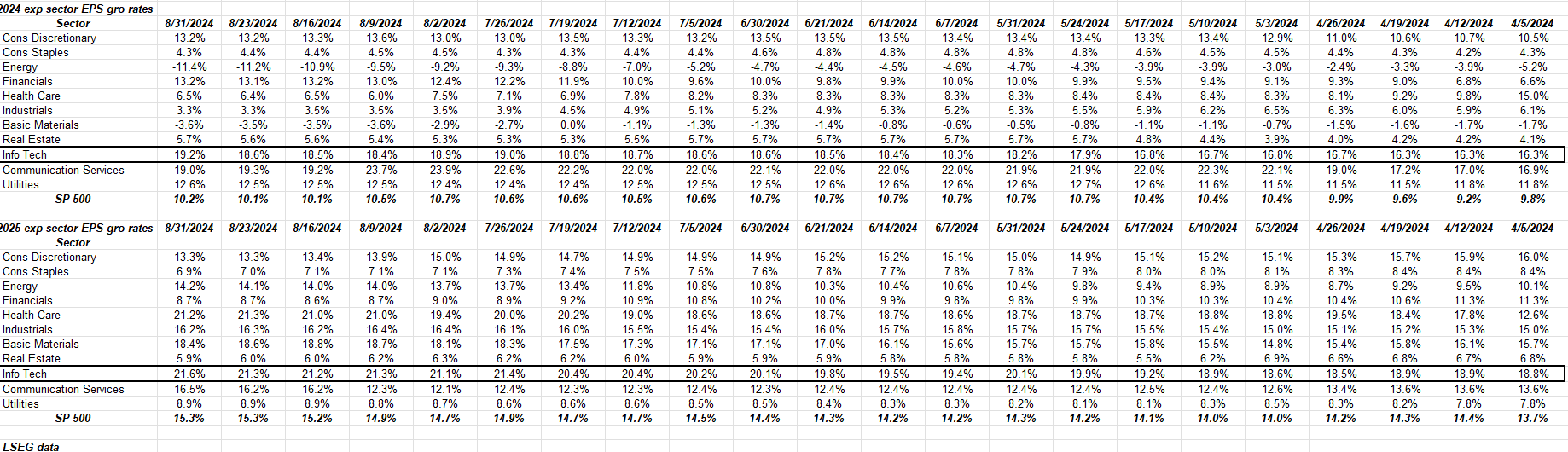

Despite Mag 7 price action, tech sector forward estimates are still rising.

Looking at estimated earnings growth for full-year 2024 and 2025, note how the expected tech sector growth rates are trending:

- 2024 expected tech sector earnings growth has risen about 300 bp’s or 3% since early April ’24.

- 2025 expected tech sector earnings growth has risen about 200 bp’s since early ’24.

For those looking for a head start on which sectors MIGHT outperform in ’25 as a function of rising sector earnings growth, peruse the calendar 2025 table for sectors with rising expected growth since April ’24. Here’s a list of the sectors.

- Energy sector growth for ’25 has risen over 400 bp’s since early April ’24;

- Healthcare sector growth for ’25 has risen over 700 – 800 bp’s since early April ’24 (Health care sector growth in ’24 has been cut in half the last 6 months so don’t ignore that);

- Industrial’s sector growth for ’25 has risen 120 bp’s since early April ’24;

- Basic Materials sector growth for ’25 has risen about 250 – 300 bp’s since early April ’24;

- Communication services sector growth has risen 290 bp’s since early ’24;

- Technology expected tech sector earnings growth has risen about 200 bp’s since early ’24;

- Utilities expected sector growth has risen about 100 bp’s since early ’24;

Here’s a perspective that is rarely talked about in the mainstream financial media: which sectors are looking for the greatest changes in absolute earnings growth for 2025 (versus what is expected in 2024):

- Energy gets the prize currently: as of this week 2024 is expected to decline 11% on the year, versus an expected 14% growth rate for ’25;

- Consumer Discretionary and Consumer Staples are looking for similar (i.e flatter) growth rates in ’25 that are being seen in ’24;

- Industrial’s are expecting much faster growth in ’25 (+16%) versus ’24 (+3%).

- Health Care is also expecting much faster growth in ’25 (+21%) vs ’24’s (+6%);

- Basic Materials too, with +18% expected in ’25 vs -3% in ’24.

Expected technology growth for ’25 as of today, while still seeing positive revisions, is almost expecting a growth rate in ’25 (+21%) that isn’t all that different from ’24’s +19%.

The above sentence could be the reason why the Mag 7 and the tech sector stocks have suddenly gone flat the last 8 weeks. While sector estimates are rising, the absolute change in 2025 expected tech sector’s earnings growth is about the same rate of growth as being seen in ’24.

Looking at the industrials, energy, and basic material sectors, the ’25 expected growth rates look like the industrial economy of America is poised for healthy growth in ’25. Those sectors are roughly 25% of the SP 500’s market cap, with industrials being half the market cap weight of the three at 12%.

Summary / conclusion:

This article had an entirely different title and objective at the start, but the title was changed after writing this piece, which is exactly why you want to have a blog or do a podcast, i.e. so you lay out or articulate the thought the process before drawing the conclusion.

While the goal of today’s blog was to talk about the still-rising earnings estimates in the tech sector, the article broadened out to include all sectors within the SP 500 that are seeing rising sector growth (i.e. positive revisions) in 2025, which is somewhat an unusual pattern.

Also of note was the identification of sectors that will see the biggest absolute swings in expected growth in calendar 2025 (based on today’s estimates), versus 2024, hence readers can see the sectors with the biggest possible swings in growth for 2025.

This weekend, this blog will be out with “Top 10 holdings” for clients and what portfolio changes have been made. Investment advisors, fund managers, and folks who manage their own money, should already be thinking about what 2025 holds.

There is a lot that can go right and wrong: stocks go up for many reasons, i.e. PE expansion, easier monetary policy (i.e. lower interest rates that generate lower discount rates), favorable (i.e. pro-business) tax and economic (fiscal) policies, favorable demographics, and vice versa.

So far 2025 looks positive from an “expected 2025 SP 500 EPS growth” perspective. SP 500 EPS growth looks healthy, and with a possibly-easier Federal Reserve, and a lower fed funds rate, you’d think the interest rate sensitive sectors will outperform. That being said, which other sectors do you wish to overweight and which sectors do you want to avoid ?

None of this is advice or a recommendation, but only an opinion. Past performance is no guarantee of futures results. Investing can and does involve the loss of principal even for short periods of time. Readers should gauge their own comfort level with portfolio volatility, and adjust accordingly.

Thanks for reading.