FedEx (FDX), the freight and transport giant, reports their fiscal Q4 ’25 after the closing bell, next Tuesday, June 24th.

The stock is down 20% YTD in ’25 and down -7.77% in the last twelve months after guiding lower for fiscal Q4 ’25 in March ’25, and has now guided the last 3 quarters lower, despite the focus on reducing FedEx’s cost structure by $2 billion.

After becoming positive on FedEx’s prospects after management initiated the cost reduction and FedEx One (consolidation of operations), in early 2023, the earnings release in December ’23 was not a positive and decided to exit the stock. (The problem with FDX as this blog has written many times about the freight giant, which is also true of many industrial companies, is a small slowdown in revenue can cause much bigger changes in EPS thanks to the operating leverage.)

Even with the Freight spinoff, which is due to get completed sometime in fiscal ’26, the stock hasn’t been able to generate any upside.

On Tuesday night, June 24th, 2025, analyst consensus is expecting FedEx to print $5.87 in earnings per share, on $21.8 billion in revenue, and $1.95 billion in operating income, for expected year-over-year (y-o-y) growth of +9%, -1% and +4% respectively.

Eight of the last 11 FedEx quarters have seen negative y-o-y revenue growth. If FedEx meets the revenue estimate Tuesday night, FDX revenue for fiscal ’25 will have been flat, with just 2% expected for fiscal ’26.

Fiscal ’26 guidance today is expecting $19.75 in earnings per share on $87.5 billion in revenue for expected y-o-y growth of +9% and +2% respectively.

The onset of the pandemic in March, 2020, resulted in a huge surge in volume and operating leverage across the FedEx system, only to see this slow in 2022 (and continue to slow) with the rate hikes.

Revenue growth rates (yoy):

- 4-quarter avg: 0%

- 12-quarter avg: -1%

- 20-quarter avg: +6%

- 40-quarter avg: +7%

Operating income growth (yoy):

- 4-quarter avg: -2%

- 12-quarter avg: -2%

- 20-quarter avg: +19%

- 40-quarter avg: +9%

Valuation:

FedEx stock is about 10% -15% cheap to perceived intrinsic value (probably not enough of a discount to attract long-term investors given the operating leverage involved at FedEx), at it’s current price around $223 per share, trading at 12x earnings for expected EPS growth in fiscal ’26 of 9% on 2% revenue growth. The compelling valuation metrics for FDX are the price-to-TTM revenue value of 0.6x, and the price-to-TTM cash-flow metric of 7x. (TTM is trailing twelve month.)

The 6% free-cash-flow yield looks compelling as well.

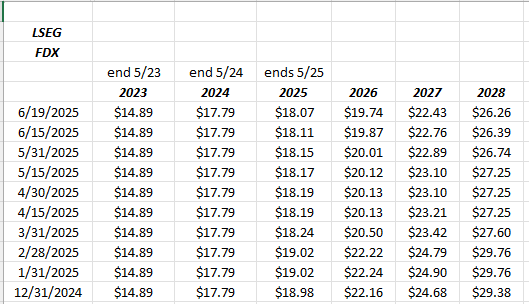

Trends in EPS and revenue revisions:

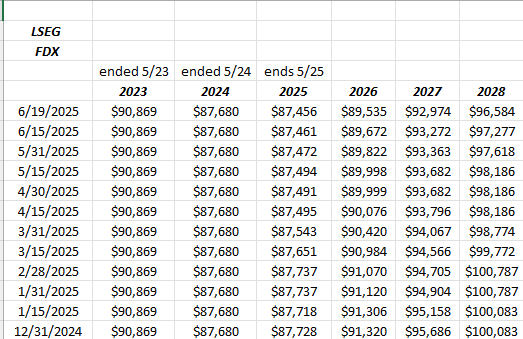

Trends in revenue revisions:

Neither of these EPS and revenue revisions portend well for FedEx. The revisions remain negative, and the revenue revisions are more worrisome than the EPS revisions.

