There was a slight sequential improvement in the forward 4-quarter estimate (FFQE) this week, but the 2023 and 2024 calendar year EPS for the SP 500 continue to be revised lower.

The data really doesn’t give investors confidence that SP 500 earnings will cure the stock market’s ills, but it’s not yet a disaster. The fact is the SP 500 earnings data is more “coincident” than leading or lagging, at least looking through the aggregate earnings data.

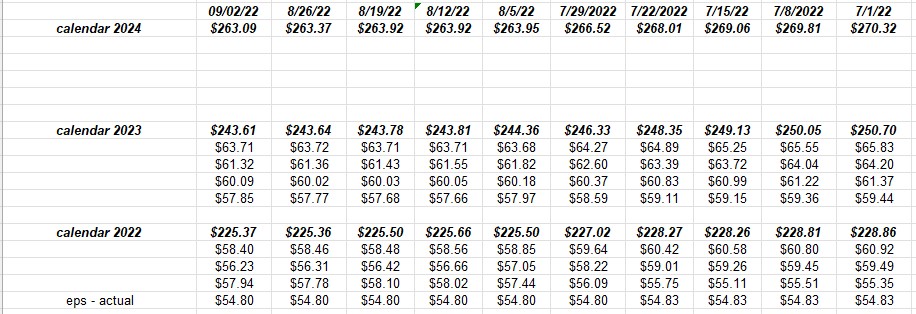

SP 500 data:

- The forward 4-quarter estimate rose two cents this past week to $232.57 from last week’s $232.55 and if there is anything notable about this data point, it’s that it is the first sequential increase in the FFQE since the week of July 1.

- The SP 500 PE ratio ended the week at 16.9x;

- The SP 500 earnings yield jumped to 5.93% this week from last week’s 5.73%. Anything above 6% since gets interesting, and 7% was the SP 500 earnings yield during Christmas week, 2018;

These calendar year and quarterly bottom-up SP 500 EPS estimates indicate that 2022 – 2024 full-year EPS estimates peaked this Spring ’22.

- 2024 peaked the first week of April at $276 and change and has declined to $263 today;

- 2023 peaked numerous times from late April ’22 to May ’22 at $251 and change and has been revised lower from there to $243.61 today;

- 2022 peaked between $229 and $230 in mid-June ’22 and has declined to it’s current print of $225.37;

- The Q3 ’22 bottom-up quarterly estimate has been revised lower by 5% to $56.23 today, from it’s peak near $59 as pf late July ’22;

- The Q4 ’22 bottom-up quarterly estimate has been revised lower also by 5% from it’s peak near $61 per share to today’s $58.40;

The data is right above for you to look at, and at least so far anyway this isn’t that extreme.

However, one high profile earnings warning from an Apple or a Microsoft or any of the mega-cap 5 and it could get grim in a hurry.

Technology is worrisome:

![]()

The above table shows the “expected” full-year 2022 SP EPS growth rates (y.y) by sector.

Highlighted in dark border is the Tech sector’s expected growth rate for 2022 since April 1 ’22.

Technology’s expected growth rate has been cut by 2/3rd’s since April 1 ’22, probably pretty consistent with the action in semiconductors, and Intel in particular. Intel still has a pretty sizable market cap weighting in the SP 500 (63rd if I counted right) but Nvidia is 11th even after their miss, with a 1.13% weight. Bespoke has long written that watch semi’s for a tell for technology and often for the market in general, and the news of late isn’t good.

The nice thing is – in terms of the Tech sector – was that their troubles started in Q4 ’21 with the ad spending slowdown. Q2 ’22 was a very tough quarter for comp’s for technology as a whole, but tech comp’s get easier as we get into year-end.

Summary / conclusion: Given the stock market action today, Friday, September 2nd, 2022, there is little reason to do anything in the stock market until we get some kind of technical improvement in the action.

The August ’22 jobs report was almost picture-perfect today with the unemployment rising to 3.7%, the average hourly earnings coming in better-than-expected, the actual “new new jobs added” to US economy was almost exactly inline with what was expected – around 300,000 – and we even saw a big negative revision to June’s numbers, which made the aggregate number look even lighter.

The stock market is clearly saying “we will wait to hear from Jay Powell” before we get too excited about expecting higher future stock market returns.

The CPI and PPI don’t come out until a week from next Monday, September 5th, 2002, and Tuesday, so there will be another 5 days to wait before the data confirms the numbers are actually “disinflating”. The market signals are indicating inflation is declining rapidly.

Here’s what’s worrisome: the stock and bond market action from January to May ’22 was all about higher inflation and waiting for it to break, since May – June and the mid-June ’22 lows, as market-based inflation data has fallen sharply, the Fed seems to have ever-so-slightly shifted it’s focus to labor and wages, and now today – albeit the average hourly earnings is just one data point – but if the labor and wage data softens and stocks STILL do not get a footing, the only conclusion is that the US economy is headed for a weaker recession than the pundits expect.

That’s my own calculus, so take it all with a hefty wheelbarrow of salt. Jay Powell changed his mind quickly in the last two weeks of 2108, and the stock market sniffed it out and rallied sharply after Christmas and all through 2019. But again, there wasn’t the inflation issue there is today.

There isn’t really 1 company that will report earnings next week that is of interest, but the next week, September 12th to 16th, investors will hear from both Oracle and Adobe, two software companies and software hasn’t fared too well since 2021 ended.

Long weekends like memorial and Labor Day usually make for good writing. More to come (hopefully) over the weekend.

Remember all of this is one opinion, it can change quickly, it can be very wrong, so take it as such. Past performance is no guarantee of future results.

Thanks for reading.