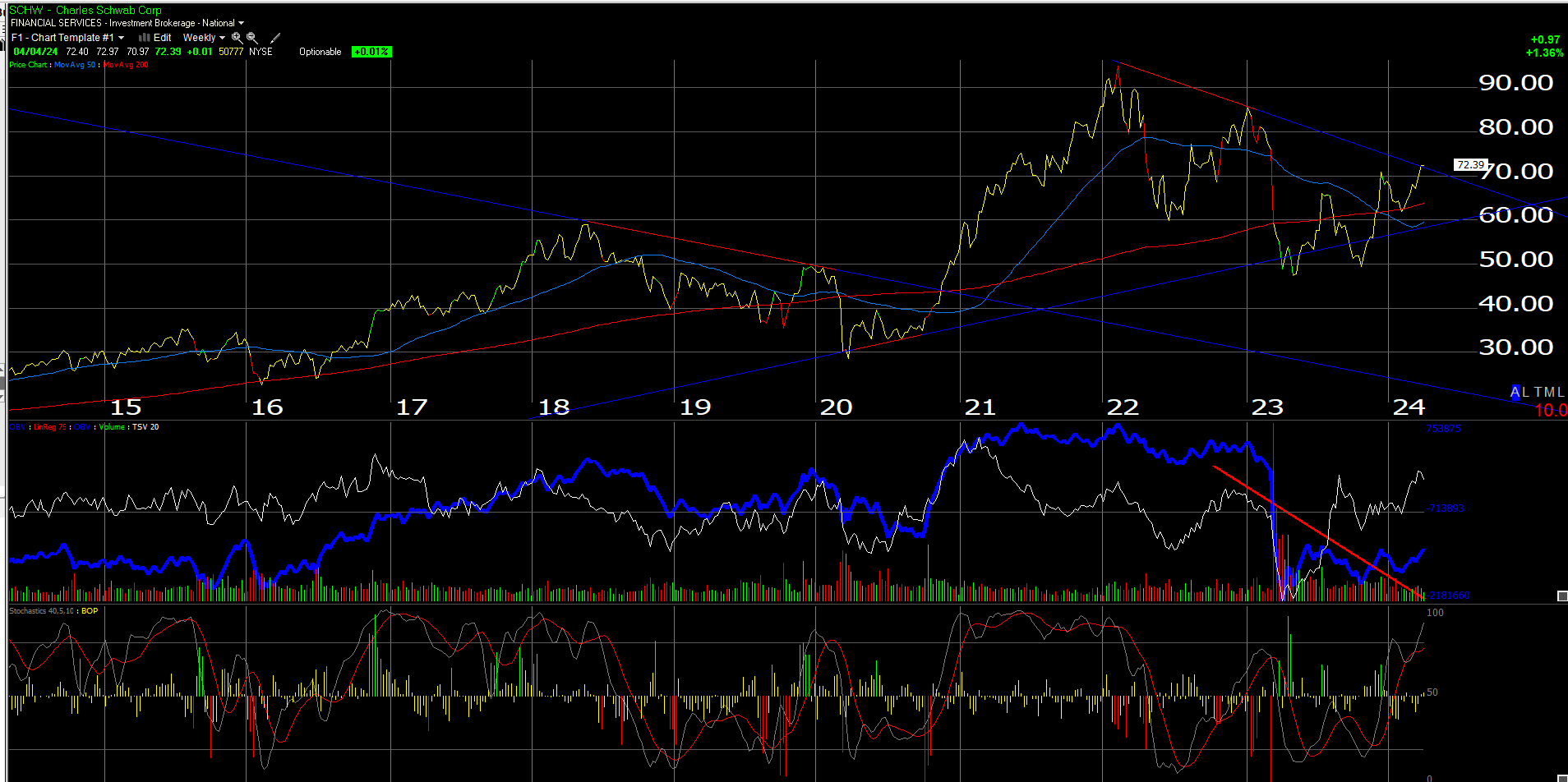

If there are two stocks in the market right now that are feeling the pain of an inverted yield curve (in my opinion), they are Charles Schwab (SCHW) and the regional bank ETF (KRE).

This Schwab chart caught my eye this week as the stock seemed to stall at $72. A trendline was run from Schwab’s $96 high in early ’22 to the current price of $72, and the trendline is one reason the stock stalled near $72.

A hot jobs number tomorrow (probably +200k net new jobs added in March ’24) along with a lower unemployment and hotter “average hourly earnings” will likely send SCHW trading back down toward $60.

A light number tomorrow with the accompanying metrics that the market wants to see, and a decent Treasury rally to boot, will likely send SCHW through the trendline tomorrow and as long as it closes above $72 – $73 Friday, it means the stock is likely headed higher.

The point is I believe SCHW and KRE are good tells for monetary policy, maybe much better tells than the constant prattling by Fed Governors, and Wall Street economists.

It’s puzzling to me why Jay Powell has been consistently talking “rate cuts” (meaning fed funds rate reductions) when the economic data doesn’t seem to support the change in policy at all. Is the Fed worried about something else ?

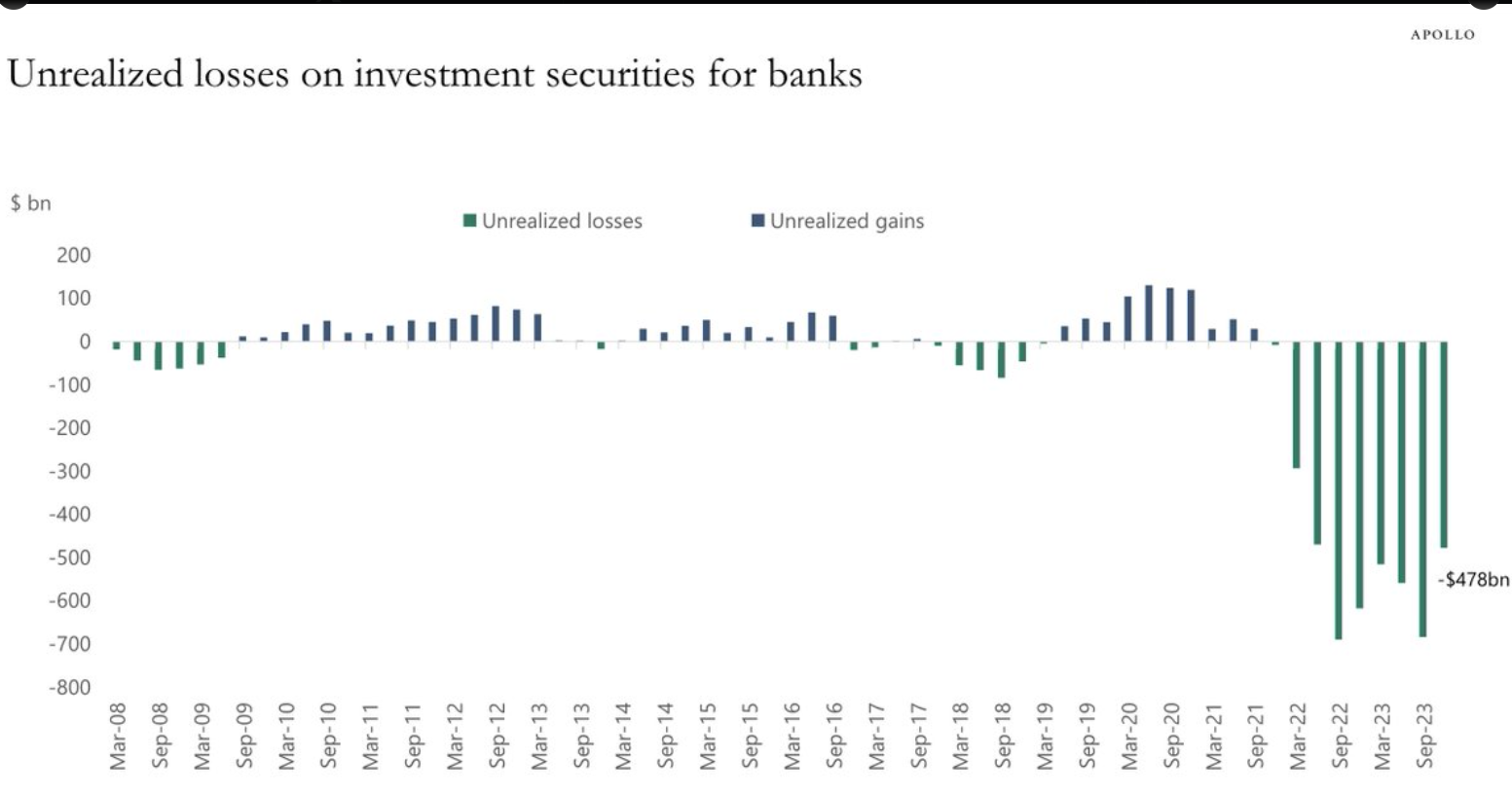

The KRE could use a lower fed funds since it would help the regional banks bleed off some of this commercial real estate exposure and the CMBS (commercial mortgage-backed securities) that go with it. A Chicago periodical today – it might have been Crain’s – noted that Chicago’s office vacancy rate hit 25% this week. The CMBS and commercial real estate, not to mention bank portfolios, could use a little fed funds relief.

Source: The Kobeissi Letter via X

It just seems unusual to me to see a Fed Chair keep discussing a change in monetary policy when that same change seems quite unrealistic, particularly when – during Covid and zero interest rates – at the August ’20 Jackson Hole meeting, Chair Powell noted he “wasn’t even thinking about thinking about (not a typo)” a change in monetary policy.

Investors would likely conclude the Street is leaning into a strong job growth number tomorrow. Annual bond returns have been pretty grim, looking at 3 and 5 year returns per this blog post last night. Other than high yield credit, the bond market hasn’t been contributing much to balanced portfolios.

I can’t recall a payroll report that was well below expectations recently. It seems like most have been big beats with then subsequently lower revisions in future months.

Anyway, SCHW and KRE tomorrow after the March ’24 jobs report, might give readers a tell on monetary policy if the numbers are not clearly decisive.

None of this is a recommendation or advice. Past performance is no guarantee of future results. Investing can involve loss of principal even for short periods of time.

Thanks for reading.