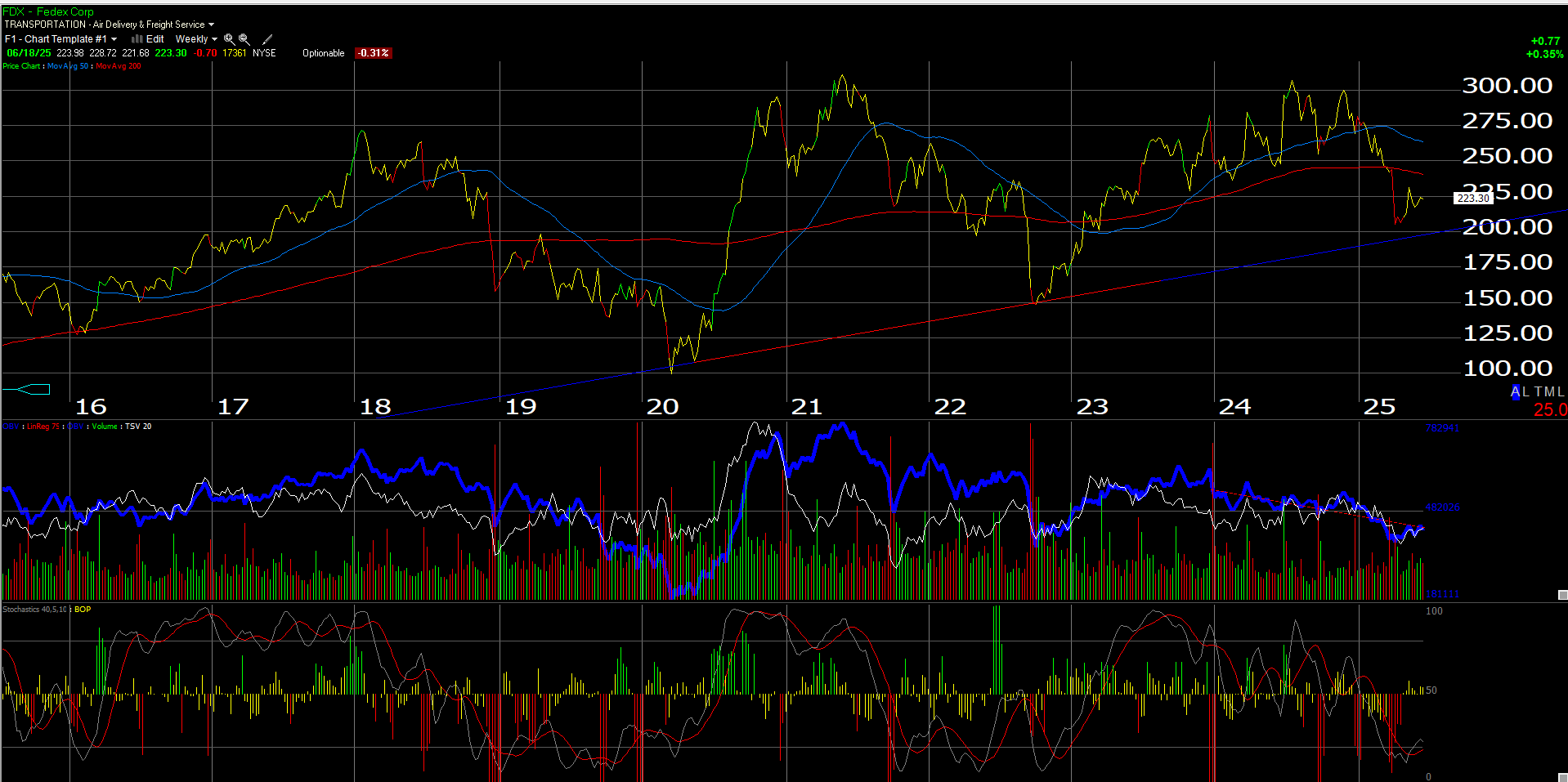

The chart:

Summary / conclusion: Looking at XPO Logistics (XPO) and UPS stock, both well off their all-time-highs (and UPS is looking far worse than XPO or FedEx,) it’s clear that FedEx’s issues are not all company-related. Increased Ground competition from companies like Shein and others, following in Amazon’s footsteps with a proprietary home delivery service, i’ve wondered now these services impact FedEx Ground. (UPS peaked at over $233 per share in early ’22, but is now trading under $100 per share. Haven’t followed the stock fundamentally since the 1990’s. No opinion on it’s investment merits, and never followed XPO either, just looking at charts.)

The negative EPS and revenue revisions are the biggest issue around FedEx right now given the tariff kerfuffle, the sharply higher crude oil price (jet fuel for FedEx), but FedEx can put on a fuel surcharge to protect itself from higher crude prices.

Technically, the upward-sloping trendline for FedEx stock off the Covid March ’20 lows is around the $200 share price (see above chart) or roughly 10% lower than where the stock is trading today.

Clients have no position in the stock other than one longer-term, tax sensitive client that has a FedEx position purchased in March, 2000. The key question for readers though is would this blog commit to a decent weighting in the stock if FDX should trade below $190 – $200 over the next few quarters, and I’m sure that will happen. (Will try and answer that at a later date.)

None of this should be construed as advice or a recommendation but only an opinion. Past performance is no guarantee of future results. The information above may or may not be updated, and if updated may not be done in a timely fashion.

Thanks for reading.