According to the Chicago Merc’s fed funds futures contract there is a 98% chance that the new fed funds range will be 1.50% – 1.75% which would obviously be a 25 basis point reduction in the FOMC’s fed funds target.

However Apple and Facebook report after the closing bell tonight, and I’d like to focus on Apple for readers, just because the iPhone has become the new “consumer staple” of the Technology world. (That comes from an Ariel Capital portfolio manager – can’t recall her name, in a presentation to the CFA Society of Chicago in Spring ’18.)

Facebook has a bigger moat around their business but I do think the three damaged brands today that have occurred the last few years remain:

- 1.) Facebook

- 2.) Boeing

- 3.) Wells Fargo

However the fact is, all three stocks act quite well given their respective headlines and newsflow.

So What’s Up with Apple ?

Because many of our client’s have taxable accounts with us and thus are “capital gains adverse” the major changes to client accounts the last two years were to sell Apple and Facebook in 2018, with most of the sales for both occurring between $155 – $175.

The worries over Apple were (or are):

- Technology hardware brand which was consistently trying to push through price increases on the Apple phone, which was completely antithetical to the traditional “tech hardware” (i.e. Moore’s Law) model;

- The stock has been a dramatic outperformer since early 2000, in the midst of a substantial business model transition.

- I wondered if Apple’s thoughts of trying to price Apple iPhones at $1,000 per model would eventually be too much for consumers

- No mega-cap giant from the 1990’s (or ever, thinking of IBM, ATT, etc.) had successfully transitioned its business model from a dominant technology to another dominant (i.e. wide-moat) technology without a substantial correction in business fundamentals. (Hopefully readers can give me examples of when and where that has happened to correct my substantial ignorance).

- The biggest reason for the sale of Apple was this quality of earnings issue which, with cash-flow of net income at 100% isn’t horrible, but the fact is the trend had deteriorated markedly perhaps indicative of some internal stress.

- In 2018 when the majority of the stock was sold for clients, the China trade talks were a major concern (of mine).

- Here’s the spreadsheet showing casg-flow vs net income:

(The attached spreadsheet from our fundamental homework shows the trend in cash-flow-vs-net income.)

Tonight, the Street consensus is expecting $2.84 in earnings per share on $62.9 billion in revenue for expected year-over-year growth of -2% EPS growth and 0% revenue growth. The all-important December ’19 quarter which is the first quarter of fiscal 2020, is expecting $4.45 in EPS and $86.9 billion in revenue for expected y/y growth of 6% and 3% respectively.

Full fiscal 2020 consensus is currently expecting 10% EPS growth on 3% revenue growth, so guidance will matter tonight, but expectations seem reasonable coming into the release tonight.

Summary / conclusion: The fact that Tim Cook and Apple stopped disclosing Apple iPhone unit info last December ’18 validated our sale decision last year, but if Services and Apple’s non i-Phone related businesses can truly grow at a clip that will sustain the growth needed for a stock with a $1 trillion market cap, then selling the stock was – in hindsight – not a great decision. Could Apple become IBM, or AT&T as dominant or formidable as those franchises were in their heyday ? Doubtful but certainly not impossible.

As an Apple iPhone owner, my battery is a constant issue with the phone (and that’s probably true regardless of the brand) but I’ve wondered how long consumers will put up with that.

My iPhone upgrade will likely come next year with 5G, but it will happen.

The growth in Apple Services will have a gross margin almost twice that of the iPhone business, but the question ultimately remains how fast can Apple grow that Services business so investors can stop worrying about the iPhone and focus on the Services business.

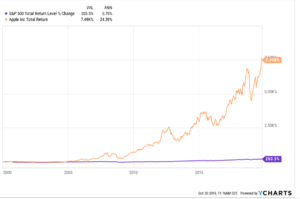

Readers will be left with a final YCharts graph showing Apple versus the Sp 500 since the 1/1/2000:

Similar charts could likely be shown for any number of the Technology giants versus the SP 500.

But for a consumer giant with narrowing margins and expected mid-single-digit revenue growth, albeit with a reasonable valuation, reducing the Apple position seemed prudent.

Thanks for reading.

(Take all opinions on markets and individual holdings with great skepticism. I write the blog pieces to impose the discipline to do the homework and to clarify my own thinking. Take or leave any or all of it but evaluate all material in light of your own risk tolerance and financial profile. None of the blog’s contents should be construed as a recommendation or “advice”.)