First, the bounce in the marijuana stocks are probably telling us that Joe Biden has taken the presumed lead of late in terms of the favorite to win the 2020 Presidential election.

That sector’s been a house of pain after the stocks got a bounce in 2019 after the House passed the SAFE Banking Act, however the major snafu was that Mitch McConnell sat on the SAFE Banking bill, and never passed it in the Senate, thus all the stocks in the sector have gotten crushed for most of 2020.

The stocks trade on the pink sheets hence most have little institutional ownership, but I expect that could change in a hurry with a Democratic Congress and President.

On August 3rd, Ryan Detrick of LPL Financial published his “stock market election indictor” noting that how the stock market performed for the 90 days prior to the Presidential election was a good leading indicator of whether the incumbent or the challenged would prevail.

Since August 3rd, through 10/21/20, the SP 500 is up 4.9%, thus signalling President Trump likely being re-elected.

The dollas has also been weaker into the election over the same period, which is also supportive of the incumbent retaining the office.

Finally, the improvement in the 10-year Treasury yield to +0.80 bp’s as of this morning, gradually making higher yield closes through October, could be indicative of a pro-growth, low-tax result on November 3rd.

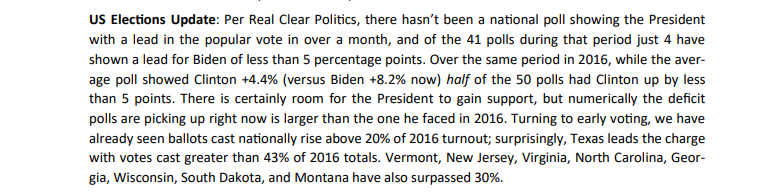

One of this blog’s favorite research sources is Bespoke Research, and Paul Hickey and Bespoke have definitely been leaning Biden’s direction in the last few weeks. I’ve been reading Paul Hickey’s Bespoke for years and never felt that their political commentary was anything but completely objective, so when they published this little blurb Monday morning, October 18th, with the Bespoke Morning Lineup, I took notice:

Summary / conclusion: With both high regard for Ryan Detrick and Bespoke’s work, I thought regular readers and clients would want an update the last two weeks of the campaign.

The final debate is tonight, and whatever happens the pundits will be spinning full time.

As someone who watched in real-time in late 2017 and 2018 as the TC&JA cut the corporate income tax rate from the high to the law 20% range and saw the commensurate increase in the SP 500 actual EPS move higher from $132 (final) in 2017 to the tax-aided $162.13 final for 2018, or a 25% y/y increase, it was unsettling to listen to Senator Kamala Harris in the VP debate state unequivocally in that the corporate income tax rate cut would be repealed, and the income and capital gains tax rates increased under a Biden / Harris ticket.

As was stated last week on the weekend update, just a reversion back to the high 20’s tax rate for corporate income taxes would likely cost at least $15 – $20 in the expected 2021 SP 500 EPS current estimate of $165.83, and that doesn’t include any changes to individual or capital gains tax rates.

Although Factset retracted the statement after publishing it, Factset was telling readers in late 2018, early 2019 that the “organic” growth rate for 2018 SP 500 EPS was 13% – 15% (excluding the TC&JA), so we might see something similar on the downside if there is a higher corporate income tax rate.

A Biden Blue Wave and a sweep in Congress with enough Blue votes to change the 2017 TCJA back to its original form, would – in my opinion – likely mean (at least) a 10% – 15% correction for the SP 500 in late 2020, maybe early 2021.

Stock prices will adjust to higher tax rates. That’s a certainty. That’s the big risk for investors, although depending on a second stimulus, and what else happens, the correction could be just that and nothing more.

Take everything you read here with great skepticism and think for yourself and do your own homework,.

The interesting action today is what’s happening in the Treasury market.