Excellent chart sourced from Gary Morrow (@garysmorrow on X) showing the SP 100 or the OEX, reaching it’s most oversold since October, ‘2022, and yet sitting right on longer-term support at the light green zone, stretching back to June ’24.

The leadership of the last two years, mainly the Mag 7, and financials, continue to take a beating, but even Netflix (NFLX) was hammered this week. JPMorgan (JPM) is trading $40 or roughly 15% off it’s all-time-high near $280 hit February 19th, ’25, (at Friday’s low tick of $239), and it’s doubtful the “macro” has changed that much.

SP 500 earnings and recession watch:

Not to bury the lede, but the SP 500 earnings yield jumped to 4.69% this past week, it’s highest print since the 4.68% hit on January 10, ’25, and only exceeded by the September 6, ’24 print of 4.82%.

Personally, I’d prefer it sit above 5%, and let the market climb the wall of worry, but the highest EY in 8 weeks, along with the above chart of the SP 100, might indicate a tradeable bottom is getting close. Plus, there is just 3 weeks left in the first quarter, so readers should expect somewhat of a bounce with the VIX now at it’s highest since December ’24.

Anyway, none of this is a prediction, just reading the tea leaves.

- The forward 4-quarter estimate fell $0.04 this week to $270.40 from $270.46 last week, and $272.67 to start the quarter.

- The forward PE fell to 21.34x this week, versus the 22x last week and the high print for the quarter of 22.6 for the week ending 2/14/25.

- High-yield credit spreads have risen to 288, after bottoming at 259 on 1/24/25 (per the Bespoke data).

- While the revenue upside surprise for Q4 ’24 earnings is relatively average at +1.2%, the EPS upside surprise for SP 500 earnings is the third strongest of the last 5 quarters at 6.9%. The weakest of the last 5 quarters was Q2 ’24 at just +4.6% EPS upside surprise.

- The aforementioned SP 500 earnings yield ended last week at 4.69%, the highest since last September 6th ’24’s 4.82%.

The difference in the SP 500 earnings yield in early March ’25, is that the SP 500 EPS estimates are not climbing as sharply as the estimates were in ’24.

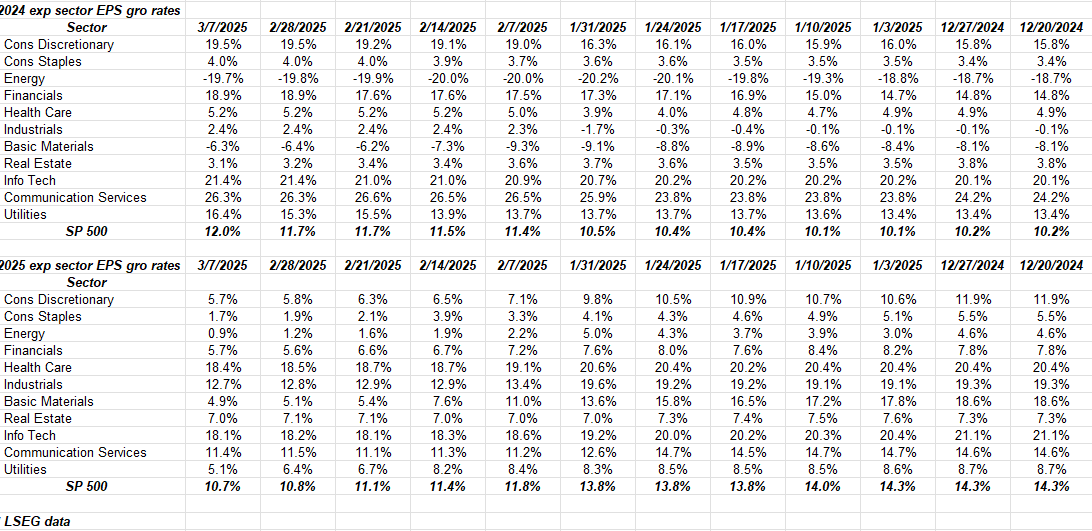

Here’s two tables this blog follows, i.e. expected sector EPS growth rates within the SP 500:

To give readers an idea how strong Q4 ’24 SP 500 earnings were, the total SP 500 expected EPS growth rate for 2024, was 10%, while the current SP 500 EPS expected growth rate for calendar ’24 is now 12%. That’s a big gain in just a few months.

Conversely, analysts have lowered expected 2025 SP 500 EPS sector growth rates, from 14% to 10.7% in the exact same period, some of which is expected given the increase in Q4 ’24, but also tariff unease in the last few months.

The tech sector is expecting slower growth in 2025, given the above estimates, than was seen in ’24, but not by much. Readers can compare the growth for 2024, vs 2025 above.

Some of the expected ’25 slowdown is undoubtedly tariffs, and uncertainty over their impact on individual company earnings for the next few quarters, but some is a sudden burst of “recession” talk by the Street, probably driven by the sharp drop in Atlanta Nowcast’s expectation of Q1 ’25 GDP growth of -2.4%.

Most take that recent Atlanta Fed Nowcast with strong amount of skepticism, but I have to add this to the discussion: this past week, a short break was taken from the grind, and I flew from Chicago Midway to Central Florida for a few days of bass fishing, and a shot at some real sunlight. While sitting at Chicago’s Midway Airport having a late breakfast Wednesday morning, I commented to the woman serving me, that the airport seemed unusually quiet relative to the last few times I’d flown out of Midway on Southwest Airlines. She told me airport traffic started to slow late January ’25 and that while they were waiting for the spring break rush to start, it hadn’t happened yet, and the restaurant manager had been cutting some shifts for some workers.

Because Midway is a smaller airport than Chicago’s O’Hare Airport, whenever you are there it always feels like you are surrounded by the hustle and bustle, but last Wednesday, March 5, ’25, Midway was very quiet.

Summary / conclusion:

The next Fed announcement on monetary policy is due out Wednesday, March 19th, (one week from this coming Wednesday), and the probabilities still reflect (as of today), just a 3% chance of a fed funds rate cut, and hence a 97% probability the fed funds rate remains at a midpoint of 4.375%.

Briefing.com is expecting a +0.3% increase in the Core CPI this coming Wednesday, March 10th, down from the prior +0.4% (January ’25 inflation read, which was a little stronger than the +0.3% expected), so yes, like the January ’25 Core PCE that was released in late February ’25, the February ’25 Core CPI is expected to improve this coming week.

The Core CPI print is what matters.

There’s a number of signs indicating that the larger-cap stocks, which have been the majority of the rally since late ’22, but also in this secular bull market that’s been ongoing for 14 years, could be looking to bottom. The tariffs throw everything off in terms of the valuations and the changing EPS and revenue estimates, so we won’t really know until Q1 ’25 SP 500 earnings start in mid-April ’25.

The probability of a recession – or at least a decent slowdown in US GDP growth – are higher than when ’25 started too.

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of future results. Investing can and does involve the loss of principal even for short periods of time. None of the information posted above may be updated, and if updated, may not be done so, in a timely fashion. All SP 500 EPS and revenue data is sourced from LSEG.

Thanks for reading.