Source: LSEG

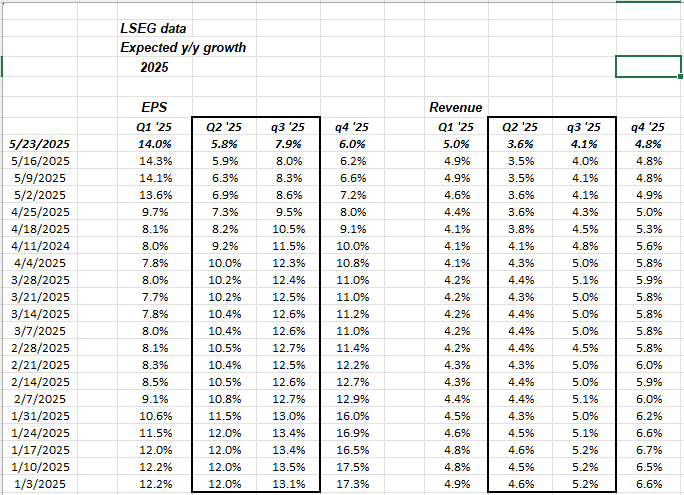

Jamie Dimon was out this week with one of cassandric economic forecasts, and this time it had to do with SP 500 earnings, with Jamie expecting a 0% SP 500 expected EPS growth rate for Q2 ’25, by the time reporting starts in July ’25. He may not be wrong, but the way the “tariff” discussion has evolved, for the expected +10% SP 500 EPS growth rate for Q2 ’25 to fall all the way to 0% by early July ’25, would be pretty extreme indeed, with the only instance I can think of that happening to that degree would have been Covid and the first 6 months of 2020.

This week in the 3rd column, of the black-bordered areas, the Q3 ’25 trend in both SP 500 EPS and revenue was added just to see how analysts are modeling for Q3 ’25, since it appears these two quarters will bear the brunt of the majority of any tariffs implemented.

Looking at the above spreadsheet, since January 3rd, the 2nd quarter has seen more severe revisions than the third quarter, but some of that “severity” is partially due to the Q2 ’25 quarter being next to report and historically the upcoming quarter sees the harsher revisions.

As someone who looks at this data religiously every weekend, be careful of staking an investment decision off it, since the next tweet could change the frequency and severity of revisions entirely.

It’s a tough environment if you are quantitatively-focused on earnings and data. It could all change with a tweet storm.

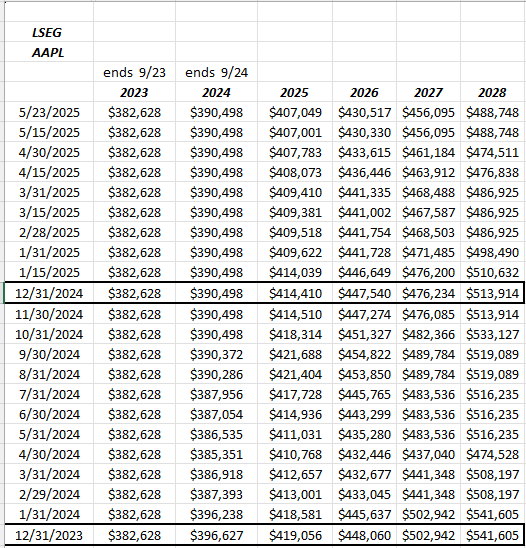

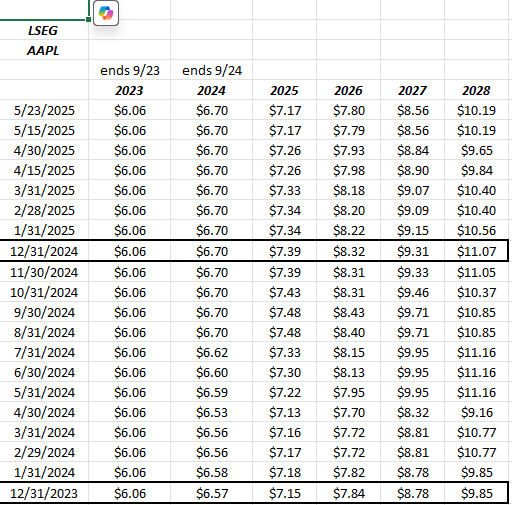

Apple EPS and revenue estimate revisions:

The first table above shows Apple’s revenue revisions. Note how from 12/31/2023 to 12/31/2024, Apple’s expected 2025 total revenue fell $5 billion over the 12 months, but since 12/31/24, and as of 5/23/2025, Apple’s fiscal ’25 revenue revisions have fallen $7 billion.

