So far, Q3 ’19 earnings are following the normal pattern.

One way to tell is to watch the “revisions” pattern for the SP 500 companies, week-by-week.

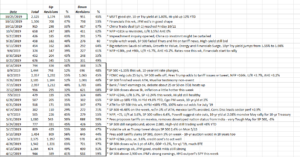

The attached spreadsheet shows that with the 3rd week of SP 500 earnings releases, the “upward revisions” have moved back above 50%, consistent with the pattern this year.

The 4th column is the percentage of positive revisions for SP 500 companies and the top line indicates that as of this week, the SP 500 revisions tipped to positive.

It’s a normal quarter so far.

The only other stat that stuck out this week is that the 2019 bottom-up SP 500 EPS estimate actually increased this week from last week’s $162.93 to $162.95. What’s unusual about that is that we usually see downward revisions into the end of the period. $0.02 doesn’t sound like much (and it is not) but I’m more interested in the change in trend than it’s magnitude right now.

SP 500 data (by the numbers): Source IBES by Refinitiv

- Fwd 4-qtr est: $173.95 vs last week’s $174.75

- TTM est: $162.96 vs last week’s $162.65

- PE ratio: 17x

- PEG ratio: 2.58x

- SP 500 earnings yield (fwd): 5.76%

- SP 500 earnings yld (TTM): 5.39%

- Y/y growth of fwd est: 6.74% vs last week’s 7.44%

(The data presentation is being revised again because of some confusion around the data. This blog has disclosed the growth rate of the “forward estimate” today vs the “forward estimate” 52 weeks prior which has narrowed to just 40 basis points as of this week. It has been distorted by last year’s “tax reform” and the 23% SP 500 earnings growth for 2018, so this blog is just showing the “forward estimate” divided by the TTM or “trailing-twelve-month” estimate so as not to confuse readers. The PEG data gets very distorted, which i’m concluding for the SP 500 anyway, is not a reliable valuation indicator. Comparing the forward estimate today vs 52-weeks prior is not going away. It will be covered in a separate post. My own opinion is that comparing the estimates gives readers an opportunity to exploit “PE expansion” or “PE contraction” for the SP 500.)

————–

Calendar-year SP 500 EPS estimates and actual:

- 2020 SP 500 EPS est: $180.44 (expected y/y growth of 11%)

- 2019 SP 500 EPS est: $162.95 (expected y/y growth of 1%)

- 2018 SP 500 EPS actual: $161.93 (actual y/y growth of 23%, ex tax reform per Factset, is 14%)

- 2017 SP 500 EPS actual: $132.00 (actual y/y growth of 12%)

If you are ever wondering why the SP 500 has an upward bias, even with the steady downward revisions in the forward estimates, the SP 500 has only had one year of negative SP 500 EPS growth in the last 10 years and that was 2015’s -1%, with 2019’s expected growth of 1% coming pretty close to breakeven point.

If we looked at SP 500 earnings growth like retail analysts use “2-year comp’s” when tracking retailers monthly sales data, the 2017- 2018 2-year growth comp was 13% (using 14% organic SP 500 growth in 2018), the 2018 – 2019 2-year comp is probably 7.5% – 8%, and the expected 2019 – 2020 growth comp could be 5% – 6% depending on how the 11% expected SP 500 earnings growth materializes next year.

Using the SP 500’s expected growth rate of 1% for 2019, the “average” annual SP 500 earnings growth rate from 2010 to 2019 has been 11%.

—————–

Summary / Conclusion: Next Wednesday, October 30, 2019 could be an explosive day with the FOMC expecting to make an announcement about monetary policy (93% probability of a fed funds rate cut to 1.50% – 1.75% per CME fed funds futures) and Apple and Facebook reporting. Of the top 10 SP 500 names Apple was the first to break out over it’s early October, 2018, $231 – $232 high. JP Morgan has followed. Surprisingly, Microsoft with it’s good quarter couldn’t break out to an all-time-high. This blog covered Microsoft’s earnings preview this week. Alphabet (GOOG/GOOGL) has been locked in a trading range, like Microsoft and facebook, and it reports Monday afternoon after the close. Let’s see if mega-cap Tech can regain that momentum.

Out with more this weekend.

Thanks for reading.