(Thanks to David Aurelio and Tajinder Dhillon of Refinitiv IBES for providing above data.)

Here is what struck me about the above data:

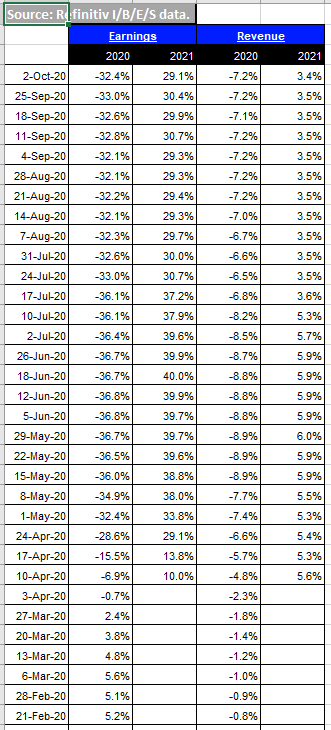

1.) The expected 2020 EPS growth for the Financial sector improved right around the time in July ’20 when bank earnings and other financial earnings began to get reported. The expected 2020 EPS growth rate improved from -36% to -32% by the end of July ’20 but has remained stagnant since;

2.) 2020’s expected revenue decline improved slightly as well from -8% to -7% and also has remained stable for the rest of August and September ’20;

3.) 2021 expected EPS growth was offsetting the expected 2020 decline up until July 24th and then from that week forward, the expected 2020 decline in EPS was greater than the expected growth rate of 2021 EPS for the remainder of August and September ’20;

4.) Same with expected revenue growth: 2021’s expected revenue growth was greater than the 2020 percentage decline until April 10th, and then 2020’s expected percentage decline eclipsed 2021’s expected revenue growth and the difference has grown since.

The top Financial sector names in the SP 500 (ranked by market cap):

- Berkshire Hathaway (BRK.A / BRK.B)

- Visa / Mastercard (V/MA)

- JP Morgan (JPM)

- Bank of America (BAC)

- Wells Fargo (WFC)

- Goldman Sachs / Morgan Stanley (GS/MS)

Whether Visa / Mastercard are “financial” stocks is probably worthy of debate, since their core operations are tied to the expansion and contraction of credit usage, primarily in the United States, but some consider them technology (i.e payment networks) and even might even be closer to Fintech.

What’s the point ?

Anyone reading this blog is sophisticated enough to know that Financial sector earnings, particularly bank earnings are being impacted by three primary issues:

1.) Expected credit losses at the consumer level, which will likely get worse in the 3rd quarter;

2.) Net interest margin (NIM) compression, which has probably run its course for the most part unless we get negative interest rates, but the steeper Treasury yield curve from last week and today will help NIM, but only if it’s sustained;

3.) The Fed’s prohibition on share buybacks to force banks and other Financials to retain capital (an order of the Fed which was reiterated late last week). In this link from Sunday’s blog post, the third table is JP Morgan’s Guide to the Market page 9, showing the various “shareholder yields” of all the major SP 500 sectors and as readers can see, the Financial sector has the highest capital return of all 11 sectors of the SP 500.

The banks have an excess of capital today, pending the addition to credit losses expected in the 3rd quarter earning’s releases, but at some point the Fed will likely allow the return of capital once again via share buybacks. The big question is “when will that happen ?” and what will be the impact on EPS ? We’ll know more after the 3rd quarter numbers are seen.

At some point I’d like to see 2021 Financial sector EPS and revenue estimates start to turn higher. 2021 Financial sector EPS needs to recover the 2020 decline.

Summary / conclusion: The banks and brokers begin reporting next week – the week starting October 12th, 2020 – and the focus on the big banks will – in my opinion – be on credit losses.

Here is a link from last April 16th, 2020 where this blog recapped the estimated full-year 2020 loan loss provisions (LLP) as put forth by some sell-side firms.

JP Morgan was expecting a full-year 2020 LLP of $40 billion and Bank of America was expecting a full-year LLP of $30 billion.

For JP Morgan, their Q1 ’20 LLP was $8.20 billion and their Q2 ’20 LLP was $10.5 billion for a total of $18.7 billion, after 2 quarters, less than half the expected full-year $40 billion LLP.

For Bank of America (BAC), the Q1 ’20 LLP was $4.8 billion while Q2 ’20 was $5.1 billion, for a $9.9 billion LLP versus the full-year 2020 estimate in April of $30 billion.

JP Morgan has used almost half their expected LLP while Bank of America has used just 1/3rd for the first 6 months of the year.

You can see why Q3 ’20 loan loss provisions are carrying such weight into the earnings releases.

Summary / conclusion: The one aspect that is tough to reconcile with the expecetd credit losses is the strength in consumer spending, particularly in big-ticket items like cars, boats, RV’s, etc. There seems to be a substantial portion of the US population that is liquid and ready and willing to take on credit.

Here is a note from Ed Yardeni from his Sunday night newsletter on expected Q3 ’20 GDP – now expected around 34% – and much of that consumer spending driven:

“In our May 21 Morning Briefing, we predicted that “US consumers will open their wallets and spend once some semblance of normalcy returns.” So far, so good. As the lockdown restrictions were gradually lifted during May, consumers rushed to spend lots of the cash they had saved up during the lockdown.

Housing-related spending has been especially strong, as consumers have decided it’s time to remodel their cabins if they are going to spend more time working, learning, and entertaining at home. They’ve also rushed to buy more new and existing cabins in suburban and rural areas in a broad-based wave of de-urbanization triggered by the pandemic. In addition, the pandemic may have convinced many Millennials (who are currently 24 to 39 years old) that now is the time to buy a house rather than to rent an apartment. The Fed is contributing to the resulting housing-related boom by keeping mortgage rates at record-low levels.

All these developments were confirmed last Thursday, when the Bureau of Economic Analysis (BEA) released the August personal income report. Friday’s employment report for September released by the Bureau of Labor Statistics (BLS) suggests that consumers continued to gain purchasing power from their participation in the labor market—i.e., working—which should more than offset the decline in purchasing power provided by the government with pandemic-support benefits.

If Washington provides another round of such support anytime soon, that will unleash even more dopamine, adding to the economic “V is for Victory” victory over the pandemic’s economic impact. Consider the following:

(1) Consumer-led V-shaped recovery. The October 2 update of the Atlanta Fed’s GDPNow model showed that Q3’s real GDP is tracking at a record jump of 34.6% (at a seasonally adjusted annual rate, or saar) following the record 31.4% drop during Q2. That’s certainly a V-shaped recovery so far.

Leading the way up during Q3 is a 36.8% projected rebound in real consumer spending, following the 33.2% drop during Q2. Consumers contributed 24.0 percentage points to the freefall in real GDP during Q2, when lockdown restrictions held them back (Fig. 1). They are likely to contribute more to the Q3 upswing. By the way, spending on consumer services was hit hardest by the lockdown during Q2, as evidenced by the -22.0ppt contribution of this component to the drop in real GDP!

{kind=link}

In current dollars, personal consumption expenditures has rebounded 18.6% from April through August (Fig. 2). It is only 3.4% below its record high during January. Interestingly, consumer spending on goods is up 24.0% over this period to a new record high. Spending on services is up 16.1% since April but still 7.4% below its record high during February. During August, consumer spending totaled $14.4 trillion (saar) with services at $9.5 trillion and goods at $4.8 trillion.”

{kind=link}

That’s what i’m having a hard time reconciling: the consumer spending and the expected credit losses. How consumer credit losses come in relative to expectations in Q3 ’20 (and the expectation is that the losses will be larger) for the big banks will determine how the banks trade in the 4th quarter.

Thanks for reading and take all of this with measured skepticism.