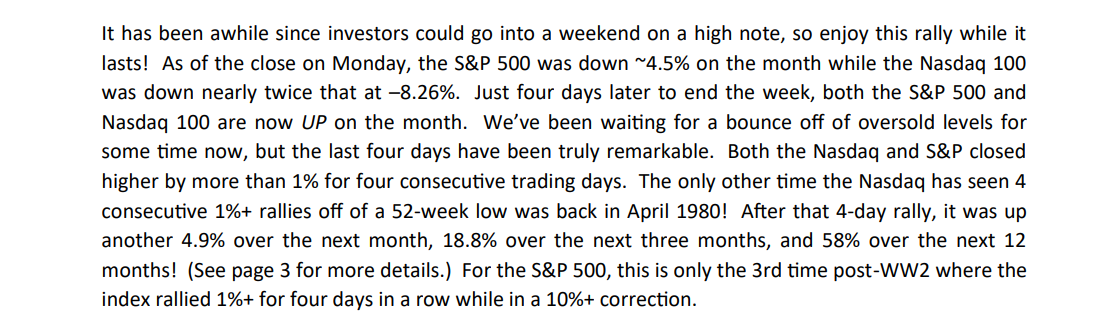

The SP 500 jumped 6% this week, in a week many of the pundits are calling a record series of daily rallies. Bespoke sums it up in the first paragraph of their weekly Bespoke Report:

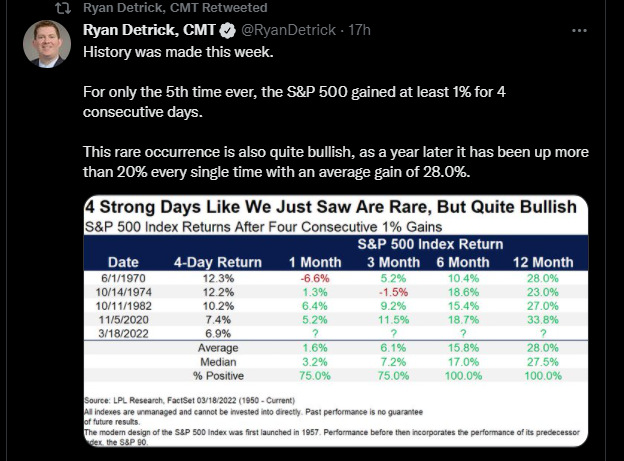

Ryan Detrick of LPL Financial lays the same data out in a table / chart format:

(Enlarge the file by clicking on the insert.)

While the pundits and the financial news can attribute the SP 500’s 6% gain this past week to numerous factors, the fact is SP 500 continue to improve.

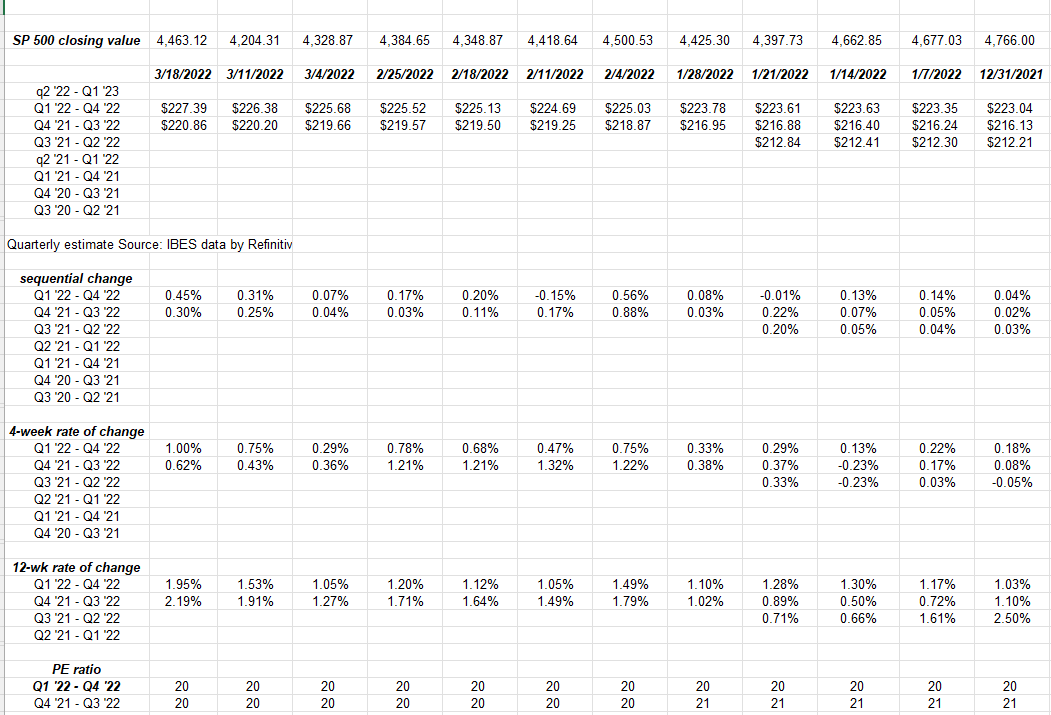

SP 500 earnings data: (Source data is IBES data by Refinitiv):

- The forward 4-quarter estimate ticked higher this past week to $227.41 from last week’s $226.46 and 12/31/21’s $216.14;

- The PE ratio on the forward estimate rose to 19.6x from last week’s 18.5x;

- The SP 500 earnings yield fell to 5.1% from last week’s 5.39% (which was an earnings yield peak not seen in the last few years);

Here’s the various metrics tracked on the SP 500 earnings spreadsheet:

Rate-of-change for various time frames:

Since 12/31/21, the various rates-of-change are showing a slight acceleration in the forward estimates, particularly over the last 4 weeks.

That’s a positive.

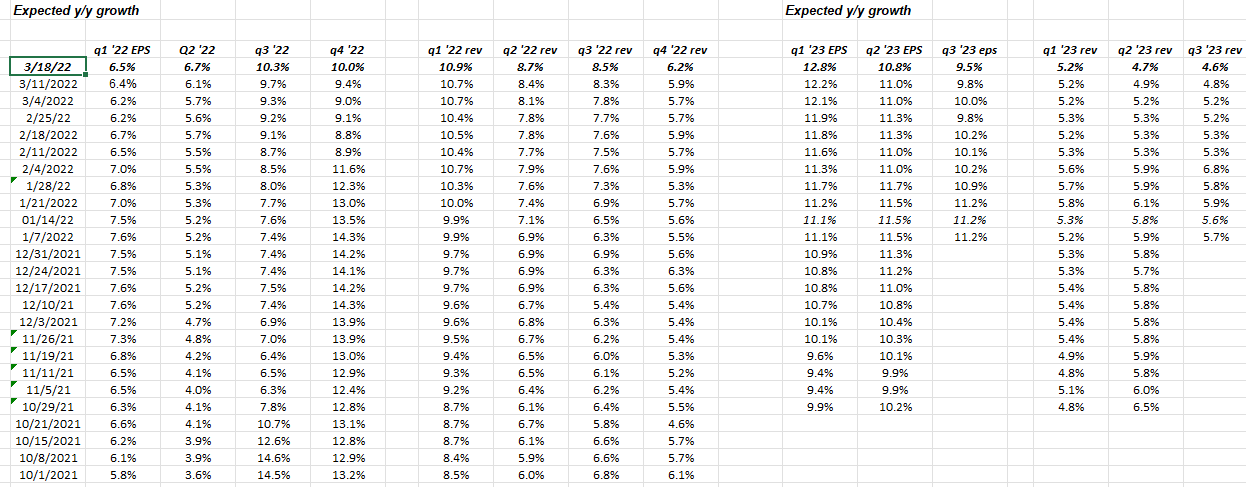

This table – long one of my favorites – shows the week-to-week progression of expected SP 500 EPS and revenue growth rates for 2022, and for the first time, 2023.

This blog has been tracking expected 2023 EPS and revenue growth rates but readers are seeing them today for the first time.

Again, what’s interesting to me is that “expected” quarterly revenue growth for the SP 500 for 2022 is expected to decline gradually over the next four quarters while year-over-year EPS growth is expected to improve gradually over the next 4 quarters.

This may indicate what first showed up the last 5 – 7 trading days and that commodity inflation and thus margin pressure will begin to subside for the SP 500.

The growth rates by quarter for the SP 500 are in a “return-to-normal” after the pandemic-influenced 2020 and 2021.

Summary / conclusion: The trends in SP 500 EPS and revisions have changed little so far this year, so the rally of this week, could simply be confirming that all is solid on the SP 500 earnings front. Last week, this was covered in detail in the weekly update.

It’s hard to get very bullish with the Fed planning on numerous rate hikes this year. Unless crude oil falls back to $70 – $75 and the rest of the commodity complex starts to give up these 12-monh gains, it’s hard to think that the Fed won’t sway from it’s already-predetermined path.

The data with this week’s rally (i.e. 4 consecutive gains in the SP 500 of 1% or more) is very hard to ignore but the Fed looms large and I can’t help but think that more rate hikes and QT (quantitative tightening) will pull the rug out from under the bulls in a hurry.

If commodity prices do collapse, I think that gives the Fed and Powell some breathing room. The price of gas is a big psychological hurdle for the consumer.

None of this is a forecast. Take everything you read and hear with a considerable grain of salt. As readers saw this week, the capital markets can change very quickly. Now even the prospect for “nukes” in Ukraine is appearing more and more in mainstream media. (Please excuse the typo’s and issues with the tables and EPS info. All errors and mistakes are likely mine and not the data source.)

This blog will have some posts on sector-related earnings issues this week.

Thanks for reading.