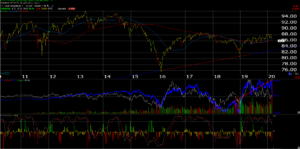

HYG is testings it’s 200-week moving average, but is still above the upwardly-sloping trend-line off the Q1 ’16 lows.

With the 50 bp’s fed funds rate reduction by the Fed, high-yield credit is always worth watching. With the Fed rate cut on the last day of July ’19, the high-yield market actually sold off a little as it did again yesterday, only to recover later in 2019.

The June ’19 lows for the HYG are just under $85 ($84.47) and the trend-line off the first quarter, 2016 lows is around $83.

——————————

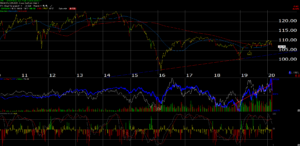

This is a weekly chart of the JNK, another similar corporate high-yield ETF that is watched as a high-yield proxy.

The JNK has traded clearly through its 200-week moving but remains above the upward-sloping trend-line off the Q1 ’16 lows.

Comparison: Both ETF’s have the lion’s share of their credits in the Single-B / Double-BB range, (north of 80% of each ETF) and both have their respective Energy weighting’s around 10%. JNK’s current yield looks a little bit higher than HYG’s at 5.46%, vs 5.02%, with a slightly lower expense ratio too. The Energy sector (you’d think) would be the problem credit sector and the high-yield sector weightings at 10% are far higher than the SP 500’s market cap weight for Energy at 3.5% – 4%.

Summary / conclusion: The recent downgrade of Kraft-Heinz became an issue for the corporate high-yield bond market since the $30 billion in debt outstanding makes it a big issuer for the junk bond market to absorb. Coupled with Covid-19, the high-yield market is seeing it’s first decent selloff since April – May ’19. Junk had a good year in 2019, returning just over 14%. mirroring the “risk-on” SP 500’s return of +31% for the year.

Even with the 50-bp reduction n fed funds yesterday, fed funds futures another reduction is scheduled for the next meeting on March 18th, 2020, so more liquidity you would think would be a plus for the asset class, even though both the HYG and the JNK finished down on the day yesterday.

Clients are long one high-yield mutual fund today (PIMCO), because it’s tough to get excited with the asset class with current yields of 5% – 5.5%.

Looking at expected defaults rates from Moody’s and Standard & Poor’s the last few years the expected default rates of 2% made sense to own high yield.

Normally, a 10% current yield would be required to own a near-market weight in high yield of 12% to 15%, but with a 10-year Treasury yield of under 1%, if the ETF’s like JNK and HYG would back up to 7% – 7.5%, the high-yield asset class would warrant a bigger allocation, and again that’s assuming that the US economy doesn’t dramatically decelerate.

Just writing to keep an eye on what is happening within the asset class.

Thanks for reading.

Remember, any opinion expressed on this blog is just that – an opinion – and it should be taken with a substantial grain of salt, as any opinion should. Readers should evaluate the content of this blog in light of their own financial profile. The markets can change quickly and content here may or may not be updated.