This morning’s Empire Report not withstanding, (the weakest since June, 2011 per Bespoke), while the market sentiment has firmly tilted to the bearish camp, “market breadth” is one reason to remain firmly rooted in the bullish camp.

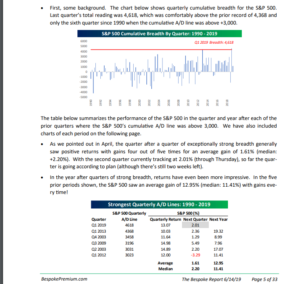

Here are two graphs from “The Bespoke Report” over the weekend:

Click to enhance / enlarge

and the next page:

Click to enhance / enlarge

The green highlighted line represents the quarter of strong breadth with the blue line the quarter(s) that follow, and the strong breadth reading usually portends favorably for the next year, as the first table indicates.

On the flip side, a bearish SP 500 earnings perspective from DataTrek Research:

Q2 Earnings, Stress Tests, and Bitcoin $9000

With 2 weeks left in Q2 2019, it’s time to start thinking about what US corporate earnings season will bring. By way of a quick review, here are the summary statistics for Q1:

S&P 500 earnings were essentially flat, down 0.3% versus Q1 2018.

That was better, however, than the -4.0% comparison analysts were expecting on March 31st.

After-tax corporate margins were down from 11.7% (Q1 2018) to 11.0% (Q1 2019). Of the 11 sectors of the S&P, 9 saw lower net margins. Utilities were the only group to see margin expansion (12.8% Q1 2018, 13.2% Q1 2019). Industrials were flat year-over-year at 9.0%.

Another way to look at that margin compression: Q1 revenues grew by 5.3% but, as noted in the first bullet, earnings growth was zero.

Keep in mind that this zero-growth earnings performance came even as the US economy grew at 3.1% and hope lingered for a Q2 resolution of a US-China trade agreement. Q2 is looking slower, with the average of Atlanta/NY Fed GDP models running at 1.7% GDP growth. As for how trade talks develop from here, things seem less certain than in Q1.

Against that backdrop, here is what Wall Street analysts are expecting for Q2 2019:

Earnings that are 2.5% lower than last year.

Revenue growth of +3.9% vs. last year.

In terms of revisions to these expectations since March 31st, analysts have been chipping away at both. At the start of Q2, they were looking for earnings growth of -0.4% and revenues growth of 4.5%.

FactSet, where we get all this data, does note that analysts have not cut their Q2 numbers by as much as they usually do (2.3% lower vs. long run averages of 3.1% – 4.2%).

Also worth noting: companies have been busy lowering expectations for Q2 at a more pronounced rate than usual. FactSet counts 112 companies that have issued Q2 guidance, and in 87 cases those were lower than expectations. This works out to a 78% ratio, higher than the 5-year average of 70%.

Here’s what we make of all this:

#1. Expect to hear further Q2 earnings warnings over the next 2 weeks. Tis the season, after all, as companies square their actual Q2 results with analysts’ expectations.

#2. However, earnings expectations are low enough that Q2 should end up with small positive earnings growth to last year. If the companies of the S&P 500 beat earnings by their typical 3-4%, that -2.5% Q2 consensus expectation should flip to +1.5% or a little more.

#3. That said, margins are still a problem since revenue growth of 4% will not be translating into similarly increasing earnings. Companies are clearly reluctant to cut staff/investment just yet, waiting for the US/global economy to “grow into” their cost structures. This will no doubt be the source of many analysts’ questions during Q2 earnings calls.

Past this pretty benign Q2 outlook, we are wondering how much longer Wall Street can hold onto its upbeat expectations for later this year and into 2020. The numbers here:

While Q3 estimates look a lot like Q2 (4.0% revenue growth, 0.0% earnings growth), analysts’ expectations for Q4 are much more upbeat at +4.5% revenues and +6.8% earnings. Yes, Q4 2018 is an easy comp, but that still seems aggressive to us.

Right now, analysts have +10.7% earnings growth in their models for Q1 2010 and +13.3% for Q2 2020. Moreover, they expect some pretty health margin expansion because Q1/Q2 revenue comps are 6.1%/6.8%.

For all of 2020, Wall Street currently has an S&P 500 earnings number of $186/share, up 10.7% from this year’s $168/share.

The good news is that no rational investor believes earnings will be 11% higher next year, and neither (apparently) does the Federal Reserve. The last time that happened (ex 2018’s tax law change) was in 2017, when global GDP growth was 3.8% (IMF data) and US GDP growth ran at/near 3% for three quarters in a row (BEA data). Best case, US earnings growth is running flat-slightly higher just now, as we’re seeing with Q2.

Bottom line: Q2 earnings should be up slightly, but numbers have to come down considerably for 2020 because global economic growth is slow and earnings leverage is essentially zero. That puts market direction in the hands of the Federal Reserve and the bond market for now. And, as we’ve been highlighting lately, makes for a choppy near term market outlook.

Source: DataTrek Research update, Sunday night, June 16th, 2019

Summary / Conclusion: Because the SP 500 has been flat now for what is essentially an 18-month period, the sentiment data, economic commentary and now as you can see the SP 500 earnings commentary (DataTrek sourcing Factset) has definitely turned negative as well. Wilbur Ross noted over the weekend according to the Wall Street Journal that President Trump will have no hesitation to lay the additional tariffs on China if the G20 and the trade talks show no China movement on the relevant discussions.

In 1994, the Fed / FOMC / Greenspan raised rates 6 times and at what point later in the 1994 raised the fed funds rate 75 basis points in one single hike, with the point being that despite the FOMC activism, the SP 500 finished 1994 flat on the year (if memory services correctly the SP 500 returned 1% for calendar 1994 despite SP 500 earnings growth of 20%).

Today, the SP 500 is flat over 18 months, and stock market sentiment is similar, but earnings growth is nowhere close to what we saw in the 1990’s.

The SP 500 has seen no “PE expansion” in 18 months.

In the above SP 500 earnings analysis, Nick Colas and Jessica Rabe say that “no rational investor” thinks that SP 500 earnings will grow 10 – 12% in 2020, as the IBES data currently expects, but be careful with blanket statements such as the one DataTrek makes (and I subscribe to the DataTrek product) since this blog post in 2016, was a good prognosticator for 2017’s SP 500 return of 22%.

Still Im not expecting 2020 to see a 20% SP 500 return yet, and only until the tariff issues are firmly resolve might we have a chance at a market where the SP 500 PE expands sharply.

SP 500 breadth is an unambiguous positive (as above details) for the SP 500, but President Trump can send the SP 500 down 2% – 3% with one tweet, so stay on your toes.