Actual technology sector earnings were pretty strong for Q2 ’25: on July 3rd, ’25, the expected EPS growth for the tech sector was +17.7%, but the actual EPS growth for the sector is now +25.0%, for an upside surprise of 730 bp’s. That’s the strongest upside beat since Q1 ’24’s 610 bp’s for the tech sector, and puts a lance through my worries that spurred this article in early July ’25.

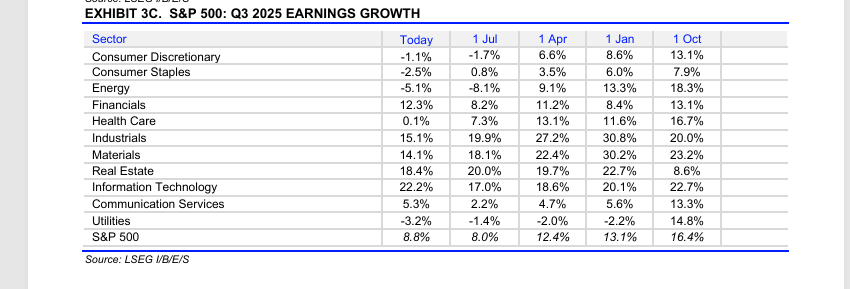

The above table cut-and-pasted from LSEG’s “This Week in Earnings” shows 4 sectors that have improved or seen positive revisions to the expected EPS growth for the sector for Q3 ’25:

- Consumer Discretionary;

- Energy;

- Financials;

- Technology;

Consumer discretionary, dominated by Amazon (AMZN) and Tesla (TSLA), will also see Nike (NKE) report their fiscal Q1 ’26 earnings this week, 9/30. Nike is a member of the consumer discretionary sector. Where is the upward pressure coming from for the consumer discretionary sector ? That’s typically addressed in the pre-earnings previews.

Energy saw a sharp improvement in the expected EPS growth rate for Q3 ’25, although it’s still negative.

Financials: it’s hard to imagine a better combination of tail winds for financial stocks coming into Q3 ’25: tight credit spreads in the public credit markets, continued low losses and charge-offs reported for the big banks consumer credit card operations, housing is slower but mortgages saw a burst of re-financings in the last month, the investment banking businesses for equity and debt should be healthy, the asset management businesses should also be healthy, etc. Normal expected EPS growth for the financial sector is usually mid-single-digits, so the starting point of 14% for Q3 ’25 EPS growth for financials, implies some confidence by analysts that the numbers will be there. What’s probably helped financials is that loan losses were increased in 2022 as the Fed was raising rates given all the recession forecasts that proliferated at that time, which means that loan loss reserves will be less as the sector moves forward.

The tech sector’s expected EPS growth rate has been revised higher by 730 bp’s since July 1 ’25. That’s a strong trend. Expected EPS growth for the tech sector in Q3 ’25 is +25%, which is a very high bar for the sector, since Q2 ’25 EPS growth for tech was +25%. The only quarter where the tech sector saw faster EPS growth (outside of the COVID period from 2020, 2021) was Q2 ’24, when technology EPS grew +27%.

Are we potentially looking at peak tech EPS ? Remember the capex spending does NOT impact EPS, i.e. capex is not run through the income statement, but capex DOES impact valuation, and the capex line is found on the statement of cash flow, under the “investing” section. Capex impacts valuation since higher capex – like the AI spend – reduces free-cash-flow (FCF), and lower FCF – ceteres paribus – lowers the valuation. Analysts can play with it and maintain the intrinsic value estimate, but I think it would require adjusting (i.e. lowering) the discount rate. Here’s an article from a little over a year ago, that tried to address this issue.)

Readers should be reminded that – while the typical pattern for EPS estimates coming into a quarter’s report is to see negative or downward revisions – the stock and sectors that see positive or upward revisions, are usually more telling since the analysts typically get reluctant to boost EPS and revenue estimates in front of a report.

Here’s a little history on the technology sector earnings (EPS) growth:

q4 ’11 – q4 ’19: The tech sector’s average EPS growth rate over this time period was +10.8%. The peak growth rates of 28% – 30% occurred after the Tax Cuts & Jobs Act (TCJA) signed in December ’17, which allowed companies like Microsoft, Oracle, Apple and others to repatriate cash from foreign countries held abroad due to tax issues. The TCJA repealed that tax hit on funds held abroad, and billions of dollars came home for share repurchases, capital investment, etc.

Q1 ’20 – Q4 ’22: The average tech sector EPS growth during the COVID-influenced period was +19.09%, with peak quarters of 45% – 50% which lapped Q1 and Q2 ’20, or the quarter’s with the biggest hit to tech sector earnings from COVID.

Q1 ’23 – Q2 ’25: The average tech sector EPS growth was +16.7% over this period, but it’s somewhat distorted by Q1 ’23’s -8.3% growth rate. Removing this only negative quarter results in an average of +19.5% for the tech sector. Three of the last 7 quarters have seen the tech sector report 24% or better in terms of EPS growth, and Q2 ’25 was +25%.

Summary / conclusion: The bearishness around AI and the tech sector seems to have increased markedly the last month. Technology EPS growth is near or nearing peak levels from any point in the last 15 years or the post-financial crisis. Is a 15% tech sector EPS growth rate going forward going to result in sharp selling within tech ? When the large-cap growth and technology sector bubble popped in March, 2000, tech sector earnings were negative for 2 – 3 years. The AI buildout is a juggernaut: it will change technology permanently. My biggest worry within the sector is the seeming disparity between rising EPS growth and rising (and record) capex, which – for investors with a valuation background – presents a rather unusual conundrum. Rising earnings, revenue and cash-flow is good and typically results in rising valuations, while sharply increasing capex and falling free-cash-flow, should (maybe) force lower valuations in a sector.

This requires another article before Q3 ’25 earnings start just to address the issue.

For now, investor should enjoy the run, and if historical earnings patterns mean anything, Q3 ’25 should results in a fairly supportive platform for SP 500 stocks.

None of this is advice or a recommendation but only an opinion. Past performance is no guarantee of future results. All SP 500 EPS data is sourced from LSEG.com. None of the above data may be updated and if updated may not be done in a timely manner.

Thanks for reading.

One man’s capex is another man’s revenue

true.