(Readers, if you havent already don’t forget to re-subscribe to the blog. We’ve made some technology changes and plan on getting rid of the RSS feed. It’s free to subscribe – please renter your name and email on the www.fundamentalis.com website.)

Usually for heady economic topics or concepts, I’ll defer to Jeff Miller over at www.dashofinsight.com or Brian Wesbury at First Trust to gather an informed opinion first.

My own impression of the headline question is that the Treasury market always fears wage inflation first, and then commodity inflation if at all.

But take that opinion with a grain of salt.

Why ? Given my 25 years in the market and my studying of both US and economic history, commodity inflation has often proved “transitory” while wage inflation – which has certainly been stifled thanks to technology and productivity gains from technology the last 25 – 30 – once embedded, would seem to be much harder to contain.

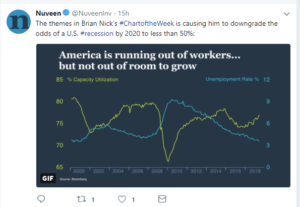

Nuveen, here in Chicago, does some solid research, and this weekend on Twitter (@nuveeninv) the above GIF was posted that addresses a very important topic in my opinion. What will happen with jobless claims and “average hourly earnings” as the US economy’s unemployment rate continues to drop below 4% (with the last employment number, the US unemployment rate fell to 3.9%, the lowest since early 2000’s), and frankly could continue to drop more.

The US hasnt had an annual unemployment rate below 4% since the 1960’s, at the time of the Vietnam War.

Nuveen here in Chicago does some good research, mainly on municipal bonds, but Bob Doll publishes research weekly on the equity markets.

The above Nuveen GIF makes an important point – with the jobs number this week, coming out Friday, June 1, 2018, and the expectations for 180,000 to 200,000 net new jobs added within the US economy, what if the US labor force continues to be depleted and more and more workers are gradually pulled into the US economy ? What will that do to wage inflation and how nervous will that make the Fed ?

Technology is a great productivity enhancer, but even that has its limits. We could see an accelerated move to more robotics, as the US labor force shrinks, not so much due to supply as continued steady demand.

You don’t read much about this, but an unemployment rate below 4%, fiscal stimulus thanks to tax cuts and heavier spending, the President and Congress contemplating additional tax cuts, and its hard to believe that wage inflation doesn’t – eventually – run a little hot. With the move in crude oil – until the last week – commodity inflation was starting to perk up too.

I haven’t really answered the headline question, but wanted to write about it to start thinking through the arguments.

Thanks for reading, and for blog readers, don’t hesitate to offers your thoughts and opinions.