On March 20th, 2020, the HYG or high-yield ETF was down 18.11% YTD, after the Covid-19 issue struck and the stock and credit markets started becoming unglued. Today, the HYG is +6% YTD, and the SP 500’s total return as of Friday, December 4th was 16.6%.

An 18% drop for the HYG is a steep correction and during that week in March ’20 it could have been worse. High-yield as an asset class bottomed with a 25% yield in late 2008, early 2009.

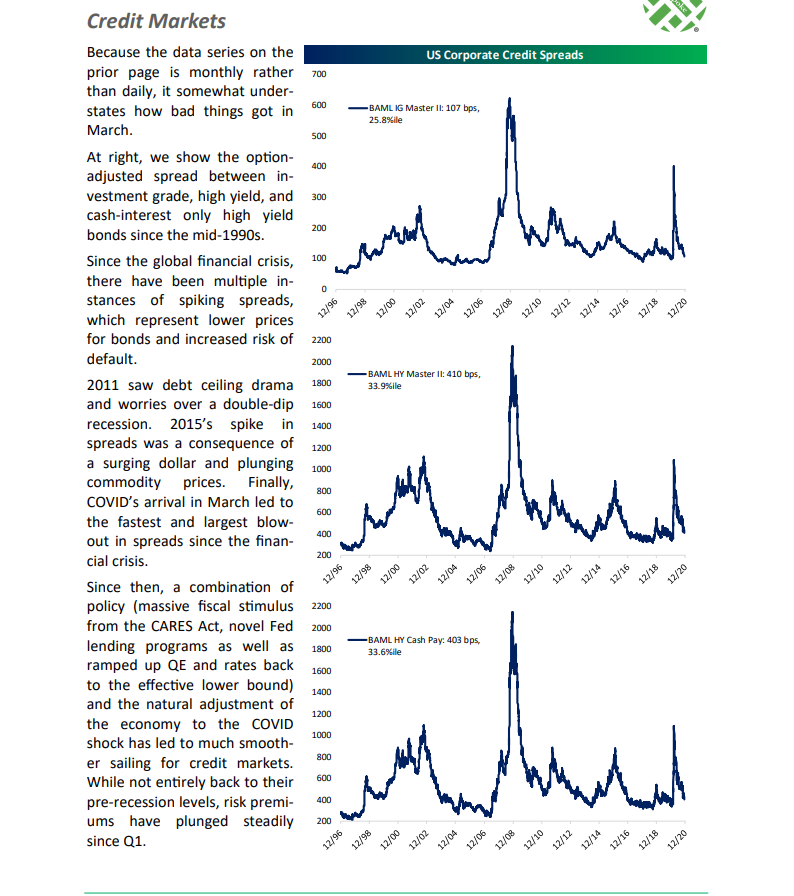

This section of Bespoke’s Credit outlook for 2021 published this weekend, shows how high-yield credit has recovered since the March – early April ’20 high yields. The fascinating thing about this is that the Fed’s liquidity programs were – for the most part – untouched since March, and the recovery in the credit markets was all on its own. The Fed did buy a little HYG in July per some reports, but for the most part many of the liquidity programs put in place were not needed.

Like the big brother behind you on the playground, all the Fed needed to do was announce the presence of the liquidity facilities and – voila – spreads started to come back in, undoubtedly helped by the fiscal stimulus too.

Housing is another positive contributor. Several clients are in the real estate business either here in Chicago or Denver and many seem to be having a record year, particularly if their specialty is residential.

The bottom 2 charts of this larger Bespoke chart from this weekend shows the extremely low single-family housing inventories and the rapid appreciation in the median “existing home price” seasonally adjusted.

For most of my clients, there largest asset is usually their single-family home, particularly if they are under the age of 40. For older clients who have done more saving in the last 10 – 20 years, their portfolio and their 401k’s can be their largest asset.

Summary / conclusion: During the weekly SP 500 earnings update done this week, and with the Covid-19 lockdowns, and the election headlines, the forward SP 500 EPS estimates have done nothing but consistently trek higher the last 6 – 7 months, and I do think corporate credit spreads and housing are a BIG part of that improvement.

All of client’s investment-grade and mortgage exposure has been sold. There isn’t much value in the high-grade corporate credit market today (in my opinion) or mortgages, so we are looking elsewhere. Even Emerging market bonds have come in substantially.

While junk bond credit spreads are at or near absolute low yields, with a 95 basis point 10-year Treasury, credit spreads have not yet the maximum “tights” from 2006 as the first Bespoke chart demonstrates.

There is still room in high-yield for relative credit spread improvement, particularly with the improvement in the Energy sector.

Thanks for reading.