While we wrap up Q4 ’24 SP 500 earnings in the next trading days, it truly is hard to exaggerate or embellish how strong Q4 ’24 SP 500 earnings growth turned out to be.

Some of this strength I’m sure was partially due to President Trump’s election, and what appeared to be the surge in imports in Q4 ’24 to beat the expected tariff war in 2025, and some was undoubtedly due to the fact that a Republican President and Administration, not to mention a Republican Congressional majority, is generally thought to be pro-business, anti-tax, and anti-regulation.

Here’s some of the numbers on Q4 ’24 SP 500 earnings:

- The SP 500 EPS growth for Q4 ’24 (as of 3/21/24, and per LSEG data) rose +17.1% y-o-y, versus the +9.5% expected in early January ’25.

- That’s the strongest rate of quarterly growth for SP 500 earnings since the 4 quarters of 2018, which were materially, positively, impacted the TC&JA, in December, 2017.

- The 4 Covid quarters were materially stronger in 2021, but that was due to the negative SP 500 EPS growth in the 4 quarters of 2020.

- The fact is – given Q4 ’24 was not Covid impacted or corporate income tax-adjusted – the highest quarterly SP EPS growth print between Q4 ’11 and Q4 ’17, the Q4 ’14 actual EPS print of +14.8.

While last week’s blog noted how the growth rates were changing for Q4 ’25 (here), you can’t fault the analysts (and strategists, for that matter) for being a little conservative with bottom-up EPS estimates for the SP 500 looking forward, especially after this strong run.

When final adjustments are made after March 31 ’24, the numbers are expecting the following SP 500 EPS growth rates for the following calendar years:

- 2026: +14% annual EPS growth expected, up from +13% last fall, but the least material of these estimates. (There’s plenty of time for the numbers to change).

- 2025: +10% – 11% annual EPS growth expected, down from 12% – 13% last fall.

- 2024: +13% – 14% annual EPS growth is expected, up from +10% last fall, after the remarkably-strong 4th quarter of ’24.

A perfect example of how the stock market is a “discounting mechanism”, the last two years the SP 500 benchmark returned 25% each year for 2023, and 2024. SP 500 EPS growth in 2023 was +1%, and for 2024, it should be closer to 13% – 14%.

That’s the perfect example of PE expansion.

The investment community hasn’t seen two straight years of SP 500 EPS growth since 2017 and 2018, or with the afore-mentioned passing of the TC&JA, and prior to that it was 2010 and 2011, or the “post-2008” SP 500 EPS rebound.

While this blog hesitates to in anyway be political, the fact is the President and the Republican Congress are sitting on a pretty solid runway of expected SP 500 earnings growth, which hopefully won’t be tampered with too egregiously.

The fact is the tariff issues, the budget deficit issue, and DOGE could wind up being “contractionary” to US GDP growth over the next 12 – 24 months.

SP 500 data:

- With one week left in the quarter, the forward 4-quarter SP 500 estimate (FFQE) fell to $269.78, versus the $270.36 from last week.

- The PE ratio on the forward estimate is 21x, 20.8x last week and 21.8x to start the quarter.

- The SP 500 earnings yield ended the week at 4.76%, vs 4.79% last week and 4.59% to start the quarter.

- High-yield credit spreads tightened this past week to 319, from 340 last week, definitely a positive.

- The SP 500 EPS “upside surprise” sits at +6.9% for Q4 ’24 as of Friday, 3/21, only exceeded by Q3 ’24’s +7.5%, and Q1 ’24’s +8%.

Summary / conclusion:

One goal for tracking all of this SP 500 earnings data is draw some conclusions about longer-term growth rates, not just for the SP 500, but for the 11 sectors as well, but that’s difficult with the pandemic’s impact on earnings, and then the bounce following the pandemic, and the “one-time” impact impact of tax cuts or tax hikes (like we saw under the Obama Administration).

Politics matters, that’s for sure.

If we get high-single-digit SP 500 EPS growth rates over the next two years – i.e. 2024 and 2025 – it would be a plus in my opinion. I’ve said it before, I do think the Republican Congress are hindered or constricted in terms of income tax cuts, or reducing the corporate tax rate, given the pressure of reducing the budget deficit.

Treasury Secretary Bessent noted that reducing the budget deficit as a size of the US GDP is a top priority.

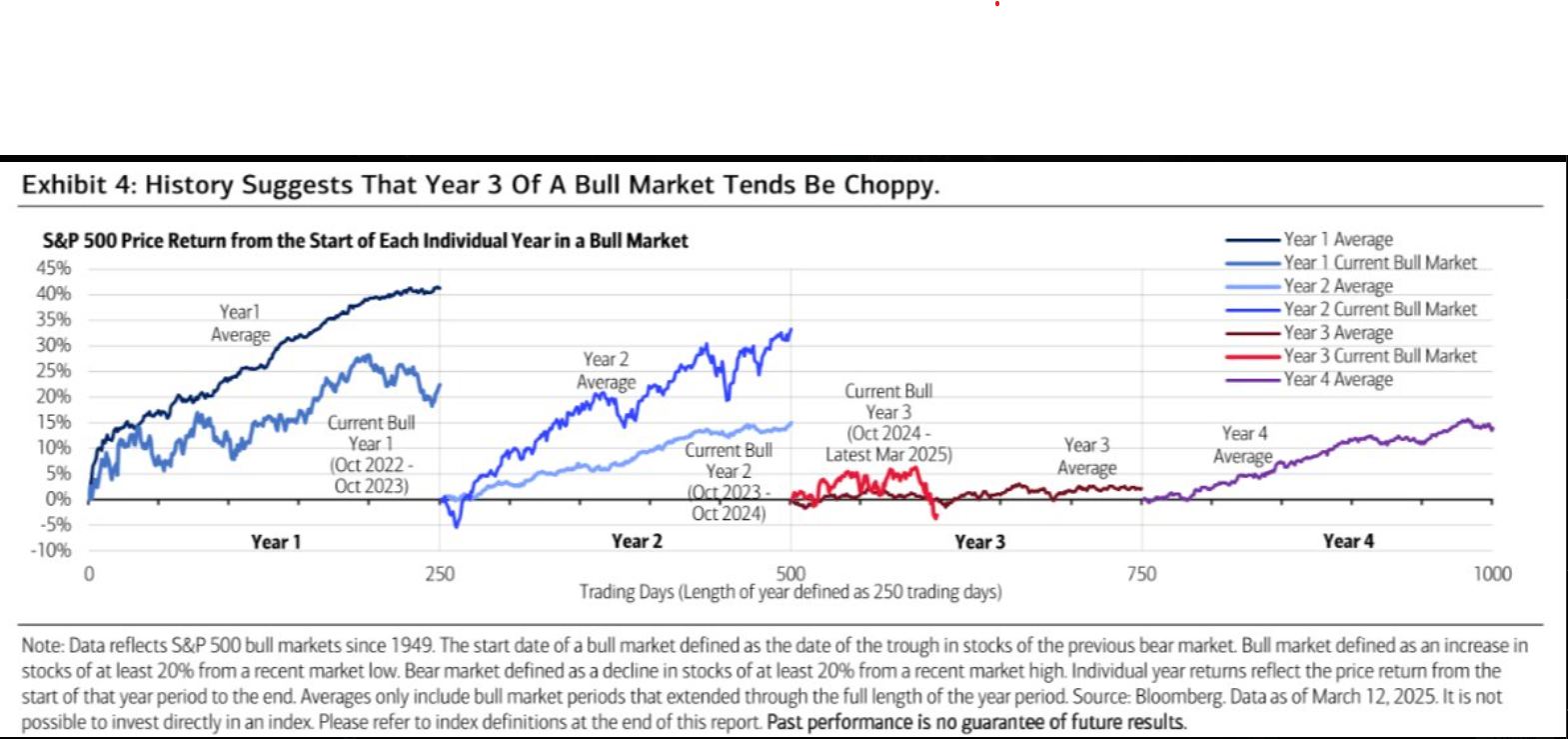

Here’s an interesting chart from Mike Zaccardi accessed via X, which is consistent with this blog post from November 10, ’24, and this blog post from December 28 ’24, which talks about a year of “PE contraction” lying ahead.

The street is flooded with many predictions on a daily basis, none of them very good, so take everything with a grain of salt.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time. All SP 500 EPS and revenue estimates are sourced from LSEG. None of the above information may be updated, and if updated, may not be done in a timely fashion.

Thanks for reading.