Next Friday, October 14th, 2022 is the big day for bank reporting next week as JP Morgan (JPM), Citigroup (C), Morgan Stanley (MS), US Bancorp (USB) and Wells Fargo (WFC) report before the opening bell. Blackrock reports their Q3 ’22 on Thursday, October 13th, 2022.

Since US Bancorp and Blackrock have never been owned by clients, those financials will not be covered here.

The big themes affecting the banking industry for Q3, 2022:

1.) Net interest income is accretive to EPS this year for the banks and financials for the first time in probably a decade as higher interest rates have allowed the banks to grow their spread income. The inverted yield curve is a bit of an issue but the banks tend to raise their “interest paid” slowly and reduce it quickly once the Fed starts to ease, so the rise in market rates along the yield curve have helped banks earn spread income.

2.) Credit is still good for the most part. Credit could be a push for banks since – even though credit is solid – loan loss reserves will likely be built and how much they are built and what bank management’s say about it could be a good tell on how deep they think a recession might be. Watching the bank’s credit card loss metrics which is reported every month, shows no material increase in charge-offs, and in fact credit loss metrics improved over the summer. Credit card losses are unsecured debt so the category is a good look into the credit health of the consumer. Plus, job growth is still positive so that’s another plus for consumer credit.

3.) Capital Markets will be a big drag for JP Morgan, Goldman Sachs, Morgan Stanley and possibly Bank of America. Debt refinancing for high-grade and high-yield debt has to be well below 2021’s compare given the rise in yields.

4.) Mortgage banking – with mortgage rates hitting decade highs this week, the results of mortgage banking operations will be obvious. Wells Fargo will suffer the most although JP Morgan and Bank of America will also feel that pull.

5.) The y.y compares for the financial sector get much easier as we move through 2022 and into 2023 as was covered here in early July ’22.

JP Morgan: (JPM)

JPM’s stock was down 32% YTD as of 9/30/22, worse than the decline for the financial sector in general which was down 21% YTD as of 9/30/22. In Q2 ’22, within JPM’s Corporate and Investment Bank, which is 32% and 43% of the bank’s net revenue and net income respectively, net revenue fell 10% and net income fell 26%. Each of the bank’s four main sectors, i.e. the Consumer Bank, the Corporate and Investment Bank, Commercial Banking and Asset Management, all saw net income fall y.y in Q2 ’22, the biggest reason being the very tough compare with Q2 ’21, which was covered here in July ’22.

Net interest income (NII) came in better-than-expected, while fees were worse-than-expected in the 2nd quarter, 2022.

Today, for Q3 ’22, JPM consensus is expecting $2.92 in EPS and $32 billion in revenue next week for expected y.y growth of -22% in EPS and +8% in revenue. If the bank hits the $32 billion in revenue that will be the strongest y.y growth since March ’21’s 14%.

Here is a quick look at JPM’s EPS and revenue trend revisions:

What I like about JPM’s EPS revision trend is the stability since the summer months or since 7/31/22 across 2022 and 2023. What’s not to like is the full-year 2021 EPS print of $15.03, since that print could be “peak EPS” for several years.

The one issue that has raised it’s head for JPM this year is CCAR (Comprehensive Capital Analysis & Review) that was instituted after 2008. JPM declared their $1 per share dividend in late September ’22, but the dividend wasn’t increased. The regulators and the economists seem greatly worried over the “The Next Coming Great Recession (in our own minds)” even though the US banking is probably better capitalized today than at any point since the early 1990’s after the then commercial real estate crisis. CCAR and the clamping down on financial services risk-profile after 2008 has actually done it’s job, but like all regulation and regulators, there is a tendency to “re-regulate” to remain employed.

JPM is trading at 9x the next 3 years avg EPS and revenue growth of 0% and +5%. After JPM grew EPS 73% in 2021, EPS is expected to decline 27% this year, both years of which are distorting the long-term averages of +15% EPS growth on +1 to +2% revenue growth (looking at the last decade from 2010 to 2019).The stock today is technically oversold on the weekly chart although I’d prefer to see JPM recover the $125 level, which is the point of the 200-week moving average. Although JPM’s price-to-book and price to tangible-book are 1.25x and 1.55x, not as cheap as other banks, this is the smallest premium that JPM has traded at to book value(s) in the last 7 quarters.

In normal markets and a normal economy, JPM should trade closer to $140 – $150 per share in my opinion particularly with a 14% return-on-tangible-common-equity (ROTCE) for Q2 ’22 so the stock is trading a 25% discount to what is thought to be “fair value”. That assumes a $13 – $15 EPS print for the banking giant, which might take another year or two to re-establish. (Since this article was written in early August ’22 over on Seeking Alpha, the SP 500 is down 9% and JPM is down 6%, so perhaps the stock is starting to discount all the news and interest rate volatility from earlier in ’22. The stability in the EPS estimate trend is probably helping.)

The stock is near “baseline” valuation so if you can look out 6 -12 months, you should be rewarded. At some point the regulators should take off the cuffs and allow well-managed banks to boost dividends and repurchase shares after they’ve built up capital. There is less than a 5% probability in my opinion, that the next recession is a repeat of 2008.

Morgan Stanley: (MS)

When Morgan Stanley reports Friday, October 14th, the consensus is expecting $1.49 in EPS on $13.2 billion for expected y.y declines of 27% and 10% respectively. Morgan Stanley does not have the EPS volatility of a JP Morgan or Goldman Sachs but it’s fortunes are still tied to the capital markets or stock and bond markets, and for 2022 that’s means MS has had a tough year.

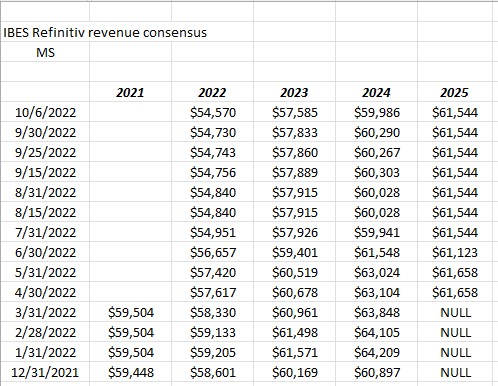

Currently, for full-year 2022, Street consensus is expecting EPS of $6.63 on revenue of $54.57 billion for expected y.y declines of -9% and -18% respectively. This is after 5 year -2017 to 2021 – where EPS averaged +23% year, respectively. Like Goldman and JP Morgan, Morgan Stanley will feel the pressure in the banking business first which as of Q2 ’22 as a percentage of their net revenue and pre-tax income, is roughly half the business.

James Gorman gave an interview in the last few weeks and wasn’t negative on the business in 2022 (presumably credit risk weakening) which in front of earnings in the next week is more positive than negative. The emphasis on wealth management and asset management since 2008 is helping the stability of the business and helping to temper EPS and revenue volatility, but in a year like 2022 where there is nowhere to hide, the stock is down 13% YTD, still outperforming both the financial sector and SP 500 YTD.

EPS and revenue trend estimate revisions:

MS’s estimate trends continue to be revised lower. Like JPM there has been a softening in revision severity since the summer of ’22.

With MS trading at 12x and 10.5x the expected 2022 and 2023 EPS of $6.63 and $7.77, like JPM it will probably take another year or two to recover the record $8.06 EPS print from 2021. That being said, the 3.75% dividend yield for MS is attractive, and per a note from the June ’22 conference call, MS is likely to repurchase $1.5 stock per quarter in 2022. Fair value for MS seems to be between $90 and $100 for a premium brand within both the banking business and the wealth management business, so the stock around $80 is probably not trading at enough of a discount to warrant a big position. Between $70 – $75 per share, I do think the stock gets to be too cheap. No positions are owned currently.

Citigroup (C):

Citigroup has been bought for clients for the first time since the 1990’s, in the last 6 months, although it’s a small position right now. The potential catalyst from an earnings growth perspective, could be the appointment of a new CEO, Jane Fraser and her emphasis on building Citi’s wealth management arm. Jane formerly ran Citi’s Consumer Bank so she has broad knowledge of the bank itself, which has attracted the attention of very good value investors like Bill Nygren at Oakmark and Berkshire Hathaway (long BRK.B stock).

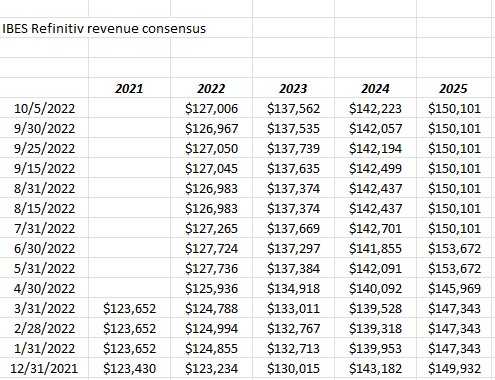

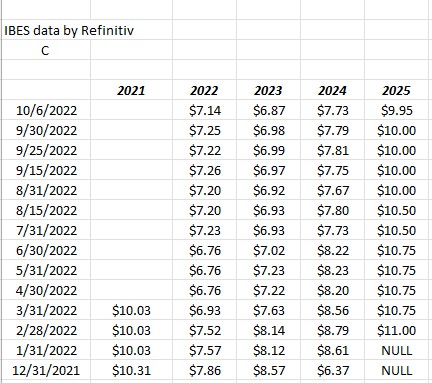

When Citi reports their Q3 ’22 financial results before the opening bell next Friday morning, October 14, analyst consensus is expecting $1.49 in EPS on $18.67 bl in revenue for expected y.y decline in EPS of 31% on 9% revenue growth. In Q2 ’22, Citi printed 13% in y.y revenue growth and a 23% y.y decline in EPS.

The real attraction to the stock is the current book value and tangible book value valuations of 0.48x and 0.64x, with the stock around $45 per share.

Trading at 7x forward earnings, with revenue growth in 2022, and at a steep discount to book value and tangible book, with a 4.3% dividend yield, you’d think the stock would be a no-brainer, but the stock has been a perennial underperformer since the 2008 Financial Crisis, thanks to the dilution Citi underwent to boost capital. My recollection is that “fully diluted shares outstanding” increased by a multiple of 3x, which was crushing for the name. Also, unlike other financials, C’s 2022 EPS are expected to decline 30%, and then decline again in 2023 by 4%, given the current consensus.

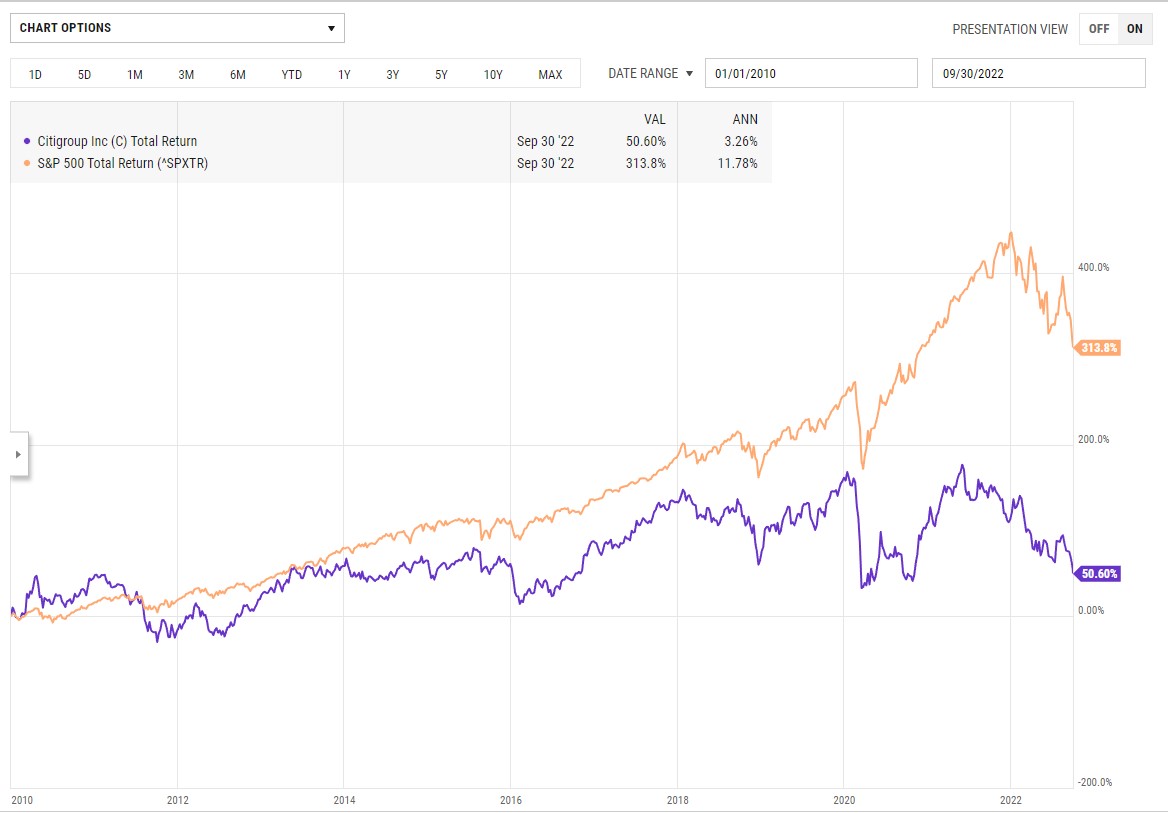

Here’s a 12 year performance chart of C versus the SP 500 since 1/1/2010:

Since 1/1/2010, C has underperformed the SP 500 by over 800 bp’s a year.

From a valuation metric issue, Citi generates returns-on-equity of high-single-digits, versus JP Morgan’s mid to higher teens ROE print.

Like Morgan Stanley, and like JP Morgan, Citi and Jane Fraser want to grow the wealth management business in the next 5 – 10 years.

It’s purely a guess since I’m revisiting the fundamental story, Jane will likely have to reduce overhead and pulls costs out of the business as she re-focuses on the long-term asset management business.

EPS and revenue estimate trends:

While down from the 12/31/21 EPS estimate, the calendar 2022 EPS estimate has risen since the summer. However if you look at 2023, Citi is expected to see EPS decline again in 2023 versus the high EPS print in 2021 of $10.14 per share.

Note how revenue revision trends are stable-to-higher. That’s a plus.

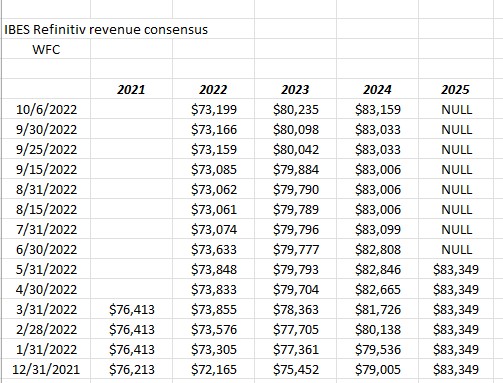

Wells Fargo (WFC):

Wells Fargo also reports their Q3 ’22 financial results next Friday, October 14, 2022. The stock hasn’t been owned by clients for several years when the account scandal broke. The stock was sold in the mid to low $40’s at the time and there is little interest repurchasing the shares. However readers seemed to be interested in the stock, given the multitude of talking heads that bring up the stock in the financial media, so here’s a quick look at the EPS and revenue estimate trends:

The first take on the EPS and revenue estimate trend(s) is that the decline or erosion in EPS isn’t too bad despite the drop in the mortgage banking business in 2022 while revenue estimates have been fairly stable through all of 2022.

That’s a positive for the stock (or should be) coming into the Q3 ’22 earnings report.

Summary / conclusion: Looking at the charts, only JPM has come close to it’s June ’22 low (in fact JPM has made a new low since the $110 – $112 print in mid-June ’22) in the subsequent months since the SP 500 put in a low in mid-June ’22 of 3,636, while both Morgan Stanley and Wells Fargo have remained about those mid-year lows in terms of their stock price action. Looking at my own internal fair value calculation as well as Morningstar’s estimate, all three stocks are trading at a 25% discount to that fair value estimate. JP Morgan is one of clients largest positions currently and remains a top 10 position while no positions are owned in Morgan Stanley or Wells Fargo.

JP Morgan still resembles the type of money-center bank that was prevalent in the 1990’s with both corporate and capital market operations and attracted regulator attention post-2008 due to revenue volatility and financial institution size and importance (SIFI). Morgan Stanley’s asset and wealth management operation is now almost 50% of the business by revenue and pre-tax income thus MS should be inherently more stable moving forward, while JPM’s asset and wealth management business is 14% and 12% of total net revenue and net income and probably needs to grow as a percentage of the business to help reduce EPS and revenue volatility.

Citi, which is by far the cheapest stock of the above – trading at a 40% – 50% discount to book and tangible book values, and will remain a work-in-progress, and may take some time.

To conclude, whether the stocks are buyable today and whether readers want to sit with them until capital markets start to perform better, probably is a significant bet on a) how bad of a recession we do see, the recession everyone is forecasting, or b) whether we have a recession at all. Prior to all of the above earnings reports next Friday, we will see September’s inflation data, both CPI and PPI, not to mention Friday morning, October 7th’s, September payroll report.

Personally, I think there is more reward than risk within the financial sector today (depending on the stock you’re looking at) but the economy and capital market conditions can change rapidly. The regulation lockdown that started in 2008 – 2009 and continued throughout the Obama Administration, was long overdue but there is also “we’re fighting the last war” aspect to it in terms of the stress tests. It seems highly unlikely the US sees another recession like 2008 for a long, long, time.

All EPS and revenue data is sourced from IBES data by Refinitiv, and the reporting dates are sourced from Briefing.com. Briefing.com is noting that Schwab (SCHW) is expected to report Q3 ’22 financial results on Monday, October 17th, while Goldman Sachs (GS) will report that week as well. Earnings preview of both Schwab and Goldman will follow on this blog.

All opinions are my own so take with a grain of salt. Past performance is no guarantee of future results and conditions can change for these stocks and yet the opinion won’t necessarily be updated. Markets change rapidly both positively and negatively. Unless the inflation data is still too hot next week, I like the double-bottom in the SP 500 at 3,636 and like financials here too. The sector is in much better shape than it was in the late 1990’s and then again in 2008.

Thanks for reading.