Flow out to the East Coast Friday for dinner with a new client, and I remember thinking “Everyone’s nervous, and everything seems overvalued” and then the following thought was, “Well, should that make me bullish as a contrarian sentiment gauge ?”

It’s a weird business, but the fact is so many people seem to be worried about a correction, and for good reason, and yet right there is the proverbial “wall of worry”.

An email went out to clients last week, looking at uncorrelated assets that have lagged badly for the last 12 – 15 years:

- Gold: the GLD has still not taken out it’s Sept, 2011, $185.85 high. It’s 10-year return is negative, or maybe by now, just barely positive;

- Emerging markets ex-China: It’s tough to own anything Chinese, but even the standard EM ETF or fund from June 30 ’07 has returned just 2% – 3% annually;

- Europe / European ETF’s: thinking mainly about the EFA ETF.

No doubt there are others. Let me know your favorite “worst performers since 2009 – 2010 or before that.

—————

With Walmart (WMT) and Cisco (CSCO) reporting this week, it’s the “unofficial” end of 3rd quarter ’21 reporting season, and the 3rd quarter hasn’t been that bad, despite the fears coming into the 3rd quarter earnings releases from several higher-profile commentators.

That being said, investor now face “tougher comps” in Q4 ’21 and 2022, so it’s likely readers and investors are going to see an emerging bearish tone to forward earnings.

And it’s not wrong, but it’s really more of a “return-to-normal” for annual SP 500 earnings and revenue growth, more than anything else.

What is worrisome today (and as a portfolio manager, there is ALWAYS something that is worrisome) is that more retail clients and even many institutional investors are worried about the stock market, while the real problem – if and when it does arise – may lay with the bond market(s).

SP 500 metrics:

- The forward 4-quarter estimate fell this week to $214.77 from last week’s $214.95. The forward estimate is returning to a more normal pattern where it jumps sharply higher at the start of a new quarter and then starts to slide gradually into the end of the quarter but remains above the final week print of the prior quarter. For example, the forward 4-quarter estimate for the last full week of September ’21 was $206.60 or roughly $206 – $207. The estimate jumped to $213.17 the first full week of October ’21 as we added a new quarter and drop off the old quarter for the “forward 4-quarter” estimate. As long as the forward 4-quarter estimate remains above $206 – $207 by the end of December ’21, the pattern is consistent with “normal” (i.e. non-pandemic) earnings patterns. This is actually the first sign that SP 500 earnings forecasts are beginning to return to non-pandemic patterns. Ed Yardeni has written about this pattern as has Jeff Miller (A Dash of Insight) in the earlier part of the 2010 decade.

- The PE ratio this week was 21.8x exactly the same as last week;

- The SP 500 earnings yield ticked up to 4.59% from last week’s 4.58%.

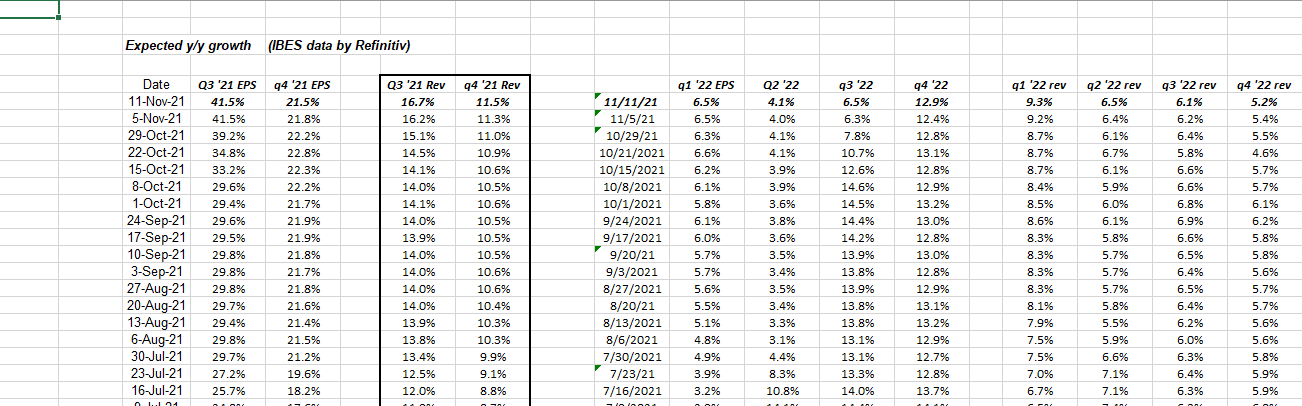

Looking ahead by quarter:

Data source: IBES data from Refinitiv

I love this table but it took me 10 years to start compiling the data this way, from Refinitiv’s Earnings Scorecard report, but readers can see the tone for Q4 ’21 or the bias to overall SP 500 EPS and revenue growth for the final quarter of the year is still positive.

With Q4 ’21 earnings releases, we will get guidance for 2022 and that’s will really move the needle for ’22 calendar year in terms of revisions.

Summary / conclusion:

This blog logs or records a lot of data every weekend, and this week – with the CPI data – the 2-year Treasury yield jumped to 53 bp’s or double the 10/1/21 closing yield on the 2-year Treasury of 27 bp’s.

Most clients and investors are worried about the stock market today, but I worry far more about the bond market(s). Clients haven’t owned any direct high-grade bond fund exposure for 18 months, with investment grade credit spreads where they are and even high-yield credit spreads don’t offer all that much absolute yield.

The fact is “everything’s overvalued” or it sure seems like it.

If there is a problem in the bond market there is a problem with everything i.e. the stock market, bond market, housing, anything financed, but all I’ve done today is add to the crescendo of negative voices in the market. It seems like pessimism is rampant and no one wants to be bullish (except maybe Tom Lee and he’s had it right all along).

Just one opinion – take it all with great skepticism.

Thanks for reading.