The rally quote was from CNBC’s nightly summary.

July ’22 index returns:

- Dow Jones: +6%

- SP 500: +9.1%

- Nasdaq: +12.4%

Source: CNBC Evening Brief (This blog is being written on Friday night, thus returns will be verified against Ychart and Morningstar returns, which don’t come out until the weekend.)

The sharp estimate cuts are from the weekly work done here on the blog, with data courtesy of IBES data by Refinitiv.

SP 500 data:

- The forward 4-quarter estimate fell to $236.83 from last weeks $239.37. That 1.06% sequential decline is a big hit to the FFQE, the largest since COVID struck.

- The PE ratio rose this week to 17.4x vs last weeks 16.5x on the 4% jump in the SP 500 combined with the drop in the forward estimate;

- The SP 500 earnings yield fell to 5.73% from last week’s 6.04%;

- The bottom-up Q2 ’22 estimate rose this past week to $56.09 from last weeks $55.75, although analyst’s are cutting forward bottom-up quarterly estimates;

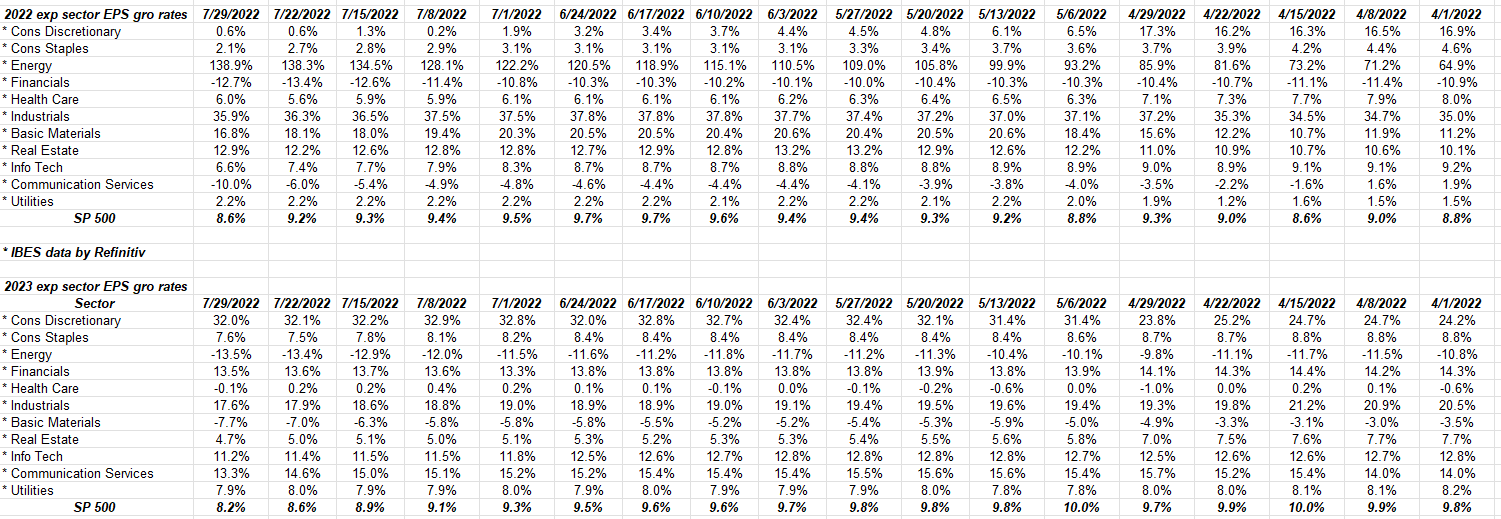

Expected sector EPS growth rates for 2022 and 2023:

These tables are from IBES and updated weekly: note how 2023 SP 500 EPs estimate (as a whole) are being cut a little more sharply than 2022.

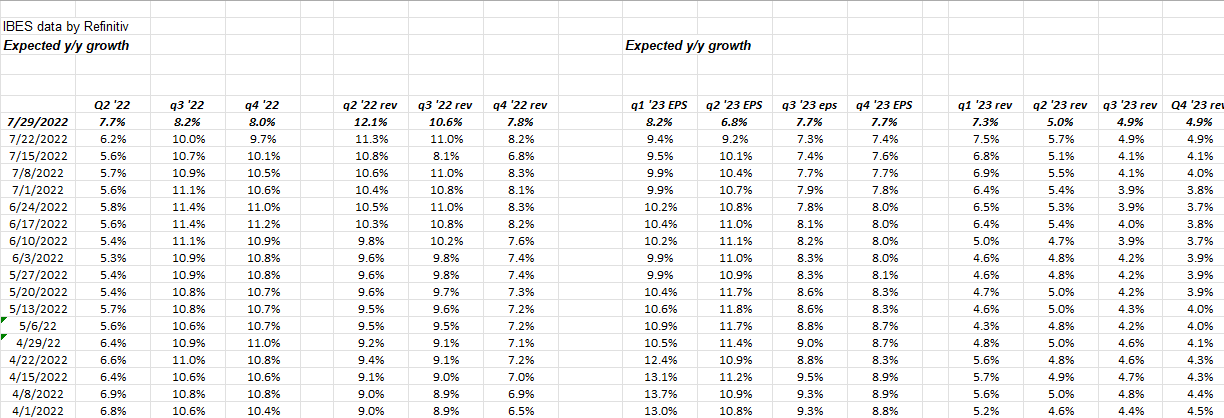

Quarterly EPS and revenue growth estimates for forward quarters:

Note from the above tables how Q2 ’22 EPS and revenue growth for the SP 500 is improving, BUT the forward estimated growth rates for both EPS and revenue growth were reduced this week. Pretty harshly too.

