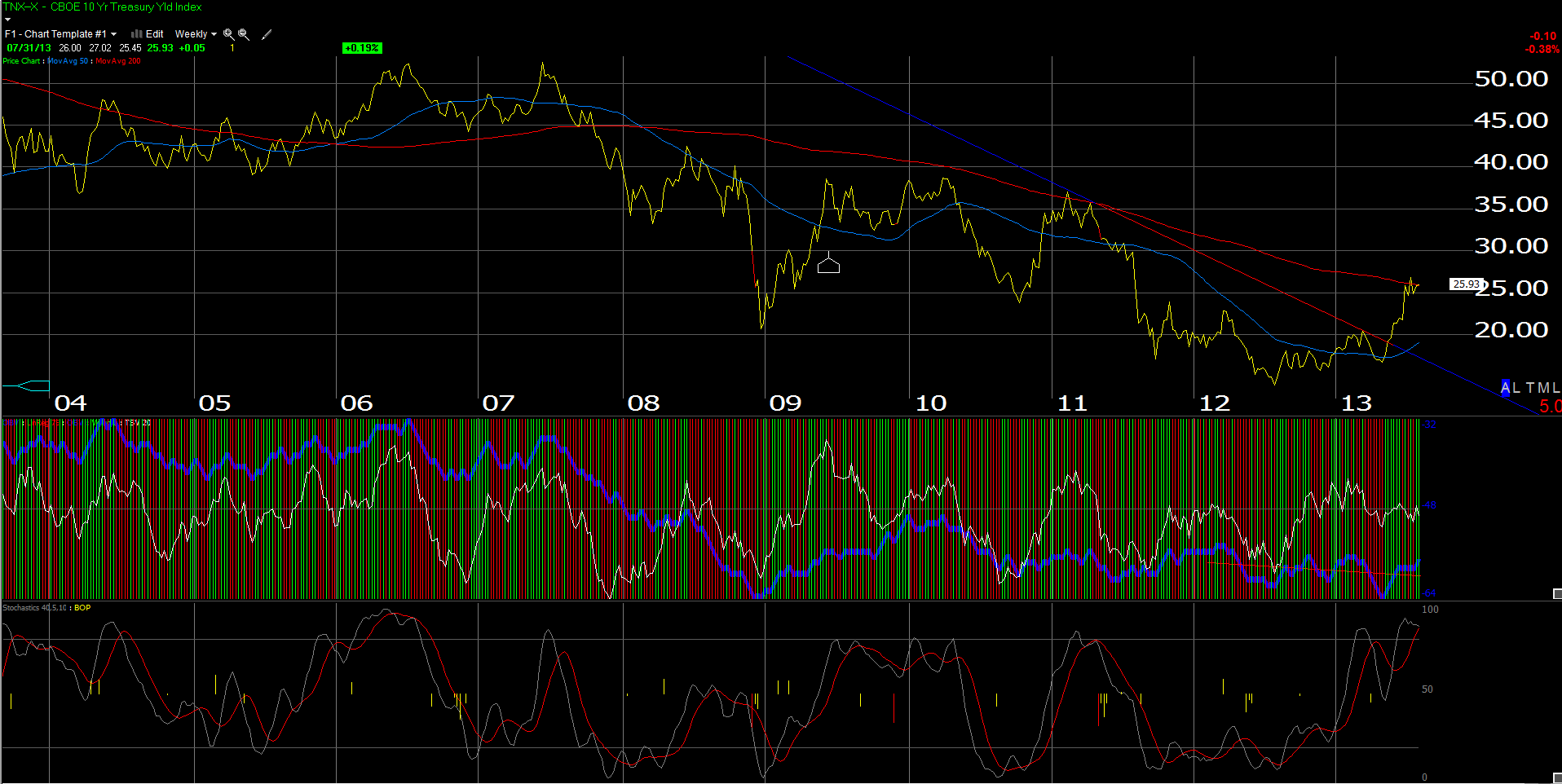

On top, is the weekly chart of the 10-year Treasury yield, (not price) bumping its head against key resistance in the form of the 200-week or roughly 4-year moving average for the key Treasury security.

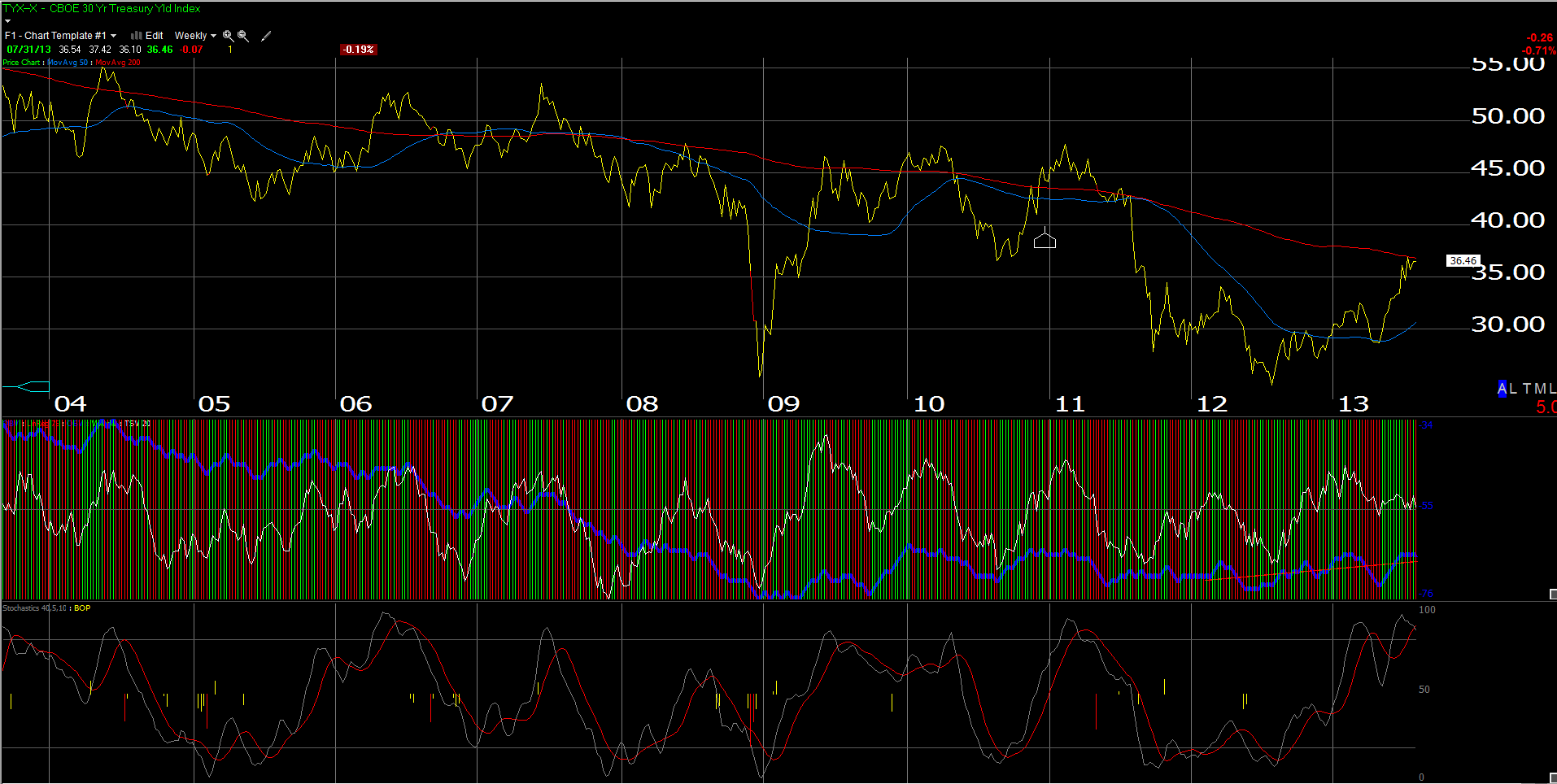

The 2nd chart is the 30-year Treasury yield, also bumping up against key resistance.

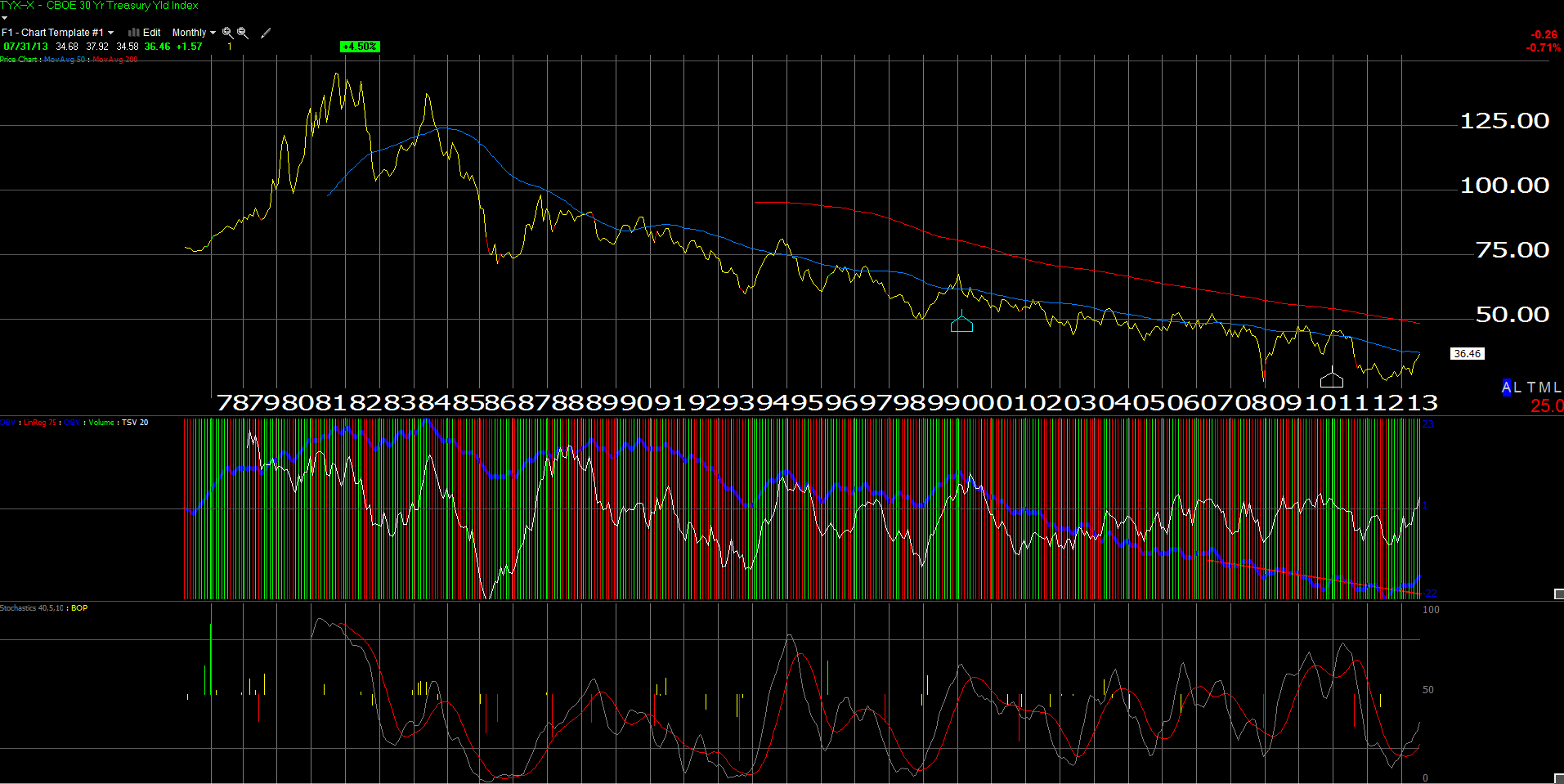

Finally the 3rd chart is the “monthly” chart of the 30-year Treasury bond yield, bumping up against the 50-month moving average, going all the way back to the 30-year’s inception issuance in 1978.

All of these charts, including this one from Norm Conley, a portfolio manager and managing partner at JA Glynn in St. Louis, shows that the Treasury complex is sitting at multi-year decade-long inflection points, possibly on the verge of long-term breakdowns across the Treasury curve.

My own opinion is that tomorrow morning’s August 2nd, July ’13 nonfarm payroll report could be the tipping point that takes us over resistance.

Consensus expectations are for 180,000 to 200,000 net new job growth for July ’13 for the US economy, and given Wednesday’s July 31 ADP private payroll number of +200,000 and today’s low reading in the weekly jobless claims data, expectations for a strong number have actually risen through the week. (It does worry me that expectations for a strong number have been raised through the week. The payroll data and the revisions, seem to be – at best – a wild guess by the Labor Deprtment and the Bureau of Labor Statistics (BLS).)

I dont know know if that means we could actually rally after tomorrow’s number, if we get – say – a 150,000 net new jobs number, but I think it is just a matter of time, before the 10-year Treasury trades through the 2.72% high tick from the first days of July, and Treasury’s break for good.

We think that Treasury’s are on the precipice for a MAJOR change in direction that could last years if not the rest of my life. Doug Kass, the famed hedge-fund manager at TheStreet.com used the term “generational low” for the SP 500 in March ’09 to describe that bottom, and we think that in hindsight, the July ’12 lows of 1.39 for the 10-year Treasury yield could be just a lovely thought by the end of 2013.

If the July ’13 jobs report is strong, and we get a 220k – 250k “net new jobs” print, I think you could still own Financials, but we would look hard at adding Basic Materials names that might participate in global recovery. No question Cyclicals, Financials, Technology and Large-Cap retail with international exposure would benefit from a resurgence in global growth. (Depsite Jim Chanos and the negativity around the name, CAT has hung in quite well. Earnings estimates have gotten crushed, and the stock still hasn’t broken support.)

The Chicago Mercantile Exchange (CME) and Charles Schwab (SCHW) / Ameritrade (AMTD) are higher interest rate and higher equity price beneficiaries.

If Friday’s number is weak, the homebuilders and possibly the dividend trade like Telco and Utilities might be good for a 30 to 60 day trade.

However, ultimately, I think the Treasury complex will breakdown and yield will push through this multi-year resistance, and global growth will return.

The SP 500 is trading at 1,700 this morning, and still the hedge fund, CNBC pundit crowd is bearish on the US stock market, despite a 19% year-to-date return on the SP 500.

We remain long the TBF (inverse Treasury) as our largest fixed income position in balanced accounts, offset with floating rate loan funds, and some closed-end funds at steep discounts. We are also still long some IEF and TLT as a reversal trade candidate for Treasuries given this long-term resistance.

Managing fixed-income money, assuming Treasuries break down, could be a very different prospect for clients, as it will be more of a game of “not losing” rather than “winning” i.e. outperforming via a simple duration bet, in the last 5 – 6 years. Absolute positive return might be hard to come by in the bond markets in the next few years.

Thanks for reading and stopping by:

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager