FedEx (FDX) the transport giant reports their fiscal Q2 ’20 financial results after the bell on Tuesday, December 17th, with consensus Wall Street estimates being $2.76 in earnings per share (EPS) on $17.58 billion in revenue for expected year-over-year declines of 32% and 1% respectively.

The good news is that – starting with the November ’19 earnings release, FedEx begins to lap the awful compares of the last 4 quarters.

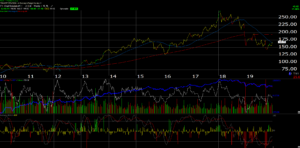

The peak in FDX’s stock occurred in late January, early February ’18 when the stock peaked at $274 per share but since then the China trade and tariffs issue, the supply-chain rerouting that has gripped industrial America, the slowdown in Europe on trade and Brexit issues, and the growing competition to FedEx Ground from the Amazon Prime trucks and one-day delivery has taken a significant toll on the stock. That doesn’t even include the hack of FedEx’s biggest European acquisition, TNT, which impacted that business and it’s integration into FedEx as a whole. (The TNT integration was scheduled to take 12 quarters or 3 years, so it will be interesting to hear where Fred Smith (CEO) and Alan Graf (CFO) think that stands today. According to sell-side comments a few quarters ago, the integration should be in the 9th or 10th quarter.)

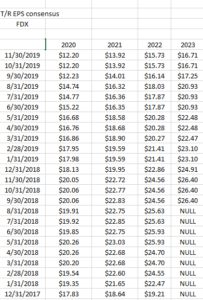

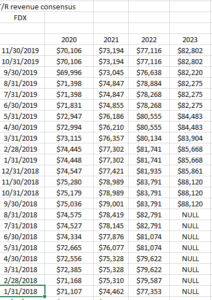

EPS and revenue estimate trends:

As readers can see, the fiscal 2020, and 2021 EPS estimates peaked in early 2018, a few months after the stock peak and have fallen dramatically since. Have the EPS estimates bottomed ? There is usually a lag between the stock price peak or trough and the trend in estimates,so be patient, but with the trade deal and Brexit scheduled for January 31, 2020 investors and CEO’s have more clarity on trade and Brexit rules and thus there should be some pickup in international trade.

To give readers and investors an idea of the operating leverage in FDX, revenue estimates haven’t declined nearly as much as EPS estimates, which is typical with businesses with high fixed costs.

The decline in revenue estimates from early 2018 for fiscal 2020, has been less than 3% versus the 40% decline in the fiscal 2020 EPS estimate,

The Issues:

The obvious issues like the China tariff tiff and the never-ending Brexit debate are now either behind us in the form of Phase One of the China Trade deal AND the USMCA agreed to last week, or will soon be settled as Boris Johnson has set a firm date of January 31. 2020 for Brexit to happen.

While the trade deals impact FedEx Express – 52% of revenue but operating income has fallen to just 29% of FedEx’s total operating income as of Q1 ’20, FedEx Ground and the encroachment by Amazon is a little worrisome. Fred Smith has described the worry as “fantastical” years ago, but Amazon with 1-day delivery seems to have upped the ante’ and pressure on Ground, which was 30% of total FedEx revenue as of Q1 ’20 but 66% of operating income. (FedEx took a charge for TNT integration, whicj I assume would have been flushed through Express, hence the drop in Express operating income in Q1 ’20.)

The other issue for FedEx is free-cash-flow generation: FedEx’s cash-flow and free-cash-flow is tracked every quarter on the valuation spreadsheet (acquisitions are INCLUDED in capex for free-cash-flow calculation purposes) and 9 of the last 12 quarters for FedEx has been free-cash-flow negative on a trailing 4-quarter basis. Q1 ’20 which was the quarter ended Aug ’19 saw a free-cash-flow deficit of $850 million, which is sizable, although to be evenhanded with FedEx, the first fiscal quarter of every year is typically free-cash negative.

The chart:

FedEx has moved back over its 200-day moving average which is a key level for chart watchers. Let’s see if “post earnings” the stock can stay above the 200-day and 50-week moving average. FedEx traded as low the high $140’s after December, 2018’s earnings release, so a trade below $145 wouldn’t want to be seen by those who are long the stock.

Summary / conclusion: After falling almost 50% from its January ’18 highs, FedEx is trying to steady the ship and the trade deals, (China and USMCA) and ultimately Brexit should provide substantial clarity to an international trade environment that was murky at best and completely unnavigable at worst. (How as a CEO do you plan for the next 1-year or 3-year capex when you have no idea what the trade rules or reg’s will look like ?)

The newer problem for FedEx is now what about the domestic US Ground business and will that be the albatross that slows the Ground giant ?

I was out for dinner last week at a restaurant in the western suburbs of Chicago talking to an old trucker guy (older than me, owned a small trucking company his whole life) and he made the point that Amazon would not have gotten into the business without the goal of dominating it eventually.

However reading the August ’19’s quarterly conference call notes, Fred Smith gave the metrics on the Ground and package business and it sounded like FedEx was viewing Ground as a continuing opportunity rather than a threat. Hearing about businesses like Uber Freight and other start ups as I see more and more Amazon Prime trucks rolling around Chicago and the ‘burbs, has me nervous for sure.

Clients have less than a 1% position in FedEx that’s been built over the last year, which includes a $36 cost basis position from March of 2000. More FedEx will be added here – maybe even a little before the Tuesday’s results – since i think Fred Smith and Alan Graf are one of the best management teams in the Transportation sector.

FedEX is trading at less than 1x revenue, 8x cash-flow and 14x 2020’s current estimate of $12.

What will be watched after the report (and assume it will be bad news, but the comparisons get far easier in fiscal 2020 and fiscal 2021) will be the trend and magnitude of EPS and revenue revisions, what Fred Smith and Alan Graf might say about the signing of the trade deals and how fast some of this traffic can recover, and what free-cash-flow guidance might look like.

Readers should assume the numbers will continue to be bad for the next two quarters.

Thanks for reading.