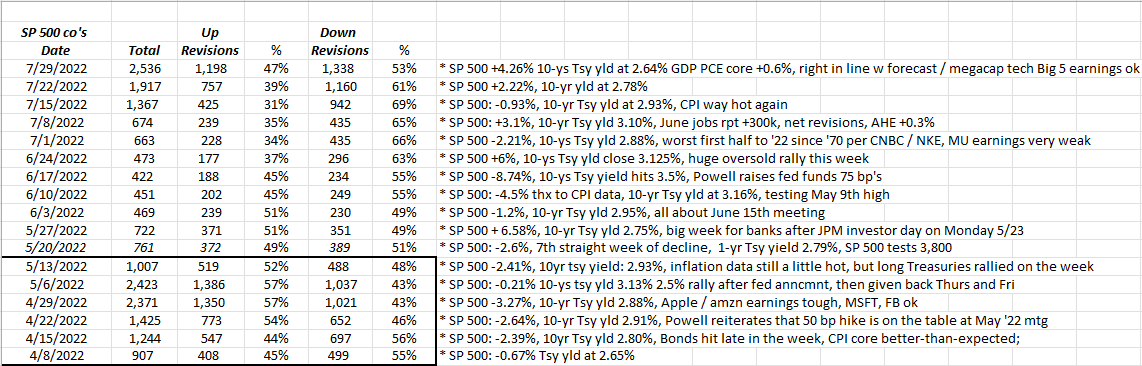

SP 500 estimate revisions as a whole: Not a positive

Refinitiv reports this data weekly. The bordered area shows Q1 ’22’s earnings revisions – positive vs negative. You can see how when earnings season started in mid-April ’22, the “positive” revisions outnumbered negative revisions each week.

Readers can also how Q2 ’22 SP 500 EPS negative revisions outnumber the positive revisions 2 to 1 since July 15th, ’22.

While the positive revisions have improved each week in the last 3 weeks, they are still below 50%.

It matters. Much of this could be the US dollar too. It’s having a big impact this quarter on revenue, which ultimately impacts EPS.

Summary / conclusion: The sentiment still seems tilted quite favorably to the bears, but the monthly rally across the major stock indices (and bond indices) for that matter, has been impressive. In the 1994 tightening cycle by the Fed, the SP 500 was trading around 445, and the index bottomed in April and December of ’94 and then took off in 1995 returning 35% (approximately). The 2000’s were a tough decade to use as an allegory because of the two 50% bear markets. In 2018, during Powell’s tightening cycle, I thought the SP 500 fell 20% through Christmas in the 4th quarter, bottoming the day after Christmas and then rallied 7% to end the month, quarter and year and that was the extent of the correction because Powell went from tightening, to neutral, to accommodative, soon after the first of the year.

Regular readers of the blog know that the two SP 500 levels being watched are (or were) 3,810 which was the May 24th low, of which the SP 500 seems safely above again, and the mid-March ’22 low for the SP 500 at 4,157.87, which was right around the March ’22 initial fed funds rate hike.

Personally, I’ll get more bullish on stocks within a 60% / 40% or 50% / 50% asset allocated portfolio if the SP 500 trades above 4,157 and then stays there, which would be a substantial recovery off the June ’22 low of 3,636.87. Remember the 2022 high for the SP 500 was 4,818, hit on the first trading day of the year, and then it was straight south from there.

What I really like is the improvement in high yield credit spreads in the last 6 weeks, and what I’d really like to see is the US dollar continue to fall, after its peak on or around July 14, 2022.

The sharp estimate cuts to forward numbers is not a positive though, that’s for sure.

Ultimately, it really depends on how deep you think the recession will be, as we debate the definition of recession in the mainstream media. Personally, there is no question the US economy has slowed, but it’s probably bumping along at neutral, give or take 1% as a margin or error. Jay Powell shifted quickly from tightening to easing in late 2018, early 2019, but he didn’t have inflation to worry about back then. Will he do the same again ? If CPI inflation comes down quickly I’d say yes, given it’s an election year, but most pundits are saying CPI inflation might be stickier than we think. Yesterday’s core PCE came in as expected at 0.6% (per Briefing.com data) but the fact that it didn’t come in better-than-expected was a disappointment.

My own opinion is Jay Powell would likely risk a deeper recession to try and keep inflation at bay, and maybe the sell-side analysts are starting to factor that into the data.

The July jobs report due out August 5th is looking for 250k – 275k net new jobs created, which is well below the post-Covid run rate of over 400,000.

It will truly be interesting how Jay Powell handles a weaker-than-expected jobs report with inflation numbers that might not come down.

However in no way do I think that we are facing a 2008-type scenario or bear market, but we are still in an environment where the range of probabilistic outcomes is still pretty wide and varied, even with the positive price action in stocks, and bonds. Inflation, recession, SP 500 earnings, the dollar, credit spreads, does Jay Powell let the economic data get worse to keep inflation in the bottle, Europe, Putin, and on it goes.

Remember, readers don’t have to pick tops and bottoms, even though it’s a fascination with Wall Street and the mainstream financial media. It’s dangerous in fact.

To complicate issues even further, the calendar is entering one of it’s worst seasonal periods of the year. August, September and October are typically tough trading.

Take all this with substantial skepticism. I have no idea what will happen over the next few months. Playing defense with accounts is still the strategy, but that could change quickly. There are both many positives and negatives to the landscape right now. Don’t be a hero.

More to come this weekend.

Thanks for reading.