Apple’s EPS revisions are more interesting: rather than negative revenue revisions, Apple’s full-year 2025 EPS estimate is basically unchanged over the last 17 months, after rising nicely for the twelve calendar months of 2024. Fiscal 2026 and 2027 EPS see the same pattern i.e. upward revisions in 2024, but since 12/31/2024, steady downward revisions for all three fiscal years which have left EPS basically unchanged over the 17-month period.

Most of the headlines around Apple the last 12 months have been AI-related (analysts critical of the seeming lack of Apple’s AI progress), while tariff issues have arisen in calendar ’25.

Two things struck me about Apple: The Board of Director’s announced a $100 billion increase in the share repurchase authorization, with the April ’25 results and the stock fell after the earnings release. Also, these negative EPS revisions have a great weight on the SP 500 since Apple’s “earnings weight” is bigger than it’s market cap weight in the SP 500. Of the top 3 market cap weights currently in the SP 500, Microsoft’s and Nvidia’s earnings weights are lower than their market cap weight, while Apple’s earnings weight is larger.

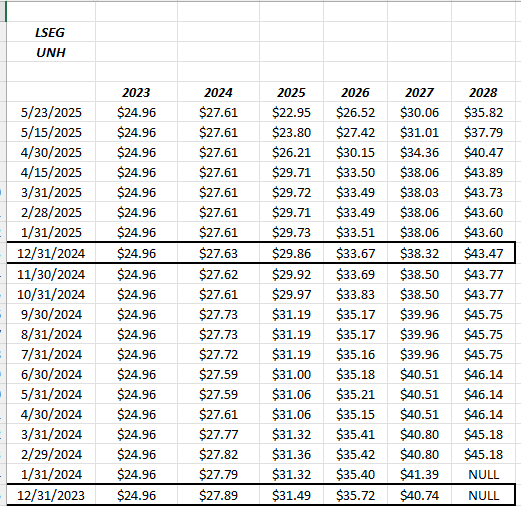

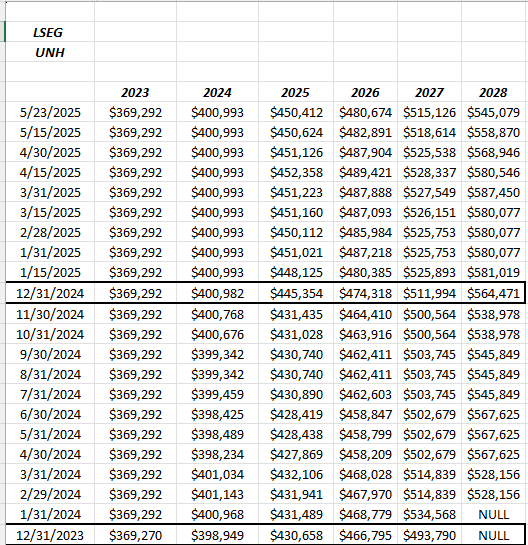

United Health EPS and revenue revisions:

The one aspect that struck me about United Health’s (UNH) EPS and revenue revisions, is that revenue revisions remained staunchly positive until mid-April ’25 and only since then have started to roll over, but notice how the analysts are still looking for y-o-y revenue growth for 2025, 2026 and 2027.

The EPS estimates looked to peak last fall ’24 and then started to slowly decline.

Having never owned or followed UNH, I have no opinion on the stock or it’s outlook. Bespoke had a note on UNH in the past few weeks when the stock looked to be bottoming, noting that the corporate bonds were trading much better than the common stock, which is definitely a credit positive.

Summary / conclusion: Long weekends are a good time to catch up on market articles. There’s a few more in the pipeline for this weekend.

A note was sent to clients Thursday or Friday, saying that any pullback in the SP 500 would / could find support at the 5,500 area for the SP 500 since it’s roughly the 50% point of the SP 500’s trading range from the mid-February ’25 highs to the April lows for the SP 500.

Credit spreads actually rose a smidge this past week, after tightening smartly since early April ’25.

More to come over the weekend.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time. None of this information may be updated, and if updated may not be done in a timely fashion. Clients and readers should gauge their own comfort with market and portfolio volatility and adjust accordingly.

Thanks for reading.