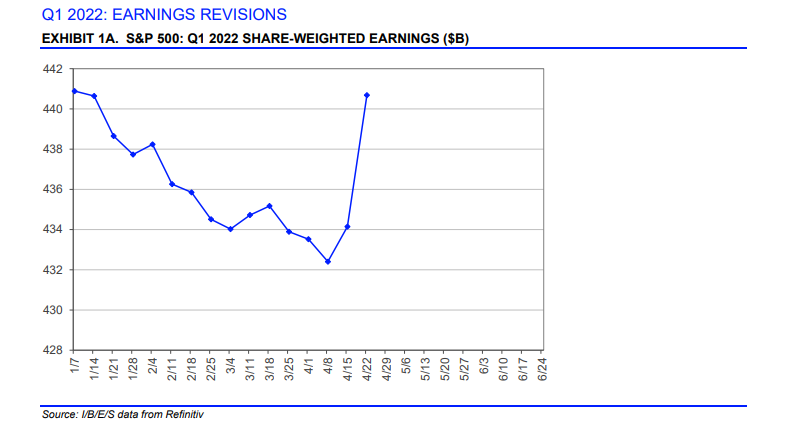

This graph is from the first page of Refinitiv’s “This Week in Earnings” and it gives a different look at “earnings” (actually it’s net income) for the SP 500 and as readers can see the ramp in net income is healthy as it usually is, with the start of SP 500 financial results.

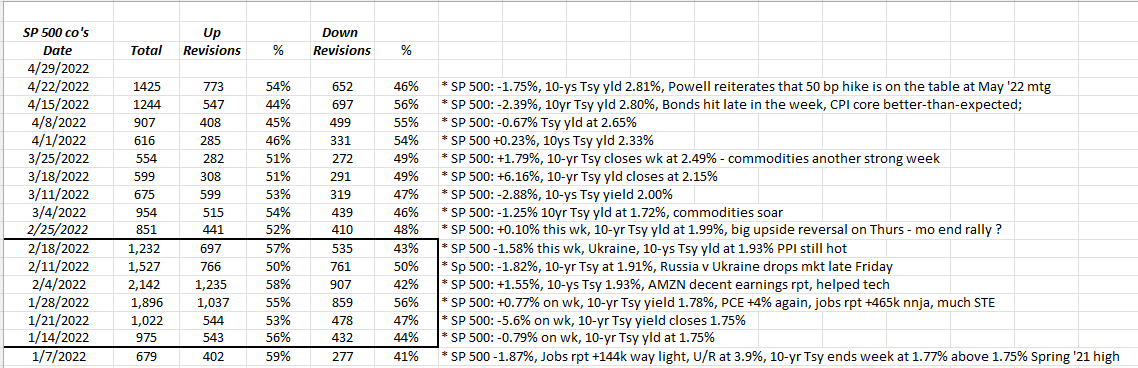

Another data point for readers to look at is SP 500 revisions: here’s the table with this week’s updated revision data:

Note how this week’s financial results saw an increase in “positive” or “Up revisions” for the SP 500. Up revisions jumped to 54% vs 46% down revisions for the SP 500, the first positive “up vs down” week since March 25th.

This table was updated around noon on Friday, April 22nd, so the actual weekly decline for the SP 500 as of 4/22/22 was -2.64%.

As readers can see from the table, it was the first “3 weeks in a row” drop for the SP 500 since September ’20.

SP 500 data:

- The forward 4-quarter estimate rose this week to $234.04 from $233.83 although the forward PE compressed to 18.2x from last week’s 18.8x;

- The SP 500 earnings yield jumped to 5.48% from last week’s 5.32%;

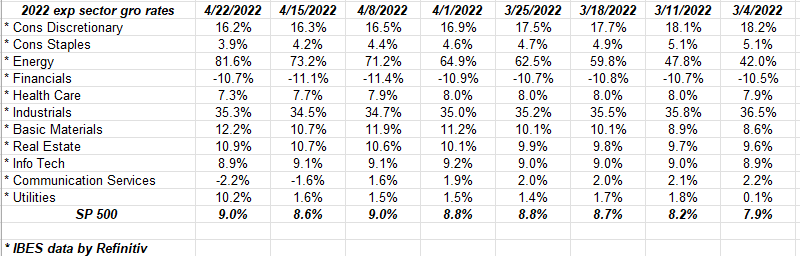

This table above from Refinitiv shows the “expected” full-year 2022 EPS growth rates currently embraced by sell-side analysts.

