Oracle reported their fiscal Q4 ’24 financial results after the bell last Tuesday, June 11th, 2024, and while the numbers weren’t great (both revenue and EPS missed consensus estimates), the stock price reaction was notable, probably due to the growth in RPO (remaining performance obligation, which is likely a fancy term for backlog), and the deals with Google and Open AI, around OCI or Oracle Cloud Infrastructure.

This blog has written quite a bit about Oracle over the years (here, here, here, and here) as just a few examples, but AI – at least for now – appears to have given Oracle a new lease on life, and investors are treating it like it’s very much a positive for the enterprise software giant.

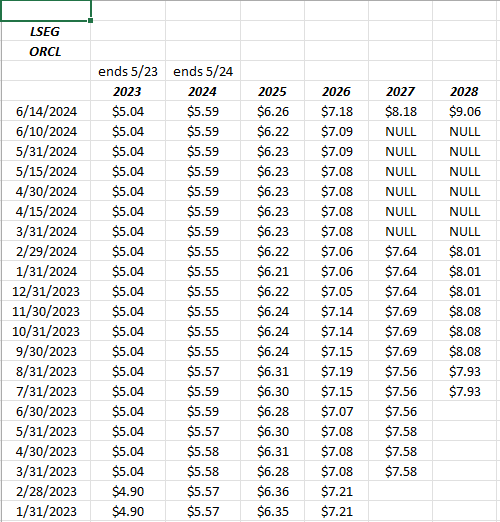

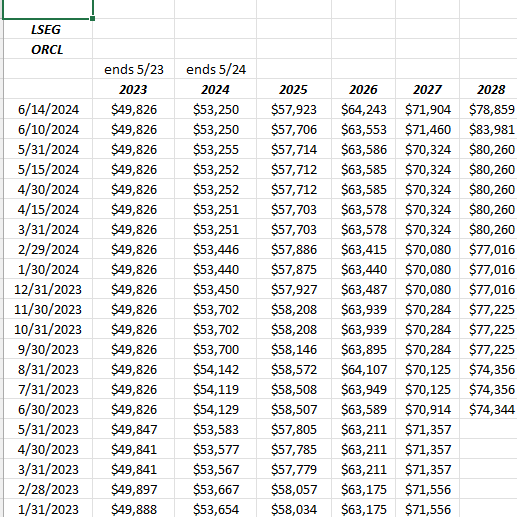

EPS and revenue revisions:

While the stock price reacted positively to Oracle’s latest earnings report, looking at the current EPS estimates, the estimates for fiscal ’25 (started June 1 ’24) are still a little lower than where they were in January ’23. Fiscal ’26 as well.

Part of this could be due to dilution from the Cerner deal as the fully diluted share count has been expanding about 1% – 2% per quarter (on yoy basis) and share repurchases remain well below the 2021 levels of $3 – $4 billion per quarter.

Revenue revisions look pretty stable as fiscal ’24 was almost exact over the last 21 months, while fiscal ’25 revenue estimates trended lower slightly and fiscal ’26 has trended slightly higher.

To the point, EPS estimate revisions are a mild positive for the stock right now. Oracle is not really a momentum stock, as Nvidia is, so keep that in mind.

Valuation:

When Oracle reported their fiscal Q4 ’24 last week, revenue grew 3% yoy, operating income grew 8% and EPS fell 2% yoy. EPS is undoubtedly feeling the effects of dilution, but given the stock price reaction, you wouldn’t think revenue and EPS both missed consensus by -2% and -1% respectively.

That being said, analysts now think ORCL will grow EPS +12% and revenue +9% in fiscal ’25, with the stock trading at 22x expected ’25 EPS of $6.26 per share. On a PE basis, the stock looks fairly valued, with the other metrics indicating ORCL trading at 7x revenue, 20x and 32x cash-flow and free-cash-flow (ex-cash) and with a 3% free-cash-flow yield.

Readers may not know this but when Oracle typically declares a dividend they pay it for 8 quarters rather than the standard 4 as most companies do. It’s just an opinion, but I suspect this is due to these huge acquisitions ORCL makes every 3 – 4 years, which causes heavy dilution, which ultimately requires large share repurchases, so ORCL builds cash by stretching out the dividend. (This dynamic has been in place for years and I hope I’m not over-simplifying it.)

ORCL’s operating margin hit 46.7% with this quarter’s results, which is a good sign, despite the overall weaker y-o-y revenue and EPS growth.

Management guided to increasing sequential revenue growth for fiscal ’25 (began June 1 ’24). with consensus estimates still at 9% expected revenue growth for fiscal ’25, it sounds like analysts are low-balling or being a little conservative with revenue numbers thus far, which isn’t a bad thing.

Summary / conclusion: Oracle has never really been a large position within client accounts, other than the late 1990’s. Since the software giant is still #3 in the cloud space behind AWS and Azure (in which clients have decent positions, i.e. Amazon and Microsoft), it didn’t seem to make much sense. The rule within tech in the late 1990’s was stay away from all but #1 or #2 in terms of market share leaders across broad tech categories, and it avoided problems. Since Oracle was #1 in on-premise stand-alone database software, it was a logical long.

The question today is, “Can Oracle use AI and overtake Azure or even Amazon’s AWS ?” (that seems very unlikely) and in fact more time will tell but both seem remote.

If you like to trade Oracle stock (as I sometimes do) pay attention to “peak” operating margin, which is usually in the 48% – low 50% range. Oracle’s stock peaked in the early 2000’s with a 51% operating margin (stock peaked at $44 and change in August – Sept ’00) in and didn’t see that margin again until May, 2014, (51%), when the stock peaked again in mid-$40’s and then fell to $33 as the operating margin fell to 30% by May ’16.

Oracle didn’t permanently trade above it’s late 2000 high until 2017.

In late 2021, the stock peaked at $106 per share and then corrected all the way down to the low $60’s, where in 2021 Oracle’s operating margin hit 48.5% (May ’21) and then 46.9% in late ’21 and then slid to 39.5% by late ’22.

Historically, buy Oracle when the operating margin drops into the high 30% – low 40% range and then selling Oracle when the financials print a 48% – 50% operating margin, has been a reliable pattern, but one has to focus on the software cycle too.

The $64,000 question today is whether the AI cycle and Oracle’s position within it, can drive material improvement in the financials where the operating margin materially exceeds 50% – 51%.

That remains to be seen.

Some Oracle was sold when the stock popped following Tuesday’s earnings report, but two older positions remain in client accounts.

The ultimate question is can Oracle change it’s stripes from an on-premise database provider (the legacy business) to a cloud and now AI leader, which it has been transforming to for the last 15 years ? Software companies have the ability to morph business models much easier (unlike hardware companies) but the moats don’t last nearly as long. By the next software cycle, many are playing catch-up again. My impression over the years is that Oracle was late to the cloud (between 2010 and 2017), and now maybe AI is a good opportunity to leapfrog some of the competition.

Maybe. (Not trying to be funny.)

None of this is advice or a recommendation, but strictly an opinion. Past performance is no guarantee of futures results. Investing can and does involve the loss of principal even for short periods of time. All EPS and revenue data is sourced from LSEG or the London Stock Exchange Group.

Thanks for reading.