Here are two charts of municipal bond closed-end funds (CEF’s) that we’ve been buying the last two weeks, buying first the Blackrock Muni Enhanced CEF (ticker MEN) and then adding the Nuveen Municipal Value closed-end fund (ticker – NUV) last Friday, August 2nd, 2013, after the payroll report.

Unfortunately, after writing this on our www.fundamentalis.com ((blog) this weekend regarding municipal cef’s:

“Municipal closed-end funds: we will be out with charts on Sunday and Monday, with technical commentary on a few positions from Gary Morrow, but we’ve added the Nuveen Municipal Value (NUV) closed-end fund to client accounts in the last week, as well as the Blackrock Muni Enhanced (MEN) closed-end fund to get both yield and technical support for clients taxable bond portfolios. We will save the fundamental write-up for the blog specific post, but we are finding a whole lot of muni closed-end funds at weekly oversold readings on our charts. What I do worry about is meaningful tax reform, which reduces or eliminates the favored tax exemption of municipal bonds for individual investors, given Congress’ and the President’s penchant for screwing the wealthy investor AND trying to boost tax revenue, BUT the catch is that current muni yields on some of these funds, rival the current investment-grade bond yield, which if you’ve followed muni’s for a while, means muni yields are trading at 100% of investment-grade corporates, which is truly cheap. If we used taxable-equivalent yields on the muni CEF’s, the muni market is approaching yields closer to taxable high-yield or 7% 8%, even as high as 10%. These tax-exempt yields discount a lot of potential trouble with an 8% to 10% taxable equivalent yield. Some of these closed-end funds could start to see “cross-over buying”, which means that they could get bought in IRA and tax-deferred accounts simply for absolute yield purposes. I know I’ve thought about it for some large IRA and Foundation accounts we manage, which are tax-advantaged already.”

Since our Saturday, 8/3/13 blog post we’ve read three different articles on municipal bond CEF’s from other sources including www.seekingalpha.com and www.marketwatch.com.

————

Here is Gary Morrow’s technical summary of the Muni CEF space as of this weekend:

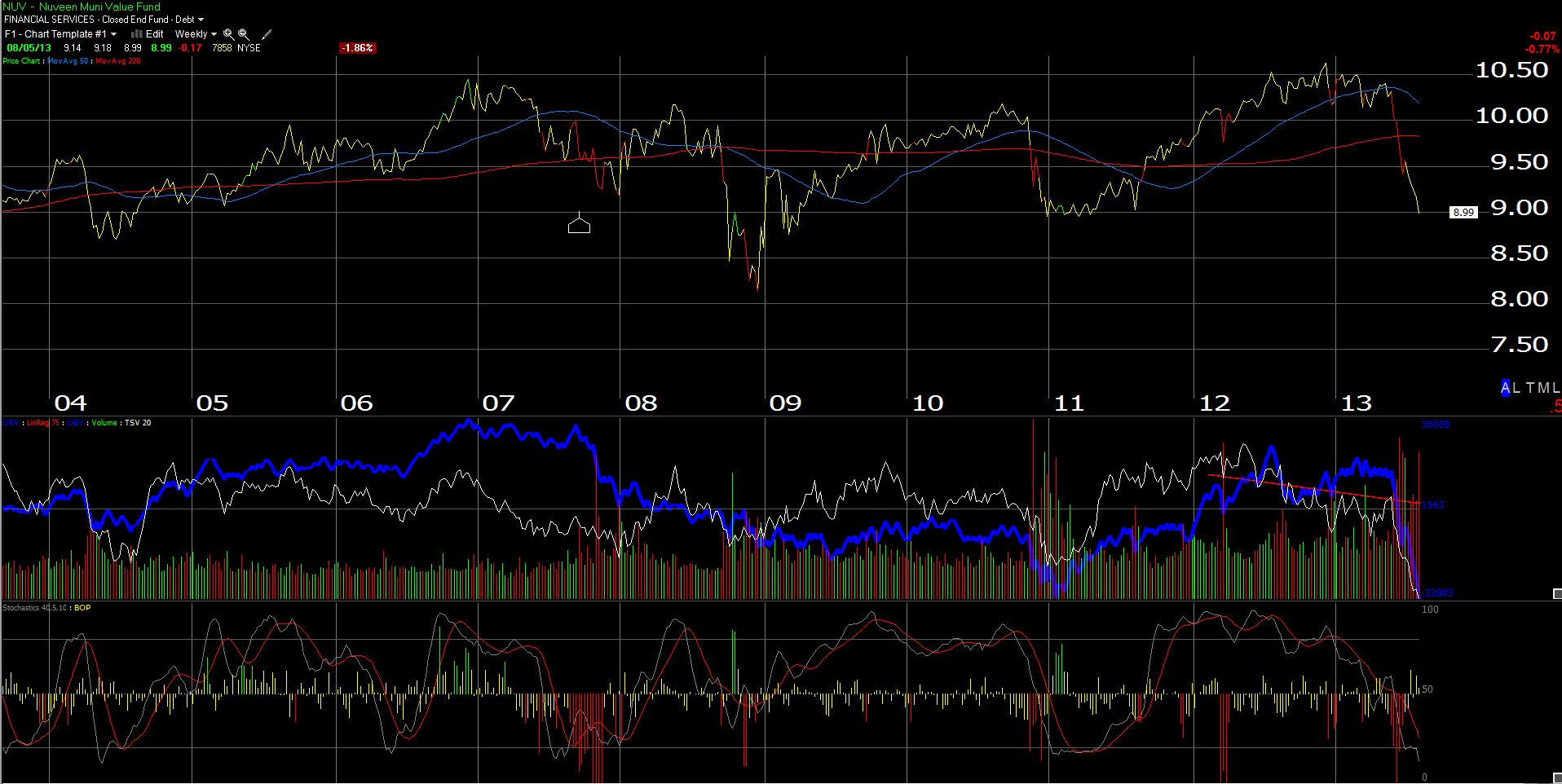

The massive distribution wave that has swept through Muni land during the last six weeks has created many opportunities. Very few, if any, Muni CEF’s have been left with only slight damage. As a group Munis have been pummeled since late May. There was a relief rally in late June that retraced over 1/3 of the collapse from the May peak in most cases. This momentum quickly wore off in early July but the selling through most of the month was far less intense. By the end of the month the initial June lows were being retested. This is could potentially set up many of the Muni CEF’s for an important bottom. One in particular is the Nuveen Municipal Value Fund(NUV).

Last week the NUV dipped down to the $9.00 area. Four weeks earlier, during the initial downward thrust, the NUV left behind a spike low here before a sharp five day bounce. This is the top layer of a key support zone that includes the 2011 lows of $8.75. A longer term view of the NUV action shows the CEF has reached a deeper oversold reading than that hit back in early 2011. On the daily chart NUV developing an interesting divergence in regard to its oversold status. We saw a slightly lower low in July while the oversold reading, as per MACD, is working on a higher low. This set up is indicative of an important bottom, or top when reversed, and could precede a healthy bottom.

Considering the major damage since late May a bottom may take some time. A period of light chop below the $9.00 area would not be a surprise. This type of action will result in rather low risk entry for patient bulls. The near panic selling that washed over just about everything interest rate related has created quite a few large distortions. I believe a very playable one is developing in Muni land.

———–

Here is my fundamental commentary of CEF’s by ticker:

Nuveen Municipal Value Fund (NUV): NUV is currently trading at 6% discount to net asset value (NAV), with a 4.9% distribution rate, which is closer to a real yield since there has been no return-of-capital. Thus for our clients, NUV represents close to a 11% total return if the discount closes within the next 12 months, and the yield is maintained or not reduced on the CEF. 38% of NUV’s municipal bond holdings are insured, the top 10 holdings represent between 6% – 7% of the CEF. NUV is sitting right at its 3-year low range, between a premium of +4%, and the current discount of -6.35%. About half of NUV is callable in the next 5 years per Morningstar’s recent analysis.

We added to NUV last Friday, August 2nd and bought more Monday, August 5th.

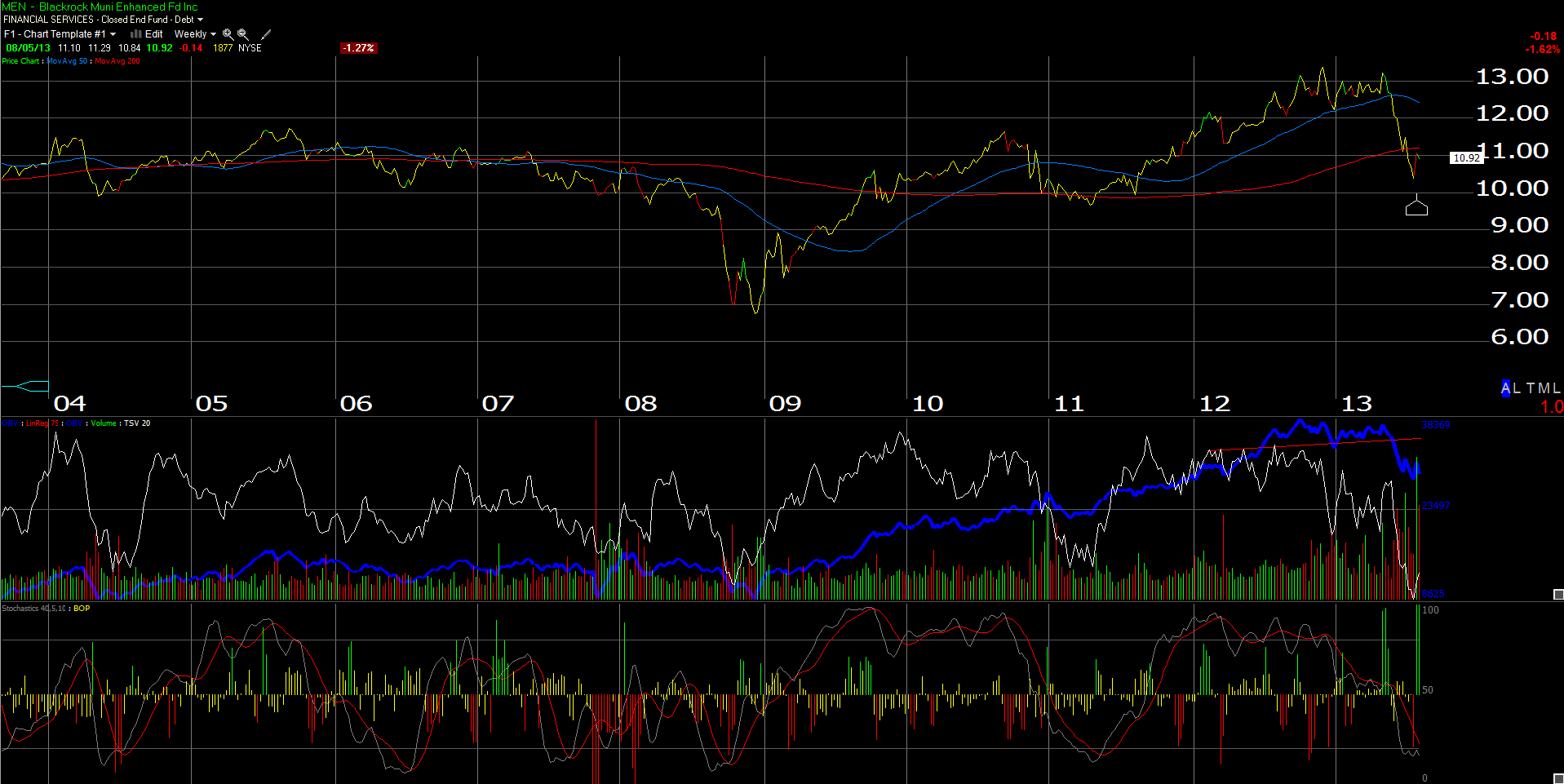

Blackrock MuniEnhanced (MEN): the Blackrock MuniEnhanced closed-end fund is trading at a smaller discount to NUV, but with better yield, and a longer duration at 9.0 years. NUV has a duration of just under 8.0 years.

MEN is currently yielding 6.5% (some of it taxable ) with a better monthly dividend and no return of principal.

Unfortunately MEN is not currently reviewed or surveilled by Morningstar, which does make me a tad more uncomfortable holding MEN. NUV is covered by Morningstar.

To summarize, MEN has better yield, but better taxable yield with a smaller discount to NAV, while NUV has a bigger discount to NAV, with s smaller yield, that is entirely tax exempt.

Here is Douglas Albo’s write-up on www.seekingalpha.com from this weekend the attractive valuation of municipal closed-end funds.

Here is Marketwatch’s article from yesterday on the Detroit – CEF impact on muni’s, as a similar theme.

It is hard to tell (for me) how much much of the discount in muni’s is Detroit, how much could be the looming impact of the repeal of the tax preference status of muni’s in general, and how much is interest rates and duration.

Muni’s are facing the perfect storm – we have picked away at NUV and MEN, and will be watching closely how the complex trades if we get a Treasury rally, and if we see the tenor of the tax conversation change in Washington.

Use the 2011 lows for each CEF as your stop-loss for exiting the trades. That would be the low $9.60’s area for MEN, and $8.75 for NUV.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager