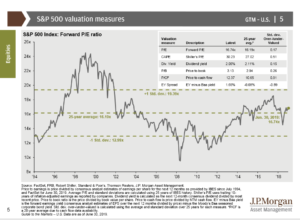

Dr. David Kelly and his team at JP Morgan put together – each quarter – one of the best capital market, economic and portfolio management summaries on the Street in the form of JP Morgan’s, “Guide to the Market”.

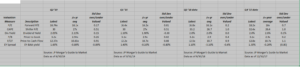

This valuation table is typically found in the first 10 pages of “The Guide”. Here is a spreadsheet summary of the last few years of the SP 500 Valuation Table:

Here is the actual chart from the June 30, 2019, Guide:

Looking at the far-right column of the valuation metrics, readers can see – either on the Excel spreadsheet or on the chart itself, that – as measured by standard deviation – the valuation measures are within the normal valuation ranges.

As a cash-flow guy, here is a blog post from May ’15, when the SP 500’s price-to-cash-flow valuation had just moved over 10x cash-flow. At 12x cash flow today the SP 500 is getting a little more salty, but hardly near 1987 levels or early 2000 levels of 27x – 28x PE.

Note too on the spreadsheet how valuation measures have compressed – that is a function of the flat SP 500 we’ve seen since late January, 2018.

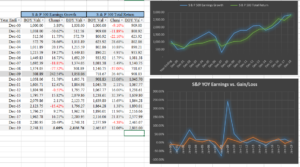

Speaking of PE compression:

This table and charts are from John Spencer, Director of Wealth Management of Hackman Financial in Cincinnati, Ohio. John and i went to school together in Cincinnati, and we typically chat about the markets when we have time to do so.

The top chart – yellow and blue lines show – show plainly that there has been little “PE expansion” in this bull market, since March, 2009.

To highlight John’s work, I took a look at SP 500 cumulative earnings growth from 1990 to 1999, versus the cumulative return on the SP 500 and SP earnings grew 79% cumulatively for the decade, while the total return on the SP 500 for the same period was 190%.

The point for readers is that there has been little to no PE expansion in this 10-year bull market despite the cacophony of the SP 500 being overvalued.

PE expansion is typically the hallmark of bull markets.

Gives the reader some idea of how this market remains so hated, even as it breaks out to an all-time-high.

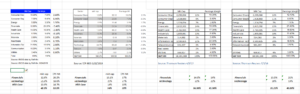

Market cap vs Earnings weight – is the Financial sector a screaming buy ?

Seeking Alpha has always been kind of enough to pick up the posts on this blog, and this recent post on Financials and the pretty substantial disparity between Financials earnings weight in the SP 500 and the sector’s market cap weight, elicited very few thoughtful responses.

You’d think – maybe as one investment strategy – that readers would overweight the sectors where the market cap was less than the earnings weight and underweight the opposite – but I have no historical data on how that strategy would have performed.

My own opinion is this “gap” is way too big, but also, I don’t know what breaks the Financial’s out of their malaise.

Maybe higher long-end rates, maybe a steeper yield curve (same thing), maybe faster economic growth, and maybe some combination of all three.

Q2 ’19 earnings should be interesting for the sector. Of the 11 sectors within the SP 500, Financial’s are actually expecting the strongest earnings growth for calendar 2019:

- Financials: +8.9%

- Health Care: +6.2%

- Cons Disc: +6.1%

- Industrials: +5.3%

- Utilities: +4.3%

- Real Estate: +4.2%

- Comm Services: +2.3%

- Cons Spls: +1.1%

- Technology: -2.8%

- Energy: -11.5%

- Basic Mat: -19.1%

- SP 500: +2.2% expected EPS growth for 2019 as of July 5, 2019

Are Financial’s being disintermediated or “disrupted” ? Sure, the sector is an easy candidate for that. All the banking system ultimately does is “wash money” in the non-criminal sense of the term.

It may be the new “retail” over the next 3 – 5 years, i.e. solid brands, attractive valuations and under-performing stocks.

Summary / Conclusion: This weekend’s blog post is chock full of various topics, so I hope readers can take something useful from the data, and spreadsheets and information.

While bullishness has increased of late and the SP 500 has made a new all-time-high, there is little excitement around investing and being in “the market”. Personally, I think that’s a long-term plus.

Q2 ’19 earnings begin in earnest with the Financial sector reporting the week after next, which is the week of July 15th, so don’t sweat what happens this week too much.

By late September, it’s expected that the “expected” Q2 ’19 SP 500 earnings of flat today, will be higher by 3% – 5%, which is the average “upside surprise” every quarter.

Thanks for reading.