Only the energy sector has seen a sharp improvement since 4/1/22. Refinitiv also notes in their “This Week in Earnings” that if energy is excluded from the SP 500, that SP 500 EPS is up just 1.6% in Q1 ’22 on a year-over-year basis. Part of this is the tough compares from the first quarter in ’21, particularly for financials and the technology sector.

Speaking of Technology:

Microsoft: ($2 trillion mkt cap, #2 market cap weight in SPY at 5.65%)

Microsoft kicks off tech earnings Tuesday night, April 26th, 2022, with fiscal Q3 ‘s financial results: IBES data by Refinitiv is looking for $2.19 in EPS on $49 billion in revenue while Briefing.com is showing consensus at $2.20 on $49 bl in revenue for expected y.y growth of 8% and 18% respectively. In March of ’21 MSFT printed 19% revenue growth and 45% EPS growth which makes for a tough compare for the software giant. Last quarter Azure grew 46% y.y, and management guided to $18.75 to $19 billion for Intelligent Cloud revenue in Q1 ’22. Azure’s y.y growth rate has been one of the closely-watched metrics by investors and it’s help up surprisingly well for a long time. If cloud and Azure miss (and there is no indication that will happen given the positive revisions to forward EPS and revenue estimates), that’s a sea change for the stock and the business.

Microsoft’s operating margin expanded 383 bp’s and 612 bp’s in the March and June quarters of 2021, so again, the MSFT has tough compares with that metric.

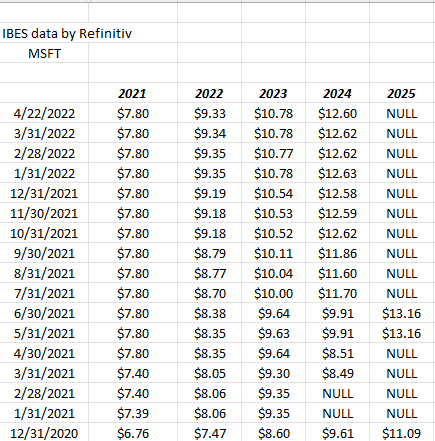

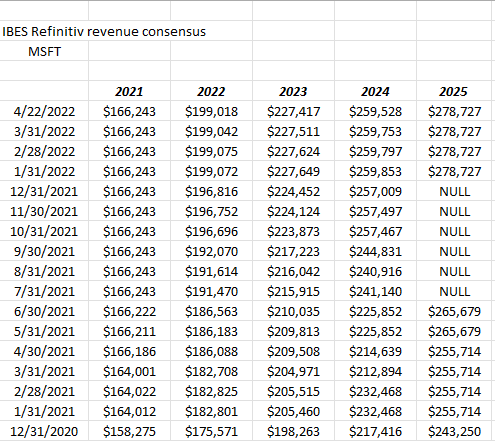

Readers can see the trend in MSFT’s EPS and revenue revisions is steadily higher with the 2022 and forward consensus being the important years. (MSFT’s fiscal year end is June 30.) The Street is currently expecting 16% EPS and revenue growth over the next 30 months (2.5 years) with the stock trading about 30x earnings so it’s pretty fairly valued with a 3% free-cash-flow yield and $127 billion in cash on the balance sheet.

After the growth of the cloud the last decade, MSFT’s 3 different business segment, i.e. Business & Productivity, Personal Computing and the Intelligent Cloud are all roughly 1/3rd of MSFT’s total revenue and operating income each. But the cloud and Azure have been the stars the last 10 years. If Azure’s growth holds up – near the 45% – 50% annual run rate – the stock should be fine even with higher rates.

Alphabet (GOOG & GOOGL): Clients are only long GOOGL or the Class A shares: (2% mky cap weight and ranked 5th in SPY as of 4/22/22)

Alphabet also reports Tuesday night, April 28th after the closing bell with Street consensus per IBES data by Refinitiv expecting $26.11 in EPS on $68 billion in revenue for expected y.y growth of -1% and 23% respectively. Briefing.com shows consensus at $25.68 in EPS on $67.9 billion in revenue, which is a smidge lower than IBES’s consensus.

In Q1 ’21, Alphabet grew revenue and EPS 34% and 166% respectively, and Q2 ’21 was even stronger at 62% revenue growth and EPS of 169% respectively, which are remarkably strong numbers so GOOGL is still facing down tough comp’s for another 90 days.

The problem w GOOGL is that the Street was looking for just an expected 4% EPS growth for calendar ’22, for the last 3 quarters and that hasn’t changed yet, so the results and guidance for ’22 are everything Tuesday night.

Looking at notes from Q4 ’21, it shows that cloud and YouTube revenue growth both fell short of consensus for Q4 ’21 for the search giant. Also, Morningstar is modeling 18% revenue growth for ad spending for ’22, which may be in question now.

Trading at an “average” PE of 18x for expected 12% average growth over the next 3 years, the stock isn’t really expensive, particularly given the low assumption of 4% EPS growth in calendar ’22.

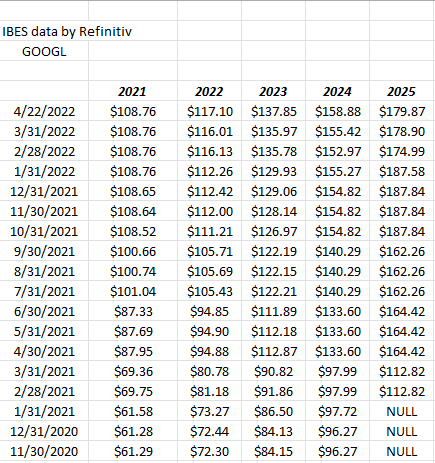

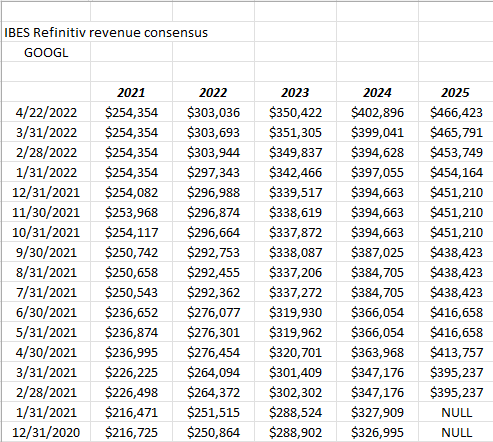

GOOGL’s EPS and revenue estimate revisions:

The EPS and revenue revisions for GOOGL actually look pretty solid. If there is a disappointment brewing in the numbers or the guidance, it doesn’t look to be in the numbers yet, but then again neither was Netflix’s mess.

Cash on the balance sheet is 9% of the now-depressed market cap, and cash-flow valuations are roughly 17x and 25X cash-flow and free-cash-flow.

The stock split is scheduled for mid-July ’22 per Briefing.com.

Facebook – Meta Platforms: (FB): (SPY portfolio weight of 1.17%, ranking 11th in the SPY as of 4/22/22)

Looking at the daily chart (Worden TC2000 Gold) Facebook closed below the early March ’22 lows of $185 and change by $1, closing Friday, 4/22/22 at $184.11, which is probably not a plus for the social media giant, but too close to call it a technical breakdown for the stock.

Facebook Meta (hereby known as just Facebook or just FB), reports Wednesday night, April 27th, 2022, after the market close and IBES by Refinitiv consensus is expecting $2.56 in EPS on $28.2 billion in revenue for expected y.y growth of -22% and +8% respectively. Briefing.com’s consensus is expecting $2.51 in EPS on $28.22 billion in revenue.

The Q1 ’22 revenue guide coming out of Q4 ’21 killed the stock as it fell from $330 to $200 and is now lower again pre-earnings, as margin compression is expected to be significant this calendar year.

Trading at 13x forward expected 3-year EPS growth of 6% (an expected 11% decline in EPS is expected for calendar ’22) the PE is still a little pricey but FB’s cash-flow valuation is reasonable at 9x and 14X cash and free-cash flow.

Like GOOGL, FB has cash and equivalents of 9% – 10% of market cap on the balance sheet as of 12/31/22, so share repurchases at these levels make more sense, but are still not ideal.

The one line that caught my attention after the Q4 ’21 earnings report came from Jeffries I think, the firm noted that Quest 2 Oculus headset was still just 3% of FB’s total revenue but would make a great on-ramp for the metaverse for the younger generation.

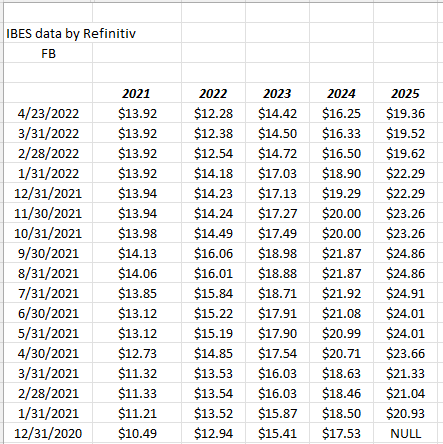

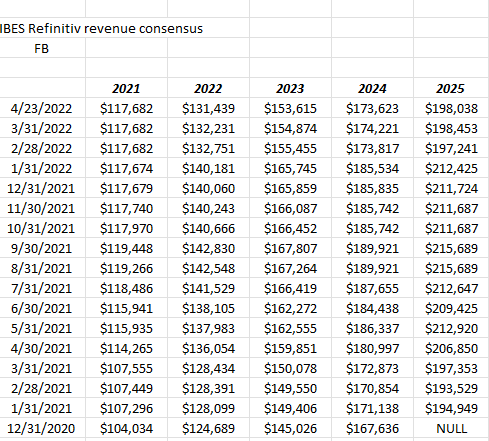

EPS and revenue revisions:

Readers can see how FB’s calendar 2022 and 2023 EPS estimates have fallen 25% since the late 2021 peak prints. Revenue estimates are also being revised lower but not to the same degree.

It’s tough owning stocks where EPS and revenue revisions are consistently negative.

Clients still have a small amount of FB in some select accounts, but the majority was sold in late 2017 – 2018 with the President’s China tariffs and along with the Cambridge Analytica mess. FB would need to trade down to around $150 per share to get to the area where FB was sold in the vast majority of accounts. (Two clients who are very tax sensitive still own the stock with a $19 and $27 cost basis respectively.)

My own opinion on the stock right now is to wait and see how the Metaverse evolves before owning FB again. The other thing too is Mark Zuckerberg lied to shareholders around Cambridge Analytica, saying shareholder data wouldn’t be shared and then silently let these firms access this data, and personally it left a bad taste in my mouth about Mark and his modus operandi.

Conclusion / Summary: After last week, and Jay Powell’s comments, this market is all about interest rates and PE compression.

Rather than include Apple’s and Amazon’s earnings previews for readers, the goal with today’s update is to keep this an easy read and allow readers to take your time digesting the data, rather than fight through an SP 500 earnings-related “War & Peace”.

Tech and Growth is struggling in 2022, which is perfectly understandable, but while the headlines are all about Ukraine and inflation, I think this is all about the Fed / FOMC / Powell scaring the daylights out of investors with an unprecedented series of rate hikes.

The technicians were talking about the breakdown in Google late last week, but the EPS and revenue revisions look fine to me. And again I have to warn readers that – like a Netflix – the analysts can be late to catch a major change to fundamentals.

Expected 3-yr avg rev gro:

- GOOGL: +16%

- MSFT: +16%

- FB: +14%

Expected revenue growth (Q1 ’22):

- GOOGL: +23%

- MSFT: +18%

- FB: +8%

Expected 3-year avg EPS gro:

- MSFT +16%

- GOOGL: +12%

- FB: +6%

Expected EPS growth: (Q1 ’22)

- MSFT: +8%

- GOOGL: -1%

- FB: -22%

Free-cash-flow yield:

- FB: 7%

- GOOGL: 4%

- MSFT: +3%

Cash-flow valuation:

- FB: 8 – 9x

- GOOGL: 17x

- MSFT: 25x

Free-cash-flow valuation:

- FB: 12x – 13x

- GOOGL: 24 – 25x

- MSFT 35x – 36x

Given all of the factors listed above, GOOGL would be the top pick coming into earnings, but readers need to be absolutely aware that a negative surprise would likely mean a 10% – 15% haircut for the stock even with the recent decline. However the upward revisions to GOOGL’s EPS and revenue estimates were surprising. Usually in a market like 2022’s analysts get more cautious. FB likely needs more time to base and investors need to see what the metaverse actually might look like for users.

Take all this with substantial skepticism. Growth stocks do not like higher interest rates – that’s the story this year. Do a lot of homework and know that – like Netflix – the bottom can fall out of higher PE growth stocks when growth slows.

Tesla’s price reaction to a great quarter i.e. higher margins, strong free-cash-flow and all around “better-than-expectations” was a great example of how risk isn’t being rewarded in this market.

Apple and Amazon’s earnings preview (Part 1) will happen in the next few days.

Thanks for reading.