Unless you live in a cave, or fail to turn on CNBC (despite your love for the markets), you are probably aware that there is a Federal Reserve meeting on Wednesday, June 19th, 2013, with an announcement to follow.

All ears are pinned to “taper” commentary, since Fed Chair Ben Bernanke gave us the “kinda, maybe” we will start thinking about tapering, during his May, 2013, Congressional testimony. (I think the May ’13 Bernanke update to the Hill used to be known as Humphrey-Hawkins, but I do think that name was dropped and it is just known today as the Semiannual update. Need to check on that…)

Remember, “tapering” is just less purchases of Treasuries / Mortgages. The way it was described to one client was that, “The Fed is just pressing less hard on the gas pedal, and they are not hitting the brake.”

Tapering does not mean “liquidity withdrawal”, it just means liquidity is being added at a lower rate, and the Fed is being slightly less supportive.

Frankly, I think it all nonsense anyway. The 10-year Treasury is the key security to watch, and the Treasury market will be far out in front of the Fed anyway. This is what the term “bond vigilante” means – the traders will be out in front on interest rates, pushing the yield as the talking heads and the bloggers enhance global warming with all their hot air and screeching about “Fed intent” (this blog included).

The smart money seems to be betting that September, ’13 meeting is the definitive month where the Fed announces a smaller amount of purchases (tapering).

Watch the 10-year Treasury yield, closing today at 2.19%. Personally, I think it is headed to 2.40%, the March, 2012 high, and ultimately higher.

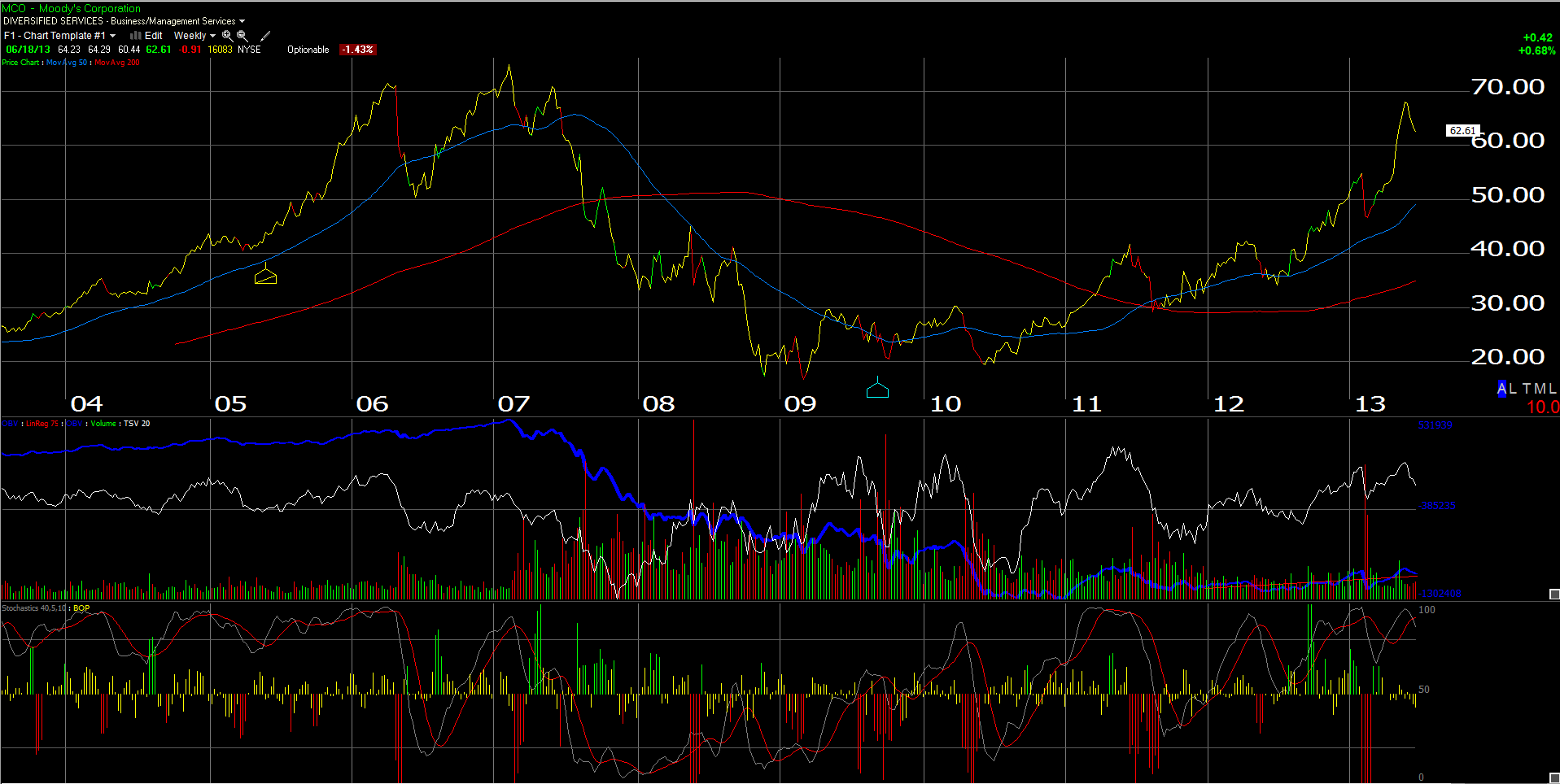

The Chart

We always like to leave readers a chart to chew on. The chart at the top of the page is Moody’s (MCO), the iconic rating agency that is a barometer of interest rate activity.

MCO has benefitted immensely the last few years from lower interest rates and tighter credit spreads, which has allowed Corporate America to refinance trillions of dollars in corporate debt and to lock in lower financing for the next 10 years.

It looks like MCO has topped already, and is in the earlier stages of breaking down, BUT that will depend on how fast interest rates do increase.

We have sold all of our MCO, most too early, since our last position was sold near $45. Moody’s is the ultimate in interest rate sensitive stocks, with the possible exception of mortgage company stocks, since bond issuance volume is interest-rate sensitive.

We would own MCO again with a “$3 handle”, preferably the low $30’s. As the 10-year Treasury yield increases, MCO should decline. Higher rates should slowly start to impact issuance volume in the corporate and municipal bond markets.

Warren Buffett publicly panned Moodys (MCO) after the 2008 Financial Crisis and the stock ran from $19 to $70. Even brilliant investors get it wrong sometimes.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager