As the 4th quarter, 2012 winds down and with all eyes focused on Washington, it has been a better year for stock and bond returns than many expected. The S&P 500 is up roughly 15% – 16% year-to-date, and the Lehman Aggregate will end the year with an increase of 4% – 5% (approximately).

In terms of S&P 500 (and per ThomsonReuters), the “forward 4-quarter” estimate for S&P 500 earnings is now $108.91, down slightly from last week’s $109.09, and towards the lower end of the 3-month range of $107.89 from Sept 28th, and $112 from October 5th. This pattern is typical of how earnings estimates “evolve” during a quarter. The forward estimate tends to get revised downward through the quarter, and then we will see a nice “pop” in that forward estimate as we roll into the first week of January, as the old quarter rolls off and we add the next forward quarter to the estimate.

With 3rd quarter, 2012 financial results all but reported (497 of 500 companies have reported their 3rd quarter, 2012 results already), the calendar 2012 earnings estimate for the S&P 500 is $101.38 as reported by ThomsonReuters (7 estimates), and I would expect that to drift a little higher as the 3rd quarter results are finalized, and the 4th quarter starts getting reported in early January.

Thus, the S&P 500 is trading at 13(x) those forward earnings expectations.

Last week, Jeff Miller, the erudite blogger that authors “A Dash of Insight” every week (http://oldprof.typepad.com/a_dash_of_insight/) called me out on my comment that I thought the S&P 500 was “fairly valued”.

When I look at S&P 500 earnings growth expectations for this year and 2013, year-over-year growth for S&P 500 earnings is expected at 4% in 2012, and 10% in 2013, and if you average the two you arrive at 7%. A 13(x) multiple on the S&P 500 currently is roughly 2(x) the average growth rate of the two years, so on a P.E-to-growth basis, the S&P 500 is thought by some to be “fairly valued”.

As a smart lawyer once said, “I can argue it either way”, but like a lot of folks in this business, I tend to think the risk / reward in terms of asset allocation is more favorable to stocks (more reward) than bonds (more risk).

This article from Brian Wesbury, First Trust’s excellent resident economist from November 5th, 2012 (http://www.ftportfolios.com/Commentary/EconomicResearch/2012/11/5/election-matters,-but-stocks-are-cheap) makes a compelling case for the US stock market.

While the Washington discussions have thrown a temporary wrench into market forecasts and have have resulted in economic predictions ranging from Armegeddon to cautious optimism. I hear a lot of recession talk about 2013 that guys like Jeff Miller and Doug Short have shot considerable holes in the last 12 months, starting with the August, 2011 market selling. Even though I don’t personally agree with the tenor of the discussions coming out of Washington regarding higher taxes, I just dont think 2013 will be that bad, unless the President really loses all perspective about America and Americans, and their willingness and ability to want to get out of bed each day and control their own destiny economically.

Ultimately, I think there will be a reasonable compromise from Washington and the taxation issue, and Americans will get about “the business of business” in 2013.

————-

Each week, in this opening section, we like to leave readers with a “stat (or stats) of the week” and this week we look at equity market returns across the various market cap ranges and investment styles. What struck me is that this has been a fairly unform year for most equity investors, even as money continues to flow out of actively managed equity funds: (Source: JP Morgan’s Weekly Market Recap as of 12/17/12)

Large-cap Value +16.2%

Large-cap Blend +14.9%

Large-Cap Growth + 14.1%

—–

Mid-Cap Value +16.5%

Mid-Cap Blend +15.3%

Mid-Cap Growth +13.9%

—-

Small-Cap Value +14.2%

Small-Cap Blend +12.7%

Small-Cap Growth +11.2%

From the data, I would attribute a slight edge to larger-cap and a slight edge to “value” over “growth”. The biggest return disparity is between small-cap growth and large-cap value, which is a 5% difference. (I wonder how much of that disparity is Apple (AAPL) ? (long AAPL).

———–

Sector / Security / Market comments:

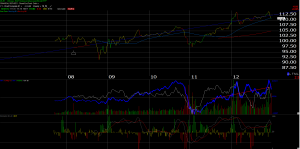

* Muni’s had a tough week – the MUB ETF looks to be in the early stages of a breakdown (see attached chart). Note the “double-top” in the attached chart from February and then late November. We have sold all of our muni exposure and have left the proceeds in a municipal money market waiting to see what happens. It could be interest-rate related, but I suspect that the tax-exemption that favors municipal bonds might be on the table in 2013 as Washington looks for additional revenue. Here is our blog update from November 17th that details our early comment on muni’s:https://fundamentalis.com/?p=780

* How bad was Citi’s downgrade of AAPL Monday morning, only to see the stock finish higher on the day? Analysts are pulling in AAPL’s 2013 and 2014 earnings estimates as they did in last year’s December quarter, only to get caught with AAPL’s outstanding earnings report in Jan, 2012. Is past prologue ? Hard to say, but it sure looks like AAPL is basing here. It has absorbed a lot of selling and negative commentary and NOT broken that November ’12 low near $500. The stock remains cheap at 7(x) 4-quarter trailing cash-flow (ex-cash). In last year’s December quarter, AAPL grew revenues 73% year-over-year, after growing just 39% in the September quarter of 2011. Not one of our world-class brands i.e. Coca-Cola (KO), Nike (NKE), Procter & Gamble (PG), Johnson & Johnson (JNJ) trades as cheaply as AAPL, right here and now, even though AAPL has substantially higher revenue and earnings growth. (Long all those stocks just mentioned.) There is still that “gap” on AAPL near $425, from the January earnings report that worries me – those technical gaps tend to get filled.

* Ford (F) finished strong on Friday, December 21, and closed right at its high of the day on 2(x) average volume. Some of our value stocks are getting a push late in the 2012. One of our worst sales this year was Applied Materials (AMAT), a value stock, at $10.15, now trading over 10% higher. AMAT also closed Friday on good volume. (Long F).

* Our PC sector call in early October (October 4 to be exact, and here is the link https://fundamentalis.com/?p=508) was too early (and wrong), but we took our first positions in Dell (DELL) and Hewlett-Packard (HPQ) this week, in a long-term, patient account. These are small positions to start, and we’ll buy more Dell at $9.80 – $9.85, and and more HPQ after we see the stocks base. I think the PC sector is more about job growth than tablets. While tablets will see cause some market share erosion, as will the Cloud, there is too big of an installed base of PC’s to say that the Windows – Intel platform is completely dead. We havent owned Hewlett (HPQ) since the late 1990’s, 2000. I like Meg Whitman, but she has been buffeted and rocked by one problem after another. Even “stability” would help Meg and HPQ today. Also, I think the Windows 8 re-design to touch from the mouse and GUI will simply take time for corporations to adapt to, and get comfortable with in terms of training their employees. The Windows 8 “touch” couldn’t have come at a worse time for the sector, but that is opportunity for those that are patient.

* Financials: Meredith Whitney finally came around to our conclusion here (https://fundamentalis.com/?p=678 ) that financials are a good bet, even in 2013. We’ve been blogging that – given the 2013 estimates for the financial sector, the stocks look like they have more upside than downside. However, Elizabeth Warren was put on the Senate Banking Committee, and she is no friend of the banks. Some think they will be (essentially) regulated utilities, for years to come. I’m not that negative though. Essentially the banks are a tangential play on the housing recovery and a lending recovery, while the proprietary trading revenue is gone from the income statement. (Not sure how much of the big bank’s earnings prop trading represented.) If nothing else, with the death of prop trading, the financial sector estimates become more stable, and stable might be “better” in 2013. (Long JPM, WFC and GS.)

* Good week for Goldman Sachs (GS) – rallied again and is testing that March ’12 high of $128.72.

* Gary Morrow, a hedge fund manager in San Luis Obsipo, California tweeted http://twileshare.com/aaun, this chart of Wal-Mart (WMT) this week. We like the stock down to $65. Had a monster run in 2012, but has given a lot back since mid-October. Talk about an earnings juggernaut in terms of consistency. One of the best (and most mis-understood) businesses in America today. The story is those US “comps”and the Cliff complicates that story, although the President seems to want to protect Wal-Mart’s typical demographic. (Long WMT – want to buy more.)

* High yield (i.e. junk bond) spreads are still tightening as are low investment-grade bond spreads. Here is a tweet (http://twileshare.com/aabo) from Norm Conley of JA Glynn out of St. Louis on historical levels of Baa yields. If there is a recession in the offing, my guess is that we will see it earliest in credit spreads.

* BBBY was our best call this past week. Here was our earnings preview http://seekingalpha.com/article/1065581-why-we-worry-about-bed-bath-beyond-heading-into-earnings. The stock was down 4% on the week. Nike (NIKE) was our worst call this week and shows how hard it is to gauge world-class brands. The valuation is extreme, but the company continues to execute. Here was our earnings preview http://seekingalpha.com/article/1073161-nike-earnings-preview-waiting-on-the-iconic-brand-to-sink-into-valuation, and we couldnt have been more wrong. Nike up sharply on Friday in a tough tape.

Thanks for stopping by and thanks for reading. Have a wonderful holiday and New Year.

We will be posting during the holiday weeks on topics of interest.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager