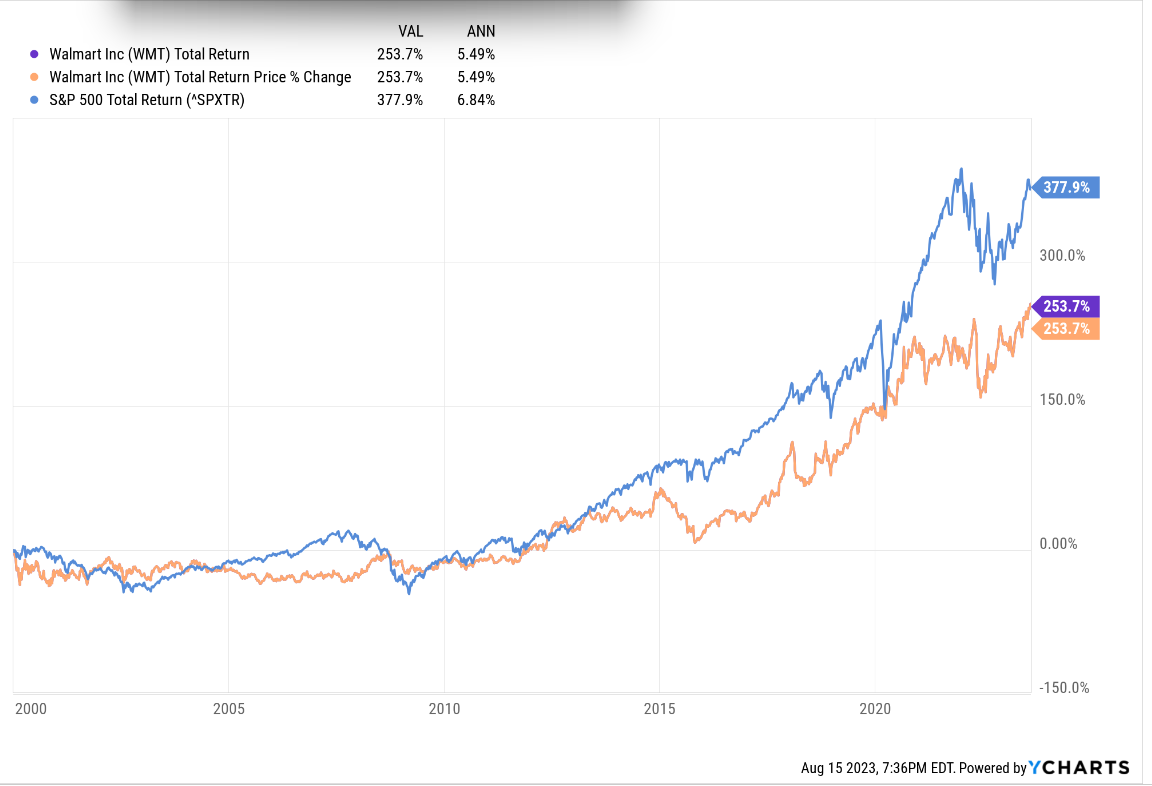

Walmart performance vs the SP 500:

(Click on chart to enlarge or expand)

Since early 2000, when Walmart’s stock peaked in March, 2000, along with the rest of the large-cap SP 500 names, the stock has trailed the SP 500 by about 100 bp’s a year for the last 23 years. There was a larger underperformance gap in the middle of last decade which corresponds with the accelerated erosion of the operating margin, and since 2020, the underperformance of 100 bp’s per year has returned.

While I’m not expecting any great quantification of the automation process to be forthcoming Thursday morning, I do think that this could be a significant event for Walmart, both financially and operationally.

If Walmart just returned the operating margin to 5%, versus the 4% today, and kept revenue constant at $635 billion, Walmart would generate an additional $6.3 billion in operating profit per year.

Valuation:

Most investors think of Walmart as “expensive” since the stock trades at 22x earnings for expected 3-year average EPS and revenue growth of 7% and 4% respectively, but investors who quickly draw that conclusion without looking at cash-flow, don’t realize on a cash-flow-per-share basis, Walmart trades at closer to 11x since cash-flow-per-share is almost $14.

The quality of Walmart’s earnings is quite high: cash-flow and free-cash-flow cover net income quite easily, with free-cash-flow historically covering net income by more than 100% or more than 1x net income.

Because of the inventory issues in calendar ’22, Walmart’s inventory and cash-flow in ’23 looks a little better than so-called normal years since inventory turnover is returning to normal and thus so is cash.

Summary / conclusion: This earnings preview is usually typically written over on www.seekingalpha.com but one of the editors thought I should wait and do an “earnings summary” after the financial results are released, which I will be happy to do.

Walmart was basically flat in 2022, versus the SP 500’s -18.16% return, and is up roughly 14% YTD in ’23, versus the SP 500’s +16% return YTD.

I got more interested in the stock in June ’22, when it tumbled to the $120 area after the inventory glut hurt earnings and more importantly cash-flow. It’s been owned for years by clients as one of the few consumer staple names in client accounts, and the sharp drop in May and June ’22 was a good opportunity to add to the retail giant.

Morningstar puts a $145 fair value on the stock, but I suspect if Doug McMillon can execute on the automation and purchasing / logistics streamlining, and get the operating margin expanding again, even if it takes a few years, which it has to given Walmart’s enormous size, I think the stock has significant upside from its current level at $159.

There is more bullishness than usual coming into the Thursday morning earnings call, which is a little worrisome, although small positions were added to the stock even this week.

This supply-chain and logistics automation could be a significant event in Walmart’s history. Or it could be a lot of noise. I could be wrong on a lot of this and the savings may not materialize, so we’ll see, but I think this is the right longer-term move for Walmart after 2 decades of pressure from Amazon.

Take all this with substantial skepticism and a material grain of salt. Past performance is no guarantee of future results. Investing involves risk and potential loss of principal. All earnings and revenue data is sourced from IBES data by Refinitiv. This information may or may not be updated and if updated may not be done in a timely fashion. All this is one person’s opinion.

Thanks for reading.