The brief SP 500 earnings update published Sunday afternoon, June 2nd, ’24, showed some critical data on SP 500 earnings.

Here’s a broader look at the numbers. Despite the Salesforce (CRM) miss and the drop in software stocks last week, the trends in technology sector earnings remain positive.

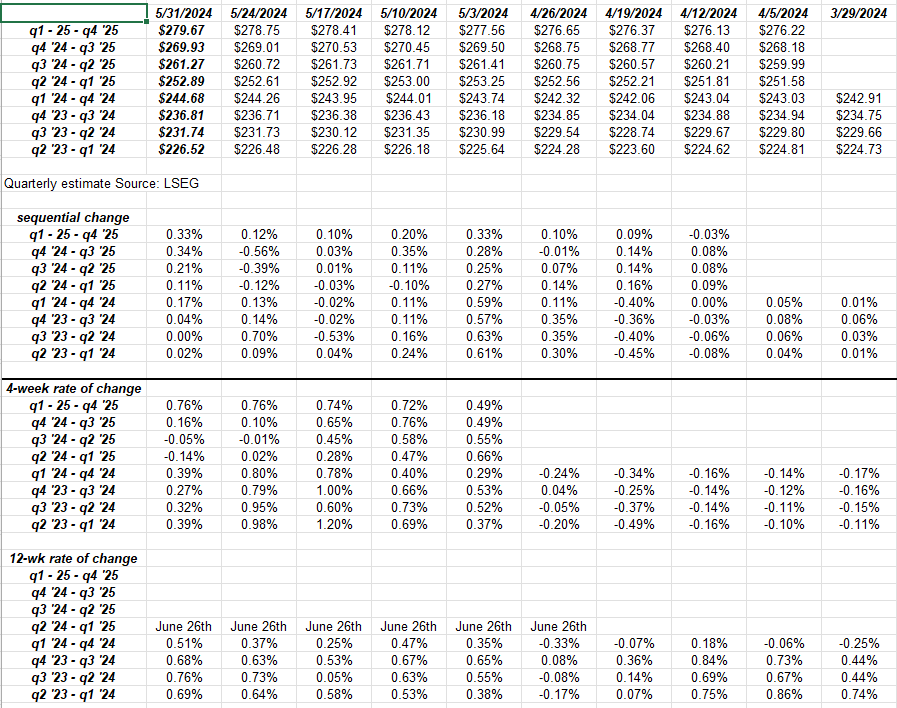

Rate-of-change for annual SP 500 EPS estimates:

The unusual aspect to watching the weekly evolution of SP 500 EPS estimates for ’24 through ’26, is that the revisions continue to be positive. Readers can continue to see the positive “rates-of-change” for the 2024 through 2026.

This table just above this sentence shows the “expected” SP 500 EPS growth rates for ’24 – ’26, but also historical SP 500 EPS growth rates back to 2010.

What’s interesting is the consistency in expected forward EPS growth rates, versus the decade of 2010.

There is nothing about the SP 500 EPS data that seems to indicate a problem with the US economy, at least as of today.

This spreadsheet table is a little wonkier. It shows the “forward 4-quarter” estimate 1-quarter out, then 2-quarters out, etc. and shows the rates of change for what is the equivalent of these forward four-quarter EPS values for the next 8 quarters.

Again, the revisions are gradually higher each week, and even when looking at 4 and 12-week rates of change, the revisions are positive.

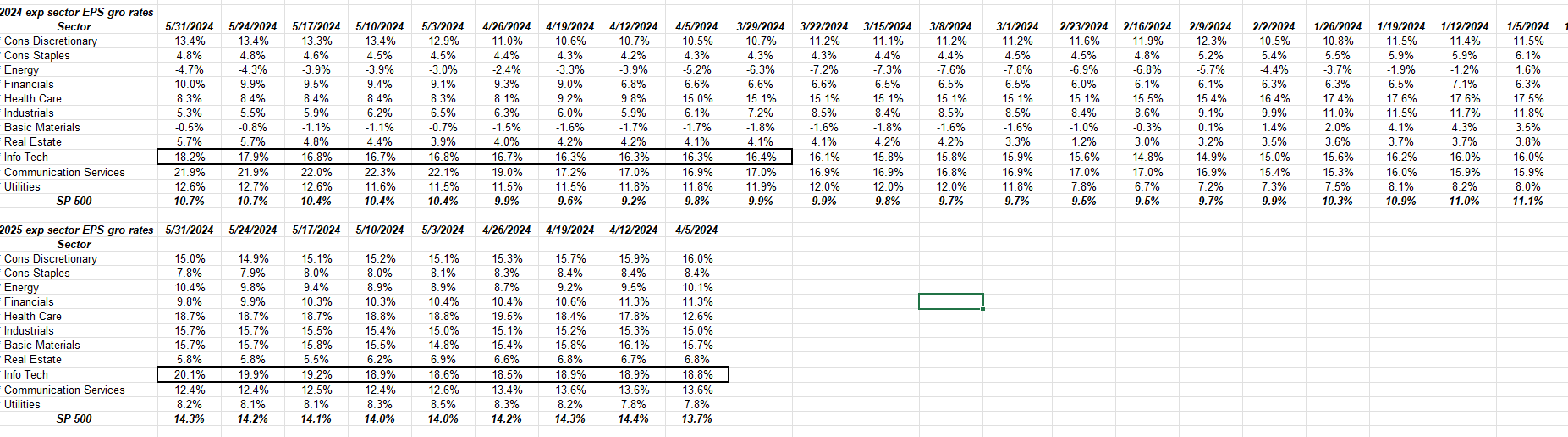

Sector look:

After Salesforce’s (CRM) results last week, Microsoft and Oracle (as well as other enterprise software companies I’d suspect) saw a pretty healthy correction.

However, the black-bordered lines in the sector table above shows continued upward, positive revisions in the tech sector growth rates after Salesforce last week, although this could be driven by semiconductors too. There’s a lot going on in the tech sector. Play the secular waves.

This blog will drill down into some enterprise software estimate revisions since Salesforce this week, and post the results.

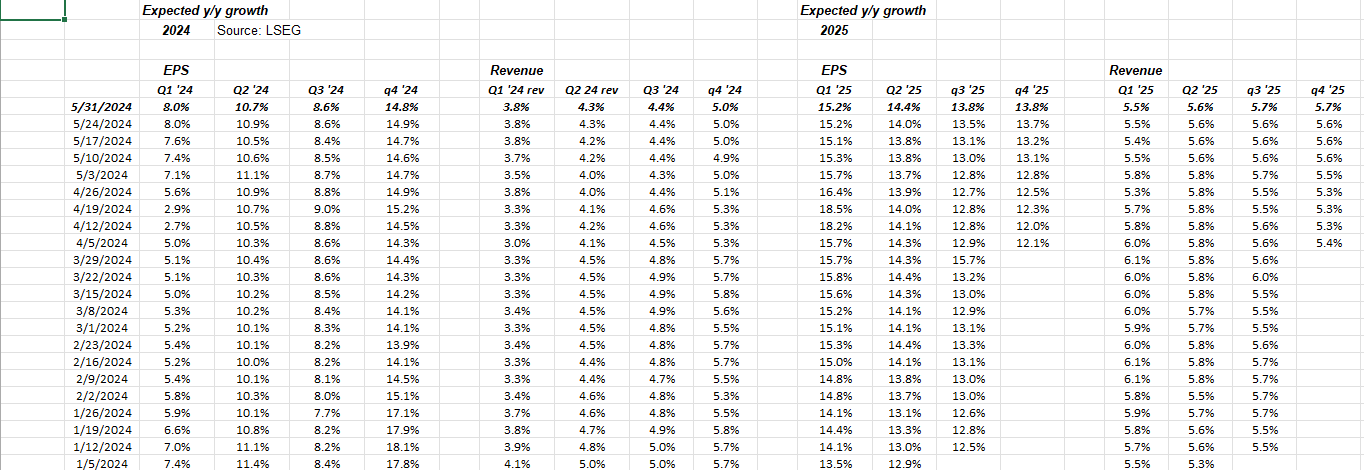

Expected growth rates by quarter (last table):

Note how expected Q2 ’24 is expecting +10% EPS growth rate, while the expected revenue growth rate is 4.4% and has actually slid lower from 5% in early January ’24.

What is fascinating – if readers look at the 2025 data – is that both expected SP 500 EPS and revenue growth rates by quarter are still holding steady.

Again, the pattern (after writing this for years) is that the revisions are typically lower as the forward projections see negative revisions until the actual quarter arrives and then the “upside surprise” is seen.

None of this is advice or a recommendation. Past performance is no guarantee of future results. Investing can involve loss of principal, even for short periods of time.

Summary / conclusion: In the US economy trends can last for a decade or more and then change suddenly based on an exogenous shock like a pandemic, or military action.

The SP 500 EPS and revenue patterns show continued positive revisions, which is a plus, but know that this can change quickly with any destabilizing event around the US economy.

June ’24 earnings will see FedEx (FDX), Oracle (ORCL), Accenture (ACN), Micron (MU), and Nike (NKE) over the next few weeks (but not this week). It’s a good cross-section of the economy and it will also give readers a look into AI and the AI hardware (MU), with Accenture, which we can probably label an AI integrator, and Oracle.

Right now though – as of early June ’24 – the SP 500 EPS and revenue data indicates no change in the glide path of the US corporate profitability.

Thanks